Tin Prices Rise Despite Metals Rout

This article by Ese Erheriene for the Wall Street Journal may be of interest to subscribers. Here is a section:

More than half of all demand for tin is accounted for by the solder which is used to assemble electronics devices such as smartphones and televisions, according to Fastmarkets, a metal research group.

China’s appetite for tin hasn’t fallen away in the way that it has for other base metals, such as iron ore, and China is tin’s biggest importer. Although this week’s devaluation of the yuan will make the metal more expensive in the Chinese market, electronics manufacturers are likely to be well-hedged and able to absorb price rises, said Ms. Bain.

Analysts see the biggest impact on prices coming from the supply side. Indonesia is the world’s largest tin exporter, with up to 35% of the global trade. New regulation this month bans all but refined products from legal mines leaving the country.

Myanmar, whose exports took off around 2011 after the fall of the ruling military junta led to the lifting of some sanctions, is a recent entrant into the tin market.

Now, though, output from Myanmar’s main tin mine is declining due to falling ore grades, and the challenges posed by the ethnic conflict raging nearby. The recent fall in tin prices also stymied investment in current and prospective tin mines, analysts say.

The Chinese economy might not be growing as fast as it did in the early part of this century but the fact that massive investment in additional supply has reached market in the last 18 months has been the catalyst for weak metals prices. Tin has some individual considerations because of Indonesia’s dominant position as a major supplier but its price shares commonality with the sector.

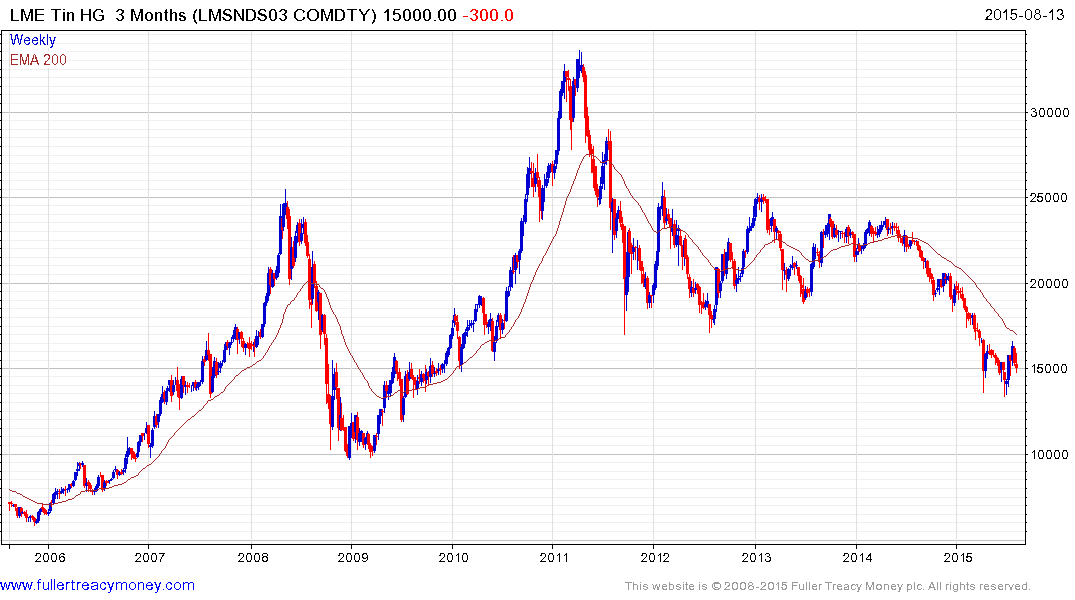

Tin lost momentum following a steep decline in 2014 but encountered resistance in the region of the 200-day MA at the end of July. The lows near $13,750 will need to hold on the current pullback if support building is to be given the benefit of the doubt.

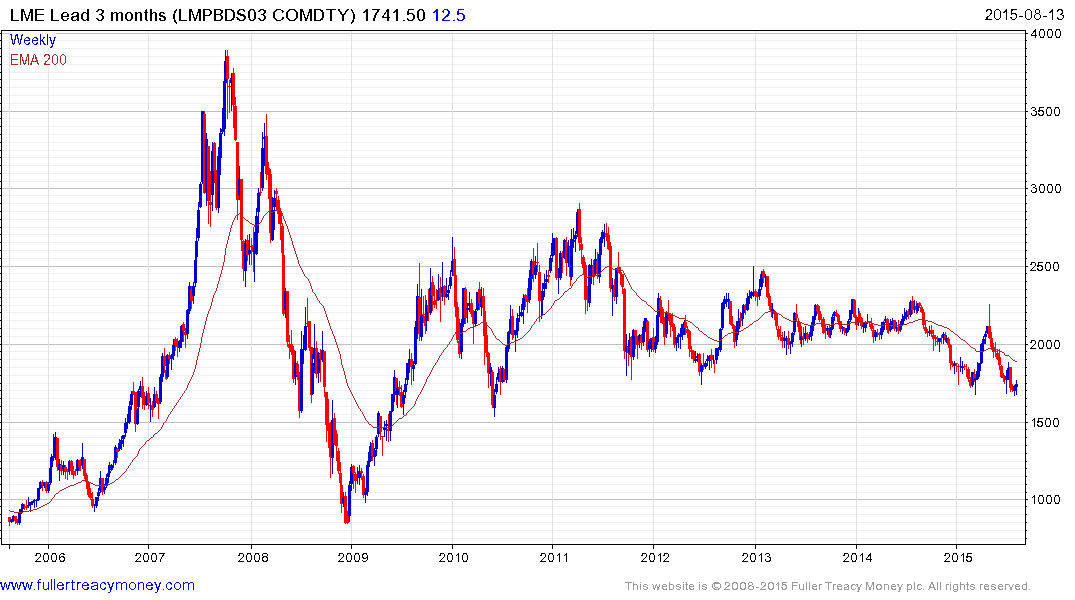

Lead is back testing its range lows of the last six years.

Zinc accelerated to this week’s short-term trough near the lower side of its medium-term range but will need to hold $1800 on a pullback to signal more than temporary support.

Aluminium has accelerated lower since encountering resistance in the region of the 200-day MA from early May. It is now somewhat overextended relative to the trend mean but a clear upward dynamic will be required to signal increased scope for a reversionary rally.

Nickel has returned to test the psychological $10,000 level which also marked the region of the 2008/early 2009 lows. A break in the yearlong progression of lower rally highs would signal a return to dominance beyond short-term steadying.

Copper has held a progression of lower rally highs since hitting a medium-term peak in 2011. While somewhat oversold in the short term, a sustained move above the 200-day MA would be required to begin to suggest a return to demand dominance beyond scope for some steadying.

We can conclude from the above charts that industrial metals have a great deal of commonalty, short-term oversold conditions are evident and some are in the region of previous areas of support. There is scope for an additional near-term bounce but there is no evidence just yet that medium-term lows have been found.

Back to top