Why We Don't Trust Government Inflation Statistics...

Thanks to a subscriber for this interesting report from Oppenheimer which may be appreciated by the Collective. Here is a section:

We all know that nominal interest rates are a function of real interest rates and inflation expectations. The nub of our argument is that the consumer price index (CPI) as measured by the Bureau of Labor Statistics (BLS) sharply understates what bond investors should incorporate into their inflation expectations.

The first component of our three-part argument is that CPI measures inflation where the people are, not where the money is. That is an appropriate stance for BLS since CPI is used to set government benefit levels, but consider that the top 20%, who effectively own all the bonds, generate as much consumer spending as the lower 62%. The basket of goods that 20% buys likely differs significantly from the basket of the average person.

Second, we look at the healthcare anomaly. Healthcare accounts for 17.7% of GDP and 14.5% of the S&P 500 but only 8.5% of CPI. Most private sources estimate healthcare costs have been increasing by ~6%+ in recent years, but BLS puts the number at 2.8%. A recent study found that the average health insurance plan now costs ~$19K (with ~$6K from the employee), but healthcare insurance is just 1.004% of CPI.

Third, in looking at how CPI is calculated, we suspect there is a "streetlight effect," where one searches where the light is good rather than where the sought object is likely to be. In the case of CPI, we suspect they measure what is easily quantified. There is incredible granularity on the cost of apples, bananas and peanut butter but only big sweeping categories for healthcare and housing.

The bottom line is that we think CPI substantially understates the inflation expectations that investors should incorporate into the pricing of bonds and that long-term rates should increase. One does not have to believe this to own bank stocks as they remain cheap in any case at a 66% relative P/E, but if we are correct about CPI, the upside should be even better.

Here is a link to the full report.

Anyone who lives in the real world and pays their own bills, mortgage and taxes knows inflation is understated. Additionally, since government spending is integrally tied to official statistics, politicians have an interest in the understatement persisting not least because fiscal deficits are already wide. However, it is reasonable to conclude that we have had such an uptick in reactionism against the status quo is because consumers have direct experience of inflation which the statistics refuse to acknowledge.

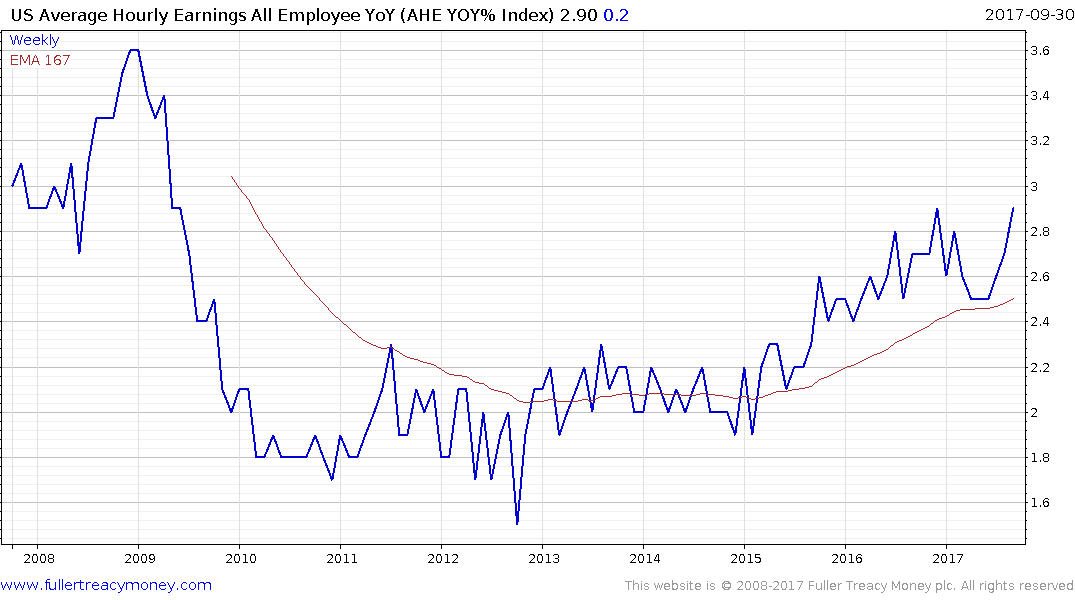

Part of the reason wages are so important is because they are difficult to headonic out of the data. If people are demanding more for the same work that is inflationary. US Average Hourly Earnings for All Employees recovered abruptly at the last update and have trending characteristics.

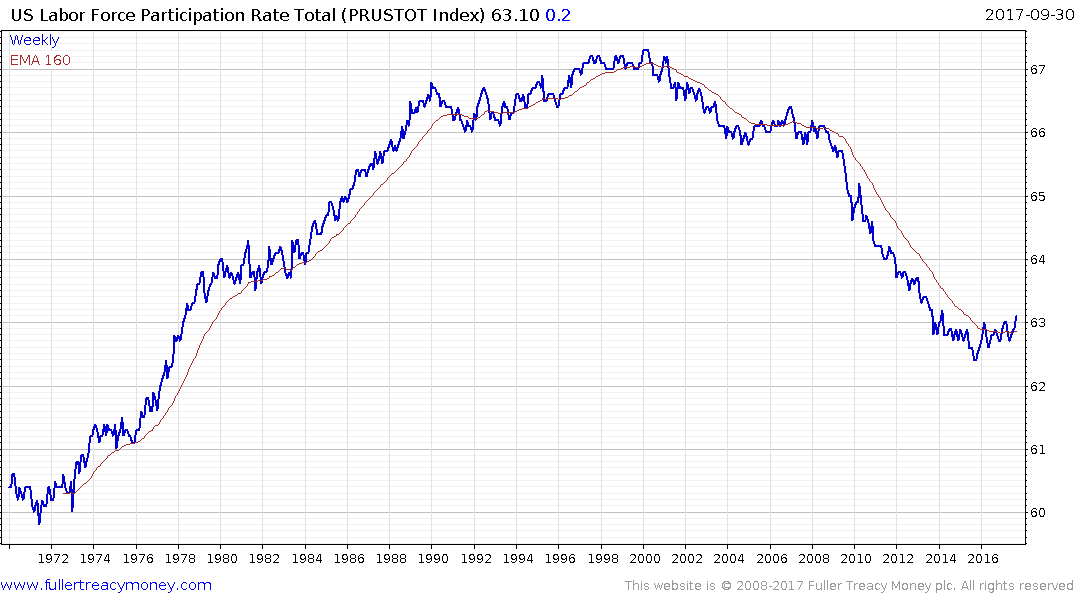

Meanwhile labour force participation has broken out to new recovery highs. If more people are in the workforce and they are asking for more money that represents a compelling argument inflation is increasing.

Gold tends to do best when inflation is outstripping central bank efforts to combat it. It firmed today for the first time in four days and will need to continue to hold the $1250 area if potential for additional higher to lateral ranging is to be given the benefit of the doubt.

Silver firmed in a more emphatic fashion today.