Yield Curve Inversion Is Inconclusive. Our 2650-2800 Range Holds

Thanks to a subscriber for this report by Mike Wilson at Morgan Stanley. Here is a section:

Here is a link to the full report and here is a section from it:

We did our own analysis on the yield curve inversion looking at the limited historical occurrences available (Exhibit 2 and Exhibit 3) and found that inversion is neither bullish nor bearish and far from conclusive either way. In other words, an inverted yield curve is important for other reasons (which we will get to) but it is far from conclusive regarding what to do with one's portfolio. In past cycles, the yield curve has often inverted twice before we have an economic recession (the primary and secondary inversion). Exhibit 2 shows what happens in the S&P 500 (market) and each sector going into the first inversion since that is what we are looking at this time. As you can see, the market is usually positive into the inversion but with very narrow performance led by Technology stocks (and other growth names). This cycle looks different, with the market trading poorly into the inversion (assuming it is near), with defensive sectors leading and Tech the second worst performer after Energy on a 1- and 3-month basis. To be clear, the curve has not officially inverted yet which may explain the difference. However, what's clear is that this time is very inconsistent with the historical patterns.

Exhibit 3 shows what has happened historically after the inversion. The market performance is generally poor on a 1- and 3-month basis and basically in line with the average market performance on a 6-month basis during all periods. From a sector standpoint, it appears that defensive and early cyclicals lead--a value bias while Tech and Discretionary lag. This is how we are positioned in our sector preferences. Once again, it's important to note that curve inversion hasn't actually happened yet, making this analysis potentially meaningless.

Despite investor feedback saying we are mid-cycle, we continue to hold our late-cycle view. We have also had numerous questions about our late cycle view, with many investors suggesting we are actually mid-cycle. If true, such a conclusion means curve inversion is irrelevant from a market standpoint, furthering their bullish view. The near inversion of December 1994 is one cited as the best comparable to the current situation. With respect to this "mid-cycle" view, we disagree due to a few irrefutable facts. Specifically, the unemployment gap relative to NAIRU, the output gap, and consumer confidence all look very different than they did in December 1994, which was indeed a mid-cycle situation. Exhibit 4 illustrates just how different it is today. In fact, on all three measures, the US economy has rarely reached such high levels.

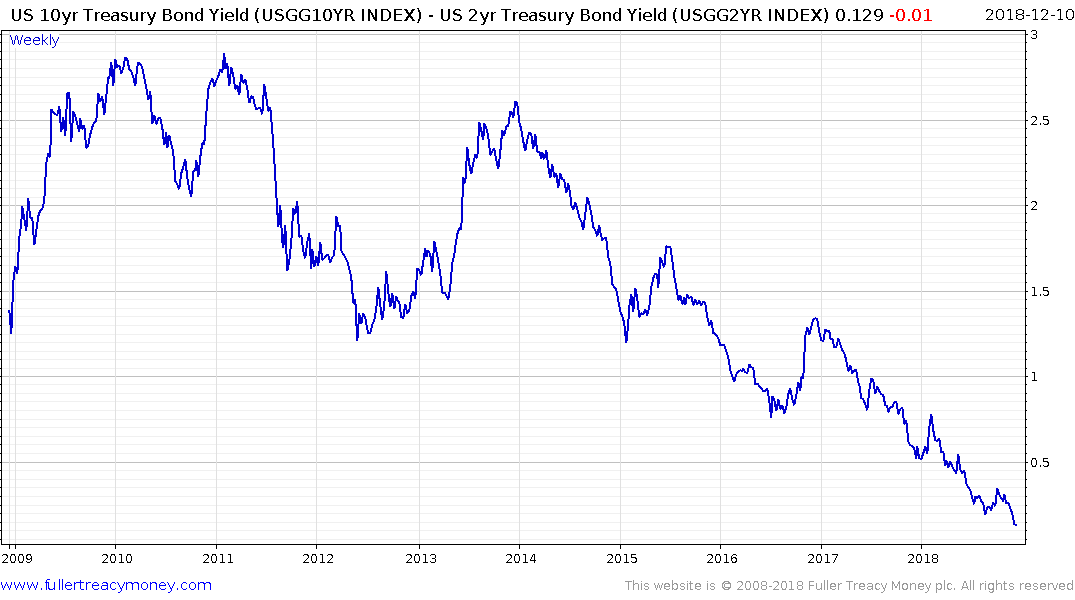

As the above report highlights the yield curve has not yet inverted but at 13 basis points it is very close to inverting. There is definitely some chatter about the near inversion in 1994 and how that presaged the evolution of the bubble in the late 1990s.

.png)

One important arbiter of that rally was that while high yield spreads widened somewhat in 1994, the expansion was contained. Today high yield spreads are breaking out of a very inert rage which would normally suggest they have room to rally further. A clear downward dynamic will be required to check the trend of widening.

Therefore, the key arbiter of whether a yield curve inversion can be avoided probably lies with Fed policy and whether they are willing to state they have achieved their objectives in raising interest rates and are willing to pause.

The clearest lesson from monitoring the yield curve spread is that it is a reliable lead indicator when the spread in fact inverts. Right now we can anticipate that earnings are not going to be as positive in 2019 as they were in 2018 and the lead indicators for stress are beginning to flash red. That suggests it is time for caution and we would do well to remember that ranges are explosions waiting to happen.

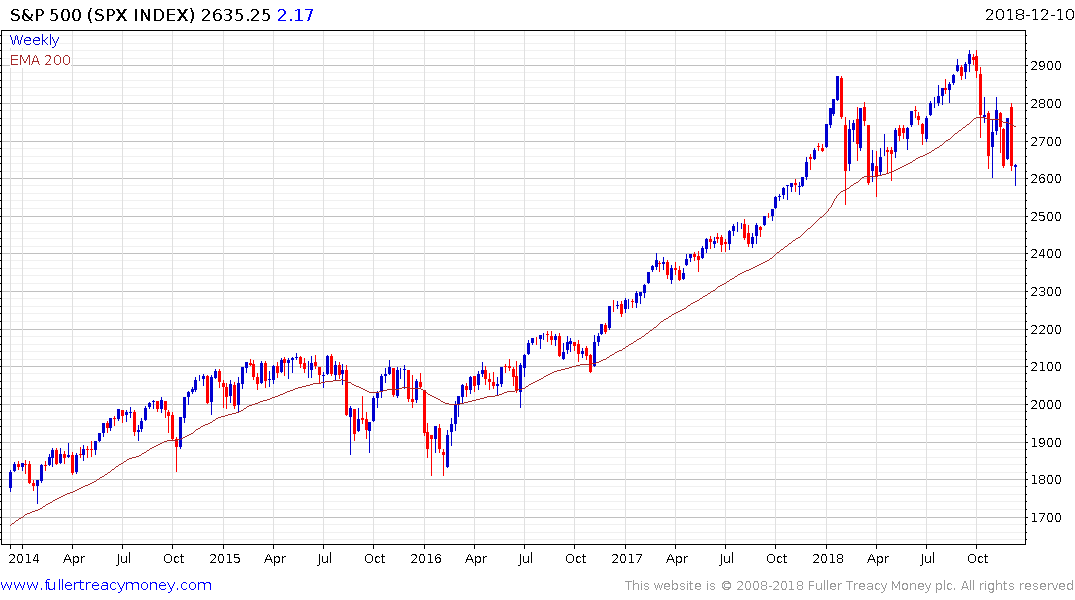

The S&P500 has been ranging below its trend mean since October and while it is above the January low, there has been a significant loss of uptrend consistency. That tells us at the very minimum that supply and demand are back in balance or may even be reversing. A short-term oversold condition is evident but it needs to sustain a move back above the trend mean to signal a return to demand dominance beyond steadying.