This Is Why so Many Chinese Companies Are Suspended

This article by Tracy Alloway for Bloomberg may be of interest to subscribers. Here is a section:

Less-known is that Chinese companies have been doing the same thing by using their own corporate stock to secure loans from banks.

This means that they stand to lose a lot when those share prices start trending dramatically lower.

Says Nick Lawson at Deutsche Bank: "Stocks are being suspended by the companies themselves because many have bank loans backed by shares which the banks themselves may want to liquidate, joining the queues of margin sellers."

Nomura analysts added that: "Some bank loans have been extended with shares of listed companies put up as collateral."

?Numbers here are sketchy, but the team at Nomura estimated that the total amount of such loans may be 500 billion yuan to 600 billion yuan ($80 billion to $96 billion). This sounds like a lot but is equivalent to about 1 percent of total loans to Chinese enterprises.

If the size of loans collateralised with shares is less than $100 billion that is good news for the corporate sector. However the wider impact is more important. If a retail investor holds the shares of a company that has suspended trading and subsequently receives a margin call, they have little choice but to sell not what they want but what they can. This is contributing to the speed of the sell off and to the swift deterioration in sentiment.

The Shanghai A-Shares Index was down today but closed off its low again. In addition to companies suspending trading in their shares, government agencies are buying the shares of state owned enterprises which constitute significant weightings on the A-Share indices.

Only 23 of the Chinext Index’s 100 constituents are still trading. This Index is representative of the smaller, high growth “new economy” companies and outperformed by a considerable margin until the peak a month ago. It is now effectively shut down and convalescence once this rout has run its course is likely to be lengthy.

Meanwhile the banking index is still steady despite being weak today. Elsewhere it is worth highlighting sectors that have avoided the carnage so far.

Kweichow Moutai the nation’s largest distiller has been confined to a reasonably steady range relative to the pullback seen elsewhere. One thing in Moutai’s favour is the high absolute price of the share. When buying shares in China an investor is forced to buy a “hand” of shares. In other words the minimum order is for one hundred shares and the number of shares one can buy moves up in increments of one hundred. Retail investors tend to favour securities with a low absolute price. Moutai’s 238 yuan handle may have represented a headwind to excessive speculative interest and helped preserve it from contagion.

Two additional considerations come to mind. The first is that the depth of the pullback has unnerved investors and not just in China suggesting that the corrective phase on global stock markets will persist a while longer. China has a substantial number of tools to support its market and economy so there is potential for a swift short covering rally once the decline loses impetus.

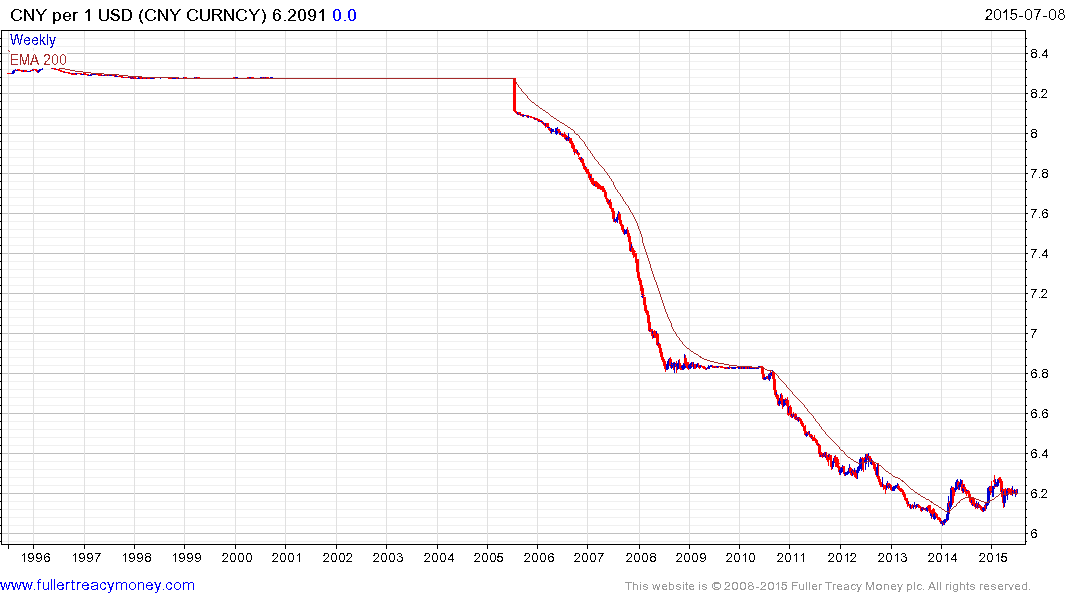

The Renminbi remains conspicuously strong. It is not beyond the bounds of possibility that China will seek a weaker currency to help solve some of its issues if the measures enacted to date do not begin to gain traction soon.

Chinese are major holders of gold. The metal is currently steady in the region of the November and March lows but a sustained move above $1200 would be required to signal more than temporary support.