This Equities Rally Is Running on Hope and a Story

This article from John Authers at Bloomberg may be of interest. Here is a section:

For the first, virtually all of the S&P 500’s gain for the year (barring this week’s surge) can be traced to the 7.5% rally from March 13 to April 13, which took it from 3,856 to 4,146. This coincided with the creation and growth of the BTFP as well as an expansion of the Fed’s balance sheet in response to the collapse of SVB and Signature Bank. Whatever the official interest rates, money was available. As money is also fungible, it had a way of finding where it could make the best return. The Fed’s balance sheet grew roughly $400 billion to $8.73 trillion between March 1 and March 22 as it tried to contain the crisis. It currently stands at around $8.50 trillion.

For the second, there was a slide in the expected federal funds rate on the anticipation that the Fed would pivot (since largely reversed). As the rally started, the projected rate after next month’s Federal Open Market Committee meeting had just dropped from about 5.5% to about 4.7%. Coinciding with this was a “defrosting of credit markets” that saw investment-grade corporate spreads compressing almost 30 basis points from this year’s peak of 163 on March 15 — again a phenomenon that was likely helped by the BTFP and increased liquidity.

Liquidity is both global and mobile. It flows to the most attractive assets and has been the driving force behind the bull market since the Global Financial Crisis 15 years ago. $87 billion has been drawn down in the Fed’s Bank Term Funding Program. That’s mostly been from regional banks requiring supplementary capital. They are still sitting on losses with long-dated bond portfolios and that situation is not improving as yields remain stubbornly high.

The Fed’s balance sheet has contracted by $280 billion since the March surge. That helps to highlight the fact liquidity conditions are tightening on aggregate even as they are easing in specific niches. The debt ceiling pantomime took a fresh turn this morning with discussions on pause. The most likely scenario remains that negotiations will go down to the wee hours ahead of a default. It’s a sorry state for politics and a needless source of potential volatility but it is reality.

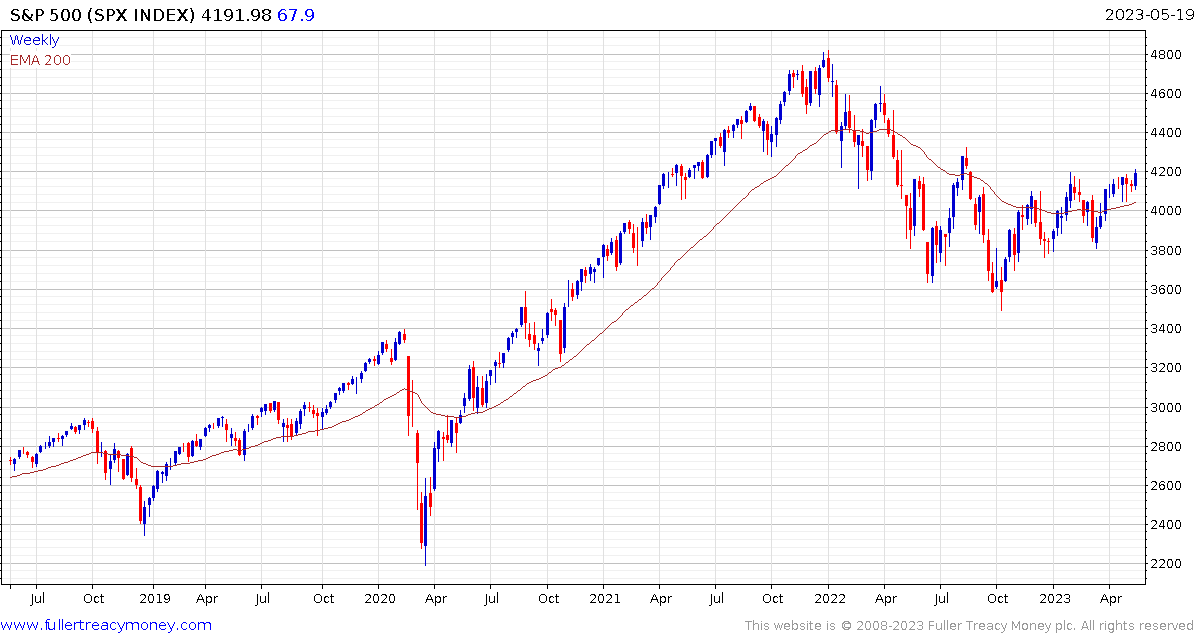

For now the S&P500 is pausing in the region of 4200. It needs to sustain a move above that level to confirm a return to demand dominance beyond the short term.