BOJ Is Said to See Little Need to Tweak Yield Control Now

This article from Bloomberg may be of interest to subscribers. Here is a section:

Still, officials aren’t confident enough to say achievement of the BOJ’s 2% price target is in sight, pointing to the need for continued monetary stimulus, the people said.

The yen fell and bonds rose after the report. The yield on 10-year Japanese government bonds fell 1 basis point, while bond futures ticked higher.

Governor Kazuo Ueda and his fellow board members will conclude a two-day policy meeting on June 16. Speaking in parliament Friday, Ueda said that recent data appear to show inflation deviating upward from the BOJ’s base case.

The final policy decision next week will be made after assessing economic data and developments in financial markets up until the last moment, the people said.

As the last anchor of global low interest rates, whether the BOJ will decide to pivot away from easing is a key factor that could cause ripples across global financial markets.

T. Rowe Price, BlackRock Inc. and the European Central Bank are among those warning that any policy normalization from the BOJ may send a wave of Japanese cash flowing out of global markets and surging back home.

Japan’s consumer prices might still be experiencing upward pressure but producer prices have fallen enough to approach the upper side of the underlying range. With slowing global economic activity, and a slow Chinese recovery the likelihood of deflationary forces triumphing has increased. That suggests the BoJ is unlikely to back away from yield curve control in the near term since their primary objective is sustained inflation.

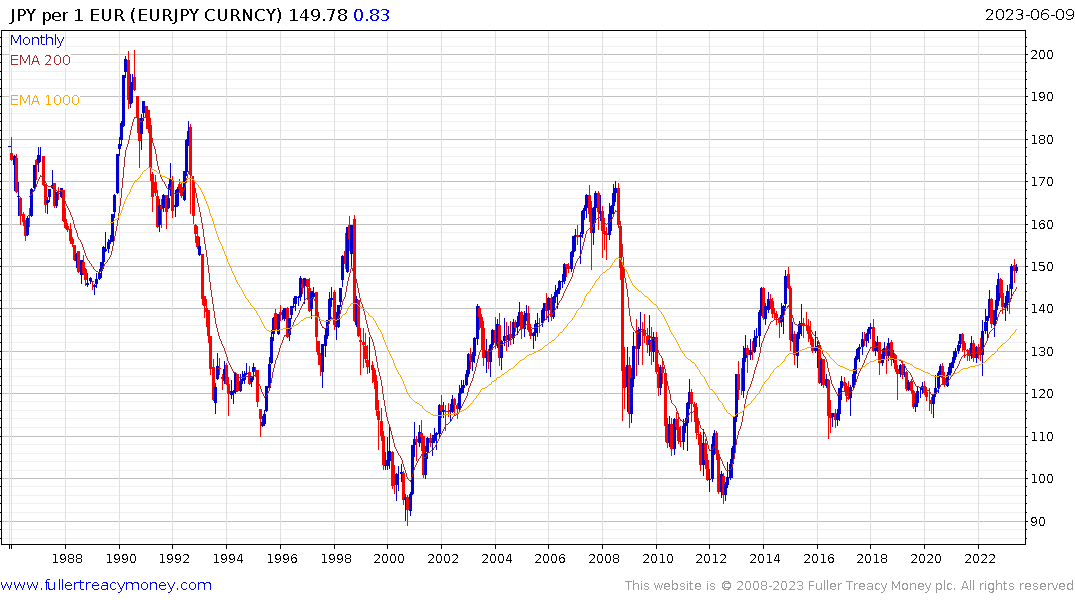

The Eurozone and Japan compete for many of the same export markets so the relative currency pair is probably more significant that Dollar/Yen. The Euro is currently testing the 150 area versus the Yen. That level represents the upper side of the range that has been in place since 2008, so a sustained move above it would set off alarm bells in Frankfurt; particularly as German growth falters.

The Eurozone and Japan compete for many of the same export markets so the relative currency pair is probably more significant that Dollar/Yen. The Euro is currently testing the 150 area versus the Yen. That level represents the upper side of the range that has been in place since 2008, so a sustained move above it would set off alarm bells in Frankfurt; particularly as German growth falters.

The pandemic era introduced competitive currency appreciation as countries battled the inflationary impulse. As growth slows down, some countries are going to be more interested in weakening their currencies to boost competitiveness.

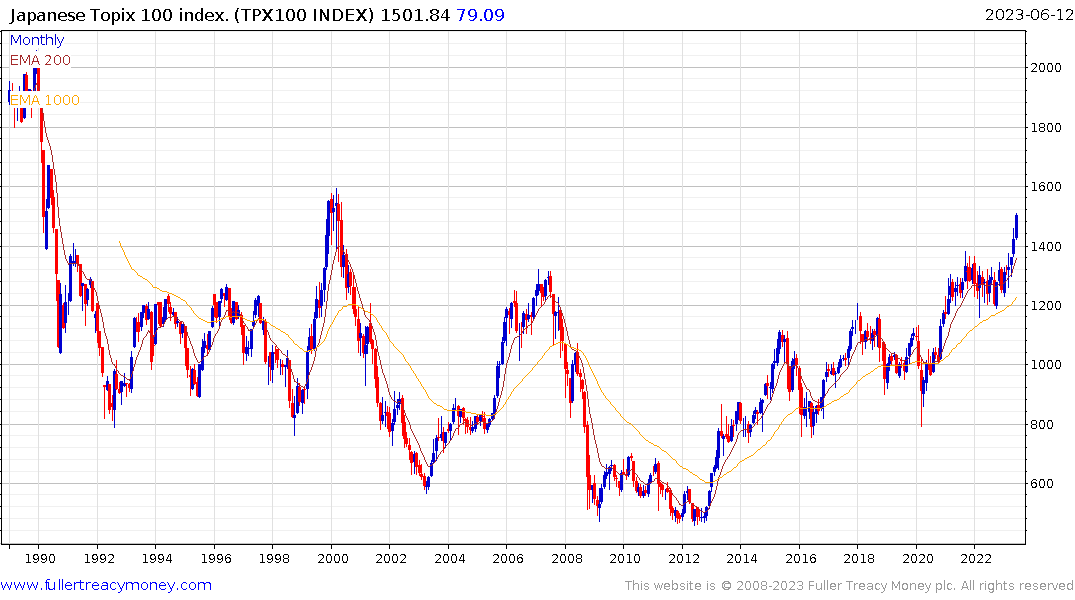

The Topix has now completed a first step above its 30-year base formation. The Nikkei-225 has a similar pattern. The market is being led higher by industrials with low/attractive valuations like Kobe Steel or Mitsubishi Corp.

The Topix has now completed a first step above its 30-year base formation. The Nikkei-225 has a similar pattern. The market is being led higher by industrials with low/attractive valuations like Kobe Steel or Mitsubishi Corp.

The big question is now in whether Japanese money will be encouraged home by a more attractive rate environment but whether foreign capital will be attracted by relative strength and attractive valuations. The retooling of the global industrial sector to allow for the possibility of greater competition with China is a clear bullish phenomenon for a large swathe of the Japanese markets. The underperformance of the Chinese market despite reopening suggests Japan is the destination of choice to play that theme from a country perspective.

This report from GMO discussing the performance of value oriented investments during recessions may also be of interest.

Back to top