Top Ten Market Themes For 2017: Higher growth, higher risk, slightly higher returns

Thanks to a subscriber for this report from Goldman Sachs which may be of interest. Here is a section:

8. Inflation: Moving higher across DM

‘Reflation’ is the theme du jour following Donald Trump’s unexpected emphasis on infrastructure spending in his acceptance speech on election night. Since then, market participants have been hard at work trying to figure out the policy agenda that Trump the president might pursue (distinct from the rhetoric of Trump the candidate). What seems clear to us, as argued above, is that economic issues, notably tax cuts, infrastructure spending and defense spending, are high on the agenda — a recipe for reflation.There was a strong case for rising inflation in the US even before Trump’s victory. Our call for higher rates in long bonds this past year was premised more on a repricing of inflation risk and inflation risk premia than on a rise in real rates. And, globally, we expect rising energy prices to push up headline CPI across the major advanced economies in early 2017. After years of deleveraging and highly accommodative monetary policy, we expect inflation to gain momentum in 2017 just as many countries are shifting their policy focus to fiscal instruments. For example, we are forecasting large boosts to public spending in Japan, China, the US and Europe, which should fuel inflationary pressures in those economies. Moreover, having had to work so hard for so long to get inflation even to the current low levels, the major central banks in developed markets sound increasingly willing to let inflation run above 2% targets.

Here is a link to the full report.

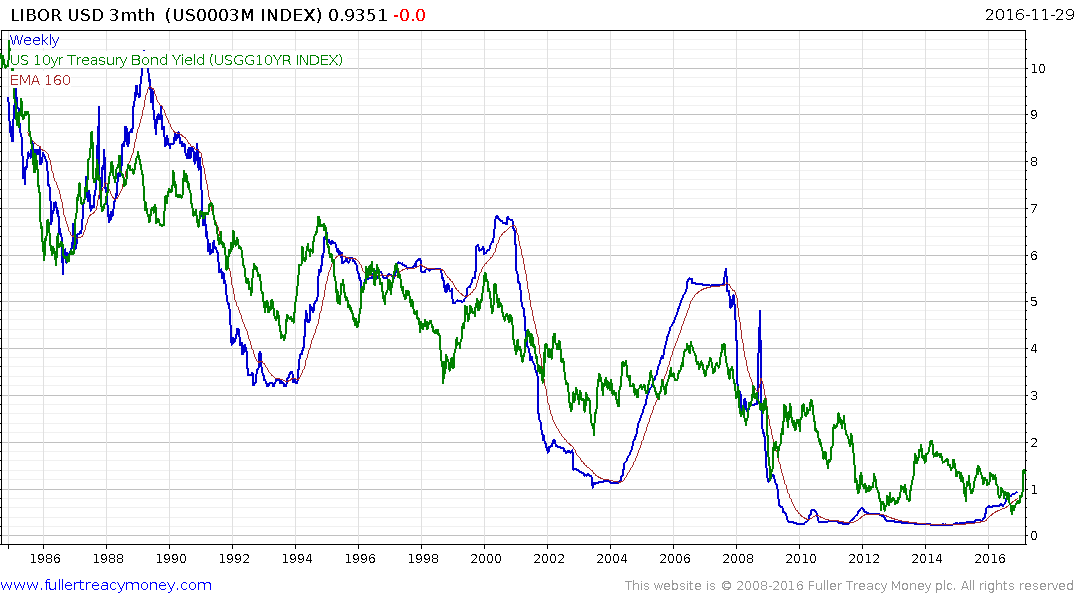

As recently as early this month a significant number of investors were betting the discount rate was never going to go up. That has definitely changed with the bond markets rapidly pricing in the potential for inflation to pick up as fiscal stimulus is expected to kick in.

.png)

3-month LIBOR has been rallying all year. The Fed’s first interest rate hike last year was a catalyst for additional risk to be priced into the rate and the reorganisation of money market funds was an additional differentiator in risk metrics.

Following the taper tantrum in 2013 yields retraced the entire advance because investors were still betting the discount rate would not move. On this occasion the market is pricing inflation in even though it has not yet been seen in statistics. Inflation figures will need to come in at least in line with expectations if yields are to be sustained at these levels let alone move higher.