Trick or Tantrum?

Thanks to a subscriber for this report from Algebris Investments which may be of interest. Here is a section:

Long duration has been the trade of the decade, as yields declined and curves flattened on ultra-loose monetary policy. Issuers and fund managers have jumped on the duration bandwagon: over a $1tr has flowed into income funds (IG, HY, REIT and dividend) since QE began, and corporates have taken advantage of low rates to issue ultra-long dated bonds (Brazilian oil company Petrobras issued a 100-year bond in 2015, despite having only 11 years in proven oil reserves).

However, the duration-party is now over-extended. Savings are being eroded as real interest rates are negative in most developed markets, and central bankers are struggling to purchase bonds under their QE programmes. In our view, sovereign yields need to move higher, and a market correction may be ugly. This is especially as liquidity in the bonds markets has declined since the financial crisis in 2008, further exacerbated by the rise of Exchange Traded Funds which offer daily liquidity to their investors (IMF GFSR report, October 2015).

4. More Fiscal Stimulus Is on the Way

Another source of inflation pressure will come from a shift in global fiscal policy. Since the crisis, most developed countries have kept their purse strings tight given existing public debt overhangs. However, more fiscal spending could be on the way after elections.This is already happening in Japan, with PM Abe announcing a ¥28.1tn stimulus package after a strong victory in the July Senate elections. Canada and South Korea also pledged extra budgets to step up public spending this year.

Fiscal stimulus should also come in the US after elections, where both candidates have promised more spending, and in the UK as a response to Brexit. Europe is still lagging behind, with the size and implementation of President Juncker’s investment plan underwhelming. However, there is a better chance that governments could coordinate on a spending plan after the German and French elections in 2017.

While fiscal stimulus is also not the panacea to all existing structural problems, it could complement easy monetary policy and generate some positive growth shocks. In a good scenario, it could help to normalise interest rates.

Here is a link to the full report.

Fiscal stimulus means the supply of bonds to fund government spending with increase. If central bank purchases do not keep pace, yields will need to rise in order to attract more investors into the market to soak up the additional supply. Considering how low yields are and how susceptible to interest rate hikes long duration bonds are it is at that end of the curve where the most risk resides.

The US 30-yr Treasury yield moved to an incremental new low in July but has staged an impressive rally since and is now trading above the trend mean. This is not the first time it has succeeded in rallying above the 200-day MA so it will need to hold the move if a change of trend is to be credible.

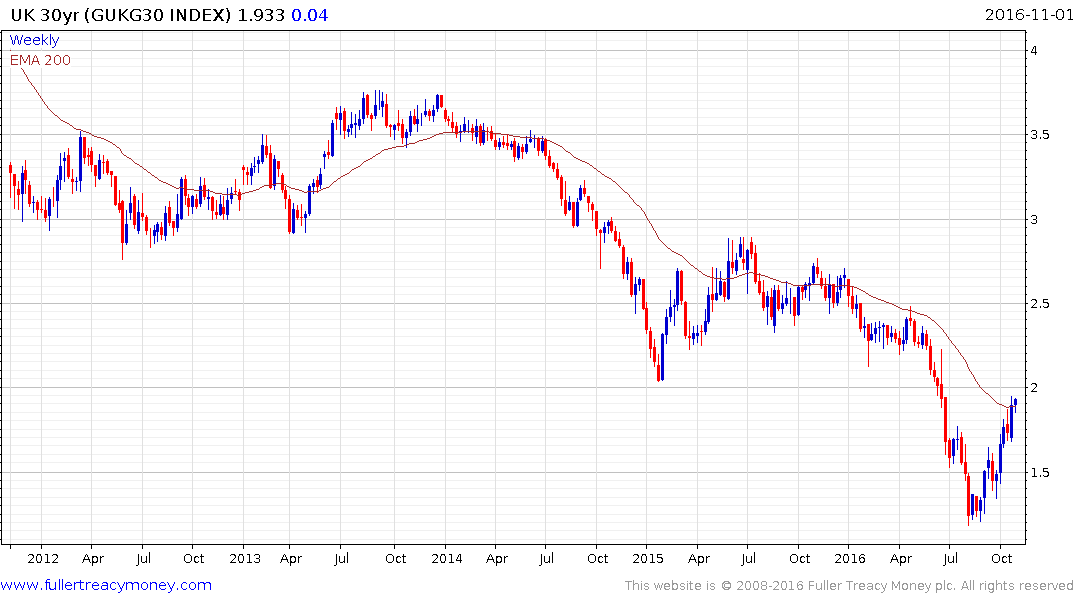

The UK 30-year Gilt yield accelerated to the August low and it has just completed a reversion back up towards the mean. A break in the progression of higher reaction lows, currently near 1.68%, would be required to question potential for additional upside.

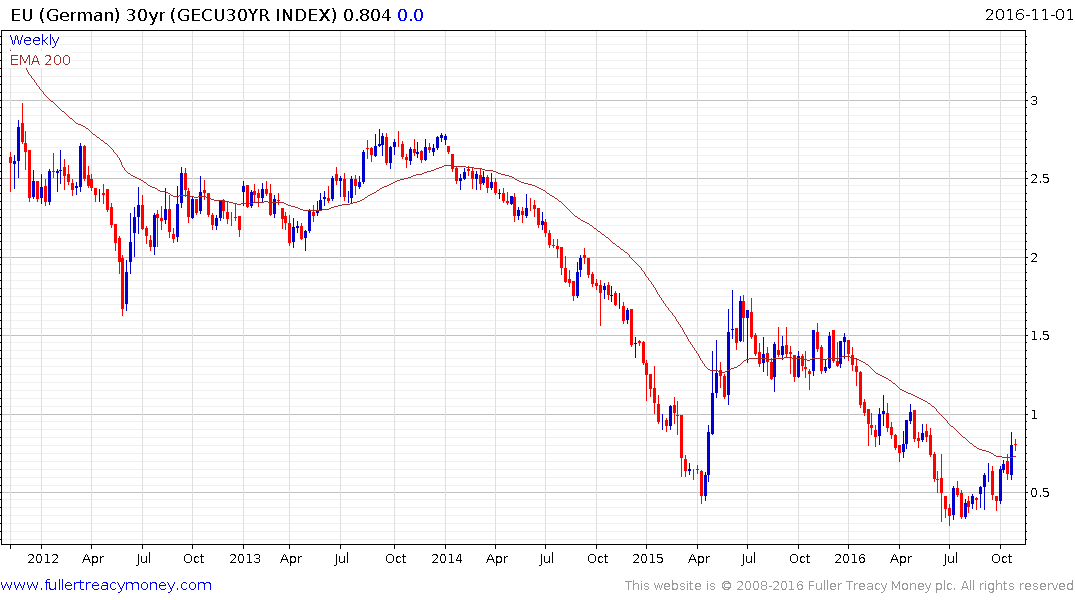

The German 30-year BUXL yield also moved to an incremental new low in July but has now staged a reversionary rally and will need to hold the four-month progression of higher reaction lows to signal a return to supply dominance beyond the short term.