Weekend Reading May 1st 2015

Thanks to a subscriber for this list of mostly academic reports which we can reasonably conclude constitute at least part of the weekend reading for policy makers.

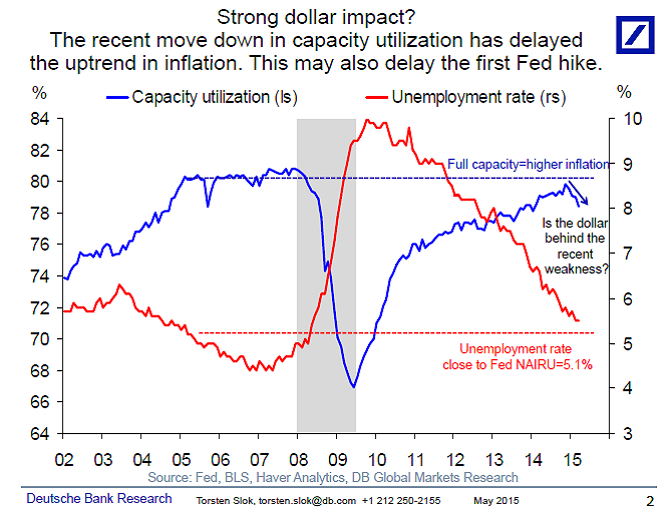

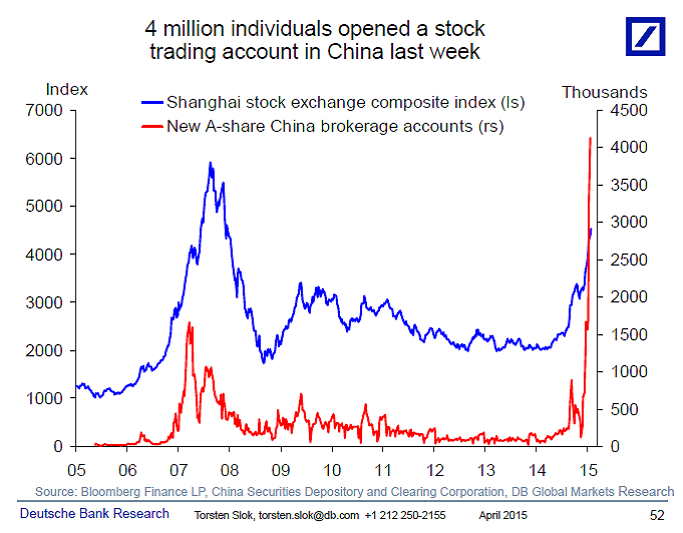

Two charts from Torsten’s Chart Book, the first one important, the second one….

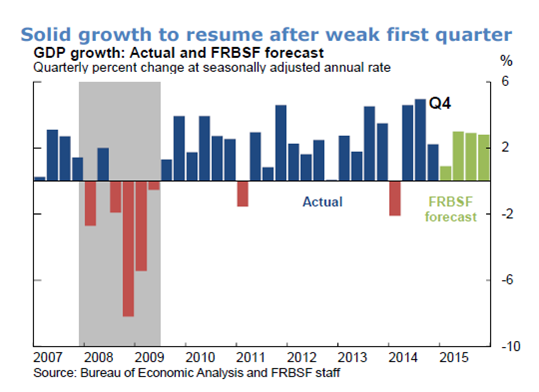

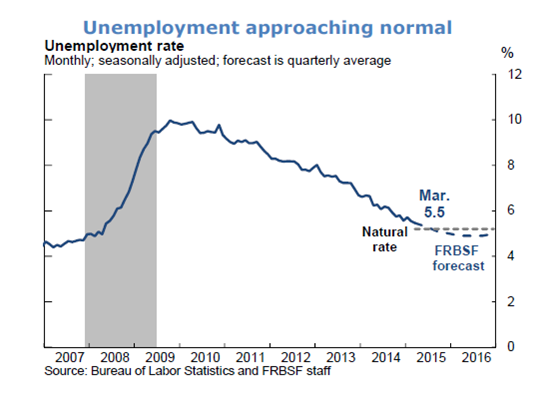

SF Fed sees rebound in Q2 and Q3

“With winter behind us, we expect above-trend growth to resume in the second quarter and continue for the rest of 2015. Accommodative monetary policy along with ongoing improvements in credit market conditions, asset values, and household incomes related to the strong labor market all are expected to help sustain this solid growth.”

IMF: “Recent US Labor Force Dynamics: Reversible or not?”

The U.S. labor force participation rate (LFPR) fell dramatically following the Great Recession and has yet to start recovering. A key question is how much of the post-2007 decline is reversible, something which is central to the policy debate. The key finding of this paper is that while around ¼–? of the post-2007 decline is reversible, the LFPR will continue to decline given population aging. This paper’s measure of the “employment gap” also suggests that labor market slack remains and will only decline gradually, pointing to a still important role for stimulative macro-economic policies to help reach full employment. In addition, given the continued downward pressure on the LFPR, labor supply measures will be an essential component of the strategy to boost potential growth. Finally, stimulative macroeconomic and labor supply policies should also help reduce the scope for further hysteresis effects to develop (e.g., loss of skills, discouragement).

Fed: “Have Distressed Neighborhoods Recovered?”

During the 2007-2009 housing crisis, concentrations of foreclosed and vacant properties created severe blight in many cities and neighborhoods. The federal Neighborhood Stabilization Program (NSP) was established to help mitigate distress in hard-hit areas by funding the rehabilitation or demolition of troubled properties. This paper analyzes housing market changes in areas that received investments during the second round of NSP funding, focusing on seven large urban counties. Grantees used NSP to invest in census tracts with high rates of distressed and vacancy properties, and tracts that had previously received other housing subsidies. The median NSP tract received quite sparse investment, relative to the overall housing stock and the initial levels of distress. Analysis of housing market outcomes indicates the recovery has been uneven across counties and neighborhoods. In a few counties, there is some evidence that NSP2 activity is correlated with improved housing outcomes.

BIS: “The costs of deflations: a historical perspective”

Concerns about deflation – falling prices of goods and services – are rooted in the view that it is very costly. We test the historical link between output growth and deflation in a sample covering 140 years for up to 38 economies. The evidence suggests that this link is weak and derives largely from the Great Depression. But we find a stronger link between output growth and asset price deflations, particularly during postwar property price deflations. We fail to uncover evidence that high debt has so far raised the cost of goods and services price deflations, in so-called debt deflations. The most damaging interaction appears to be between property price deflations and private debt.

BIS: “(Why) Is investment weak?”

In spite of very easy financing conditions globally, investment has been rather weak in the aftermath of the Great Recession. What explains this apparent disconnect? The evidence suggests that, historically, uncertainty about the future state of the economy and expected profits play a key role in driving investment, and financing conditions less so. As a result, investment after the Great Recession appears to have been broadly in line with what could have been expected based on past relationships. A stronger recovery of investment would seem to depend on a reduction in economic uncertainty and expectations of stronger future growth.