What If Big Oil's Bet on Gas Is Wrong?

This article by Jack Farchy and Kelly Gilblom for Bloomberg may be of interest to subscribers. Here is a section:

Driving the shift has been a sharp decline in the cost of building new renewable power –- which, unlike generating electricity from coal or gas, is almost free to run after the initial capital investment has been made.

“Wind and solar are just getting too cheap, too fast" for gas to play a transitional role, said Seb Henbest, lead author of the BNEF report.

The consultant estimates that onshore wind and solar power are already competitive with coal and gas in Germany, and that within five years they will be cheaper to build than new coal and gas plants in China, the U.S. and India. By the late 2020s, it will start to even be cheaper to build new onshore wind and solar power than run existing coal and gas plants.

The trends that are undercutting optimism about the global gas outlook are already playing out in Europe. Natural gas demand remains well below a 2010 peak, as greater energy efficiency, rapid adoption of renewables and resilient coal consumption cut into its market share.

The IEA does not see European gas demand returning to its 2010 high. In its base case scenario, European gas demand would be at the same level in 2040 as in 2020.

Since the majority of globally traded natural gas is tied to long-term contracts producers have some security in the investments they made. However, a decade of high oil prices created the perception of long-term outsized profits and the reality is likely to be more modest. The extent to which coal will survive as a fuel stock against increasingly high regulatory barriers as well as innovation in storage solutions are likely to be key determinants in the success of what have been massive investments in natural gas which has contributed significantly to global supply.

Both Royal Dutch Shell and Exxon Mobil produce more gas than oil.

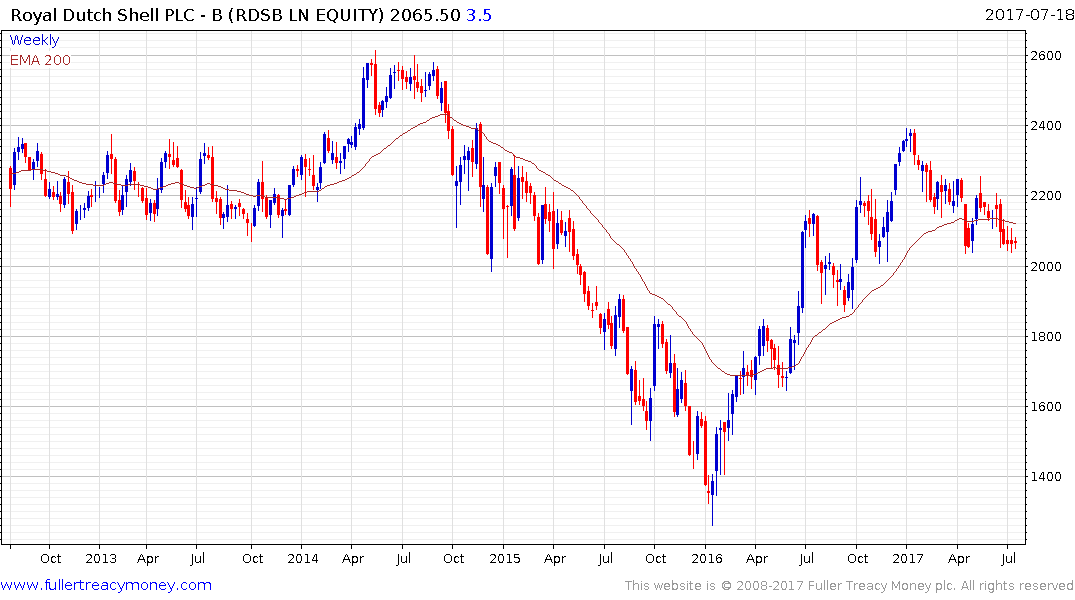

Royal Dutch Shell (Est P/E 15.61, DY 7.17%) continues to steady in the region of the late April/early May lows and the trend mean. It needs to hold the 2000p level if medium-term scope for continued higher to lateral ranging is to be given the benefit of the doubt.

Exxon Mobil (Est P/E 21.95 DY 3.82%) has also pulled back since the beginning of the year and is also testing its early May lows. A break in the sequence of lower rally highs will be required to question the medium-term downward bias.