Xi Puts Ideology Before Economy With Market-Busting Lockdowns

This article from Bloomberg may be of interest to subscribers. Here is a section:

China’s worst equity selloff since early 2020 reflects a growing concern about President Xi Jinping: He

can’t afford the political costs of shifting from a Covid Zero strategy that is pummeling the economy.

In Shanghai, a weekslong Covid-19 lockdown got even worse, with workers in hazmat suits fanning out over the weekend to install steel fences around buildings with positive cases. In Beijing, the process is just getting started, as authorities on Monday began shutting down a bustling district in the capital to

quash fresh outbreaks.

The threat of paralyzing China’s two largest and wealthiest cities with a strategy abandoned by most countries helped push the CSI 300 down 4.9%, the gauge’s steepest one-day drop since the first such lockdown in Wuhan two years ago. The spreading lockdowns have investors worried that Xi is sacrificing the Communist Party’s reputation for pragmatic economic management to defend a political narrative that portrays him as the world’s most successful virus-fighter.

“This Covid situation is really putting China into a very dark moment, perhaps the darkest moment in economic terms for the last couple of decades,” Junheng Li, JL Warren Capital founder and chief executive officer, said of the Shanghai lockdown during an interview on Bloomberg TV. “It’s a confidence

crisis in a sense that you’ve got the most affluent city in China with this consensus disappointment and resentfulness towards a very non-sensible policy.”

“People really don’t know, what’s a clear path to get China out of this Covid situation,” Li said.

Democratic capitalist systems focus on the health of the corporate/financial system to achieve social cohesion and rising living standards. Communist systems focus on sustaining political stability to achieve the same ends. That difference doesn’t become obvious until a crisis challenges it.

Originally, capitalist systems relied on brutal wipeouts to clear out the ills of misallocated capital. Appetite for such tough medicine is difficult to sustain over time and particularly as living standards rise.

I think of it as similar to Tabata workouts. They are short, severe and require maximum effort. If you don’t feel like you are on the verge of passing out, you don't get the full benefit. It’s easy to muster the courage for these kinds of workouts for a few weeks, but sustaining the routine is psychologically difficult.

The credit crisis in 2007/08 rocked the capitalist system to its foundations. The response to the crisis was to bail out the financial sector at the expense of consumers. That seeded the crypto revolution, political populism and polarization, and the revolt against globalization and profiteering.

The response to the pandemic attempted to correct some of the errors made in the response to the credit crisis. Strategies favoured consumers and large corporations but unfortunately eviscerated the small business and hospitality sectors. The increase in debt, formalization of a standing repo facility and bans on foreclosures and delays on debt repayments have only served to further increase leverage in the financial system. This is not a capitalist system but is rather a nanny socialist state. That is only likely to further intensify since consumers are not yet willing to take the tough medicine of asset price retrenchment and balanced budgets.

For communist systems the sanctity of the Party comes before every other consideration. There is a no room for failure since any admission of fallibility questions the moral authority of the entire system. When times are good, and credit is expanding communist systems are capable of startling progress. Unity of purpose is championed while every other consideration is sidelined. That cuts both ways. In times of stress, the Party’s unity of purpose is pointed squarely at ensuring nothing questions the system. Every other consideration comes a distant second.

The response to the credit crisis was to flood the market with liquidity. Salvaging the proud record of outsized growth at 10% per annum trumped every other consideration. That saved the global economy, but it saddled China with significant debts, a housing bubble and highly valued technology companies capable of challenging central authority.

During the pandemic China also sought to correct the mistakes made in the response to the credit crisis, from their perspective. Supply of liquidity was parsimonious and not least because manufacturing activity surged as global demand spiked. That afforded the Party the opportunity to crack down on tech companies, tutoring and overleverage in the property development sector.

Success in containing the virus was championed and used as an argument to justify greater control of the population. The political imperative of ensuring Xi’s third term is all the justification needed to do whatever is necessary to control the public.

Lockdowns in Shanghai have been characterized by food insecurity, dire conditions in quarantine facilities, underreported deaths and profiteering by food distribution officials. Beijing is on the verge of also facing lockdown. These cities are where people have benefitted most from Communist rule, and they have long enjoyed privileges much of the rest of the country could only dream about. The lockdowns are a hard dose of reality for millions of people.

China’s impending economic slowdown is negative for all industrial resources. The lesson we learned from the pandemic is the spike in cases lasts for about six weeks at a time. That may be longer for China because the strict lockdowns will slow the advance from one city to another. The virulence of the omicron and delta variants mean they are practically impossible to contain. The best China can hope is to slow the advance.

Destruction and rebuilding of credit and political ideas is a feature of the capitalist democratic system. It’s not a bug. Malleability is its greatest strength. The biggest challenge for Communism is it looks strong when it is doing well and struggles to adapt to anything that threatens the system. Singlemindedness is its greatest strength but also its greatest fragility.~

Copper pulled back sharply today to test the region of the 200-day MA. It will need to bounce soon, if the upward bias is to be sustained.

The Brazilian market tends to trade in line with commodities. It was the best performing market in Q1 and is likely to give up most of that advance as commodities correct.

The Brazilian market tends to trade in line with commodities. It was the best performing market in Q1 and is likely to give up most of that advance as commodities correct.

.png)

Crude oil also extended its decline today to test the recent lows and looks likely to fall further if China’s lockdowns do continue to spread.

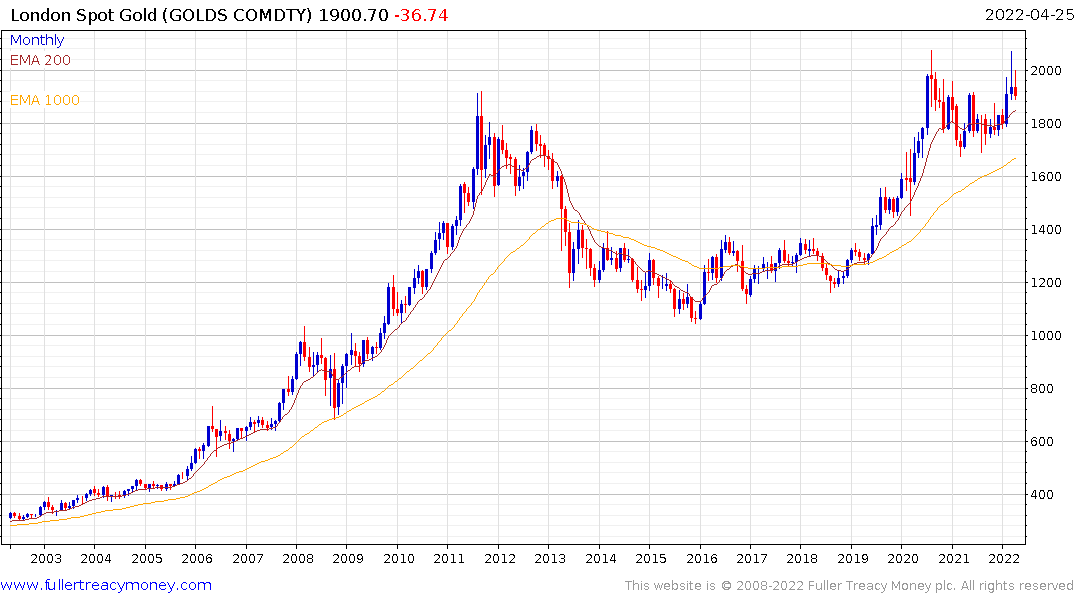

Gold was not spared selling pressure today and pulled back to also test its lows for the last couple of months.

Gold was not spared selling pressure today and pulled back to also test its lows for the last couple of months.

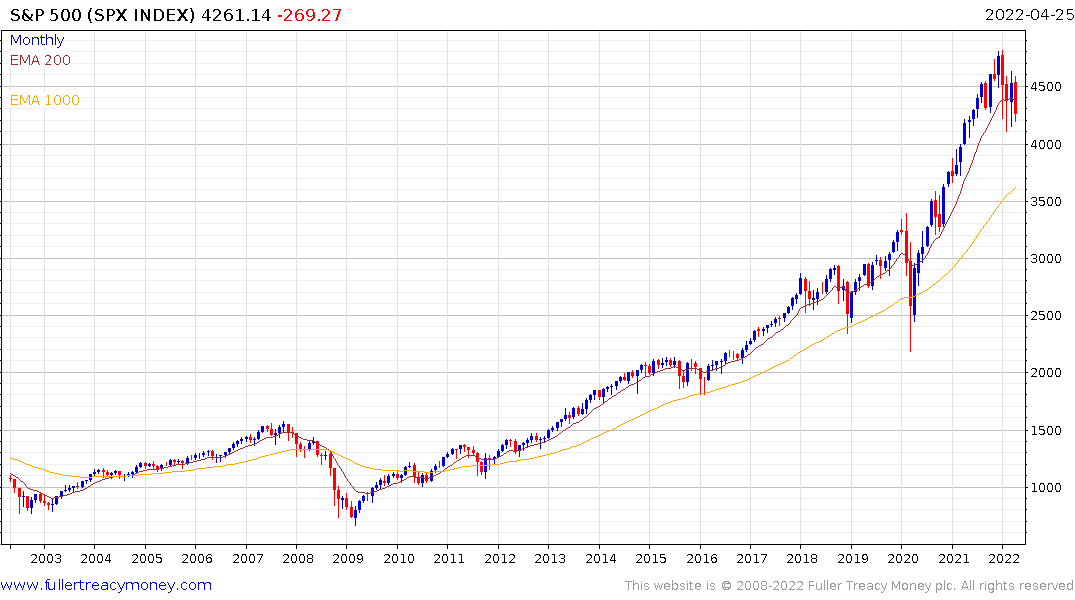

If commodities correct it removes some of the pressure on central banks to aggressively raise rates. That should help to support stock markets, so the current weakness is potentially a sell-the-rumour-to-buy-the-news event of the first 50-basis point hike next Wednesday (May 4th). That should support prices for a time, but the correction is unlikely to end until central banks declare a partial victory over inflation and ease policy in response to slowing growth.