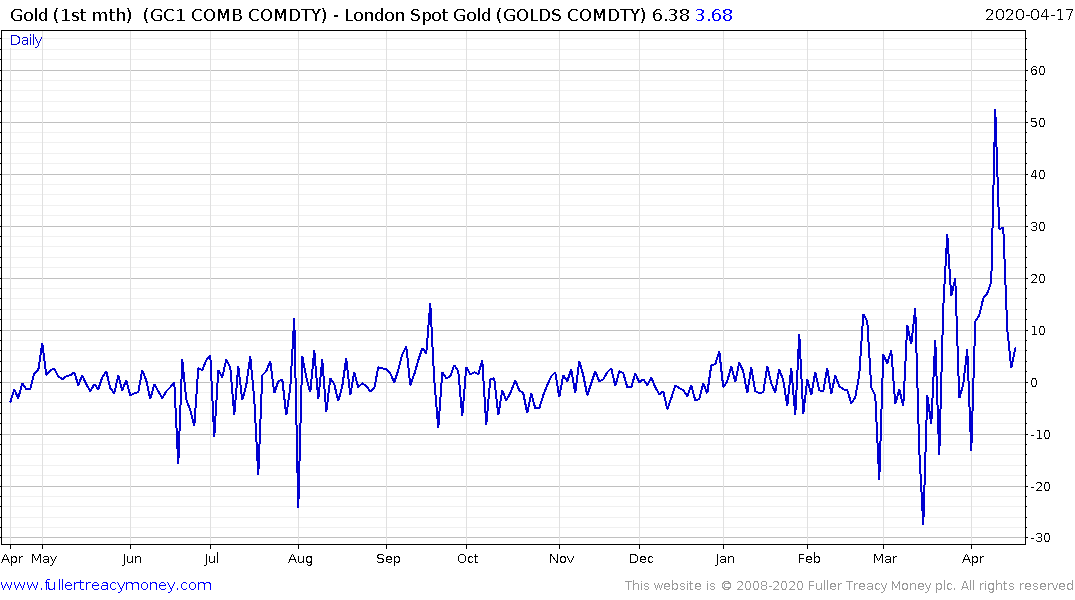

Email of the day on the spread between Comex futures and London spot gold prices:

Hi Eoin, could you please comment on the pricing discrepancies between Comex and spot? It is playing havoc with the Gold ETFs which are not reflecting the underlying as well as they should be.

Thank you for this question which may be of interest to other subscribers. Speculation about what exactly is causing this arbitrage is running hot in the media. The lack of liquidity among market makers, the shortage of refined gold, the break in shipping schedules for the metal and fears about counterparty risk among London bullion banks are all contributing to the historically wide spread.

The spread between Comex front month contract and spot gold in London got a high of $70 in April and has since retreated to $15. That is still around the higher side of the range that prevailed ahead of the coronavirus shut down.

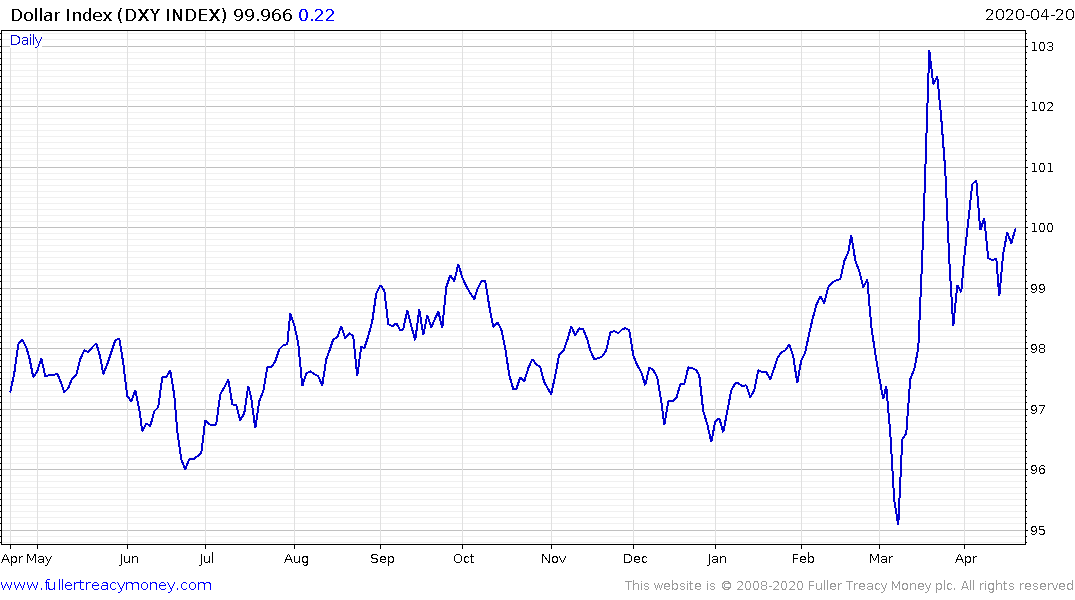

What I find particularly interesting is the commonality between the shape of the chart pattern on the spread with the Dollar Index’s chart. That suggests the arbitrage developed because gold demand spiked in March on the futures market not least for hedging as everything else sold off. Since the spot rate is not a tradable market all demand activity would have shot to the Comex market.