US 10-Year Yield Slips Back Below 3% as Recession Fears Grow

This article from Bloomberg may be of interest to subscribers. Here is a section:

The latest leg of the bond-market rally came after Fed Chair Jerome Powell said on Wednesday that the risk of harm to the economy from higher rates was less important than restoring price stability. Traders continue to expect another 75-basis-point rate increase in July, and swaps referencing Fed policy

meeting dates price in a peak rate near 3.5% in March 2023, followed by a drop to about 3% by year-end.

“The market is digesting increasing odds of recession,” said Janet Rilling, senior portfolio manager at Allspring Global Investments, which manages $541bn in assets. And it’s likely that “inflation will stay pretty elevated. So the Fed will continue to be aggressive” raising rates.

In turn, she said the extent of the recent drop in Treasury yields means shifting to a more defensive posture. “Watching today’s movement, this could be presenting an opportunity here

to reduce duration.”The market added to gains, amassed before the US trading day began as European bond markets rallied, after the release of personal income and spending data for May. Spending rose 0.2%, half the expected increase. The price index for purchases rose 0.6% versus an expected 0.7%, supporting the view that an

inflation peak is being established.

I’ve seen a lot of commentary in the financial media about where R-star might reside. It’s a valuable discussion. Afterall, we all want to know what the real inflation-adjusted neutral rate of interest is. However, the discussion must be grounded in accepting that it is impossible to prove until after the fact.

Money supply doubled in the month to April 2020 and remained at an elevated month-over-month level for a year. That quantity of money printing has resulted in a significant inflation scare. It overstimulated demand at a time when supply was constrained from responding as quickly. The volume of outstanding debt is higher today than during any previous cycle, so investors are understandably troubled.

Money supply doubled in the month to April 2020 and remained at an elevated month-over-month level for a year. That quantity of money printing has resulted in a significant inflation scare. It overstimulated demand at a time when supply was constrained from responding as quickly. The volume of outstanding debt is higher today than during any previous cycle, so investors are understandably troubled.

Meanwhile, China’s record trade surplus during the pandemic suggests supply conditions were relatively normal, but demand went up so fast that producers were under pressure to respond and many were forced to add capacity.

Month over month US money growth was negative in April and was at 1.3% in May. Meanwhile the Federal Reserve has just begun to reduce the size of its balance sheet. This is siphoning liquidity out of the global economy. Demand is ebbing, warehouses are full, and suppliers still have excess capacity. This suggests there is a clear scope for a significant period of readjustment.

Micron’s warning on chip demand is a foretaste of what is to come for the semiconductors sector. It is worth remembering that nothing has happened to alter the cyclicality of this industry.

Micron’s warning on chip demand is a foretaste of what is to come for the semiconductors sector. It is worth remembering that nothing has happened to alter the cyclicality of this industry.

Nine months ago, I inquired from Generac about getting a back-up generator for my home. The closest appointment was a month out. They were asking for a 30% deposit before scheduling a consultation and did not expect to be able to install until September 2022.

Nine months ago, I inquired from Generac about getting a back-up generator for my home. The closest appointment was a month out. They were asking for a 30% deposit before scheduling a consultation and did not expect to be able to install until September 2022.

Since I was concerned about outages over the winter, I did not see the point in waiting until after this summer for an install. I saw the same generator for sale on the floor of a local Costco last week. That’s a massive turnaround in the availability of a big-ticket item.

Mrs. Treacy’s latest container of inventory is currently en route from China. The cost of shipping is down about 60% since the last time she imported. That is likely to be representative of the wider economy. I think it is only a matter of time before we see significant price cuts to clear inventory.

There is a real tendency to think our lives will never be the same again after the pandemic. It was a traumatic event for everyone. It caused a great deal of upset and people reacted in different ways. But, will they keep reacting?

I think about my own actions. We rushed to move out of California after BLM activists attempted to extort money from us and protested outside our door when I refused. We then rushed to buy a new house, kitchen, furniture, enrolled our girls in an elite school, paid initiation for a new club membership and bought a new car. We also had surprise spending like replacing the foundation and putting in a new floor. If that level of spending is analogous to the wider population it helps to explain the jump in demand. It’s also over. We are done with big spending plans. I suspect many other people are too.

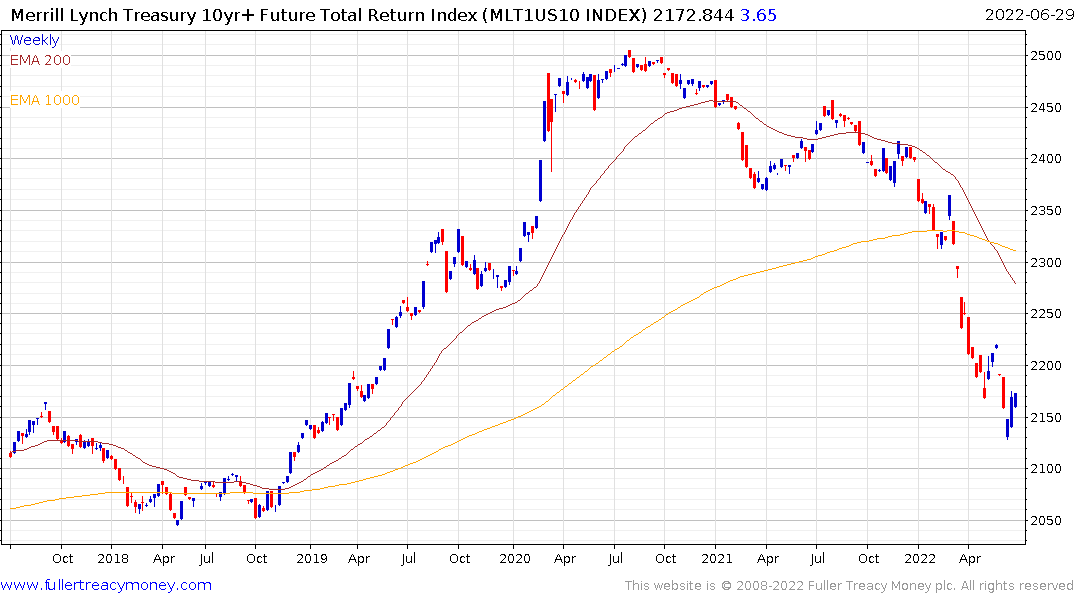

That suggests demand is going to reset. Treasury yields are back below 3%, which is lending credence to the failed upside break hypothesis.

That suggests demand is going to reset. Treasury yields are back below 3%, which is lending credence to the failed upside break hypothesis.

The total return on Treasury futures is deeply oversold and unwinding the short-term oversold condition. At least a reversionary rally is underway. If this is a change to the secular trend, the Index will encounter resistance in the region of the 1000-day MA.

The total return on Treasury futures is deeply oversold and unwinding the short-term oversold condition. At least a reversionary rally is underway. If this is a change to the secular trend, the Index will encounter resistance in the region of the 1000-day MA.

The outstanding volume of debt is an inhibiting factor to raising rates. Just as demand surprised on the upside when money supply surged, we should consider that demand can surprise on the downside when it contracts. Ultimately, the global economy should settle back into an equilibrium, with several bumps along the way.

Obviously, the repercussions of the war in Ukraine are a wild card. If Russia escalates tensions by cutting off gas supplies even more to Western Europe that will lend credence to the deep recession argument for the region. It will create a lot of economic pain, which will force technological innovation, unconventional solutions, and less demand. Berlin’s hot water energy storage tank is one recent example. https://www.washingtonpost.com/business/berlin-prepares-huge-thermos-to-help-heat-homes-in-winter/2022/06/30/8f001aca-f881-11ec-81db-ac07a394a86b_story.html

Longer-term, NATO and Russia are using up old armaments in Ukraine. That suggests a long-term cycle of modernisation and rearming is beginning. Ultimately, big debt imbalances are resolved through wars. Nothing has happened to question that conclusion.

Gold bounced back above the psychological $1800 level following an early sell-off. Traders are weighing contagion risk versus the outlook for real yields moving further into negative territory as Treasury yields contract.

Gold bounced back above the psychological $1800 level following an early sell-off. Traders are weighing contagion risk versus the outlook for real yields moving further into negative territory as Treasury yields contract.