The Global Investment Outlook

Thanks to a subscriber for this report from RBC GAM which may be of interest. Here is a section on bond yields:

The arguments for higher bond yields

The global economy is experiencing a cyclical recovery regardless of the political noise, and its performance should remain the key driver of fixed-income markets over the next 12 months. U.S. data releases have been strong and the employment picture continues to improve, leading many investors to prepare their portfolios for reflation. We believe that Trump’s loosening of financial regulations should re-ignite the animal spirits that went missing after the 2008 financial crisis, creating self-sustaining economic growth. Corporate America will likely invest and hire more, pushing up the cost of capital and inflation.Aiding this momentum will be an administration stocked with business-minded department heads and White House advisors. Trump has appointed Steve Mnuchin, a former Goldman Sachs executive, as Treasury secretary and billionaire investor Wilbur Ross to head the Commerce Department. Gary Cohn, the recently departed Goldman Sachs president, is Trump’s top economic counsellor. These appointments help to validate the optimism towards streamlining regulations and promoting business investment.

A tight labour market is another source of economic optimism and will foster inflationary pressures as higher wages embolden consumers to spend more. A higher-inflation, faster-growth environment would be a departure from the slow growth mindset that has prevailed since 2012.

Assuming that the government spending materializes as advertised and stokes economic growth, we would expect yields to be pulled higher by competition for capital between Treasury bonds and businesses and individuals seeking loans. Here’s why: capital must be financed either from abroad and/or with domestic savings, and administration proposals aimed at reducing imports would increase the importance of domestic savings as a source of capital. Domestic private savers as a group tend to demand higher compensation for loans than foreign entities, potentially leading to higher rates as growth quickens.

Here is a link to the full report.

American Airlines offered pay rises of 5% and 8% for cabin crew and pilots last week. That’s well ahead of inflation and is further evidence of a tight labour market fuelling wage demands.

The big question for the bond market is how successful the Trump administration will be in mustering a fiscal stimulus. The deal to avert a government shutdown dispensed with a considerable number of Trump’s election priorities and getting the fiscally conservative wing of the Republican Party on board for deficit spending is no small task.

Right now 2-year yields at 1.25% suggest bond investors are in a “show me” mood. They are not about to begin pricing in inflation, after a decade of false starts, until they absolutely have to. It represents a text book example of an explosion waiting to happen.

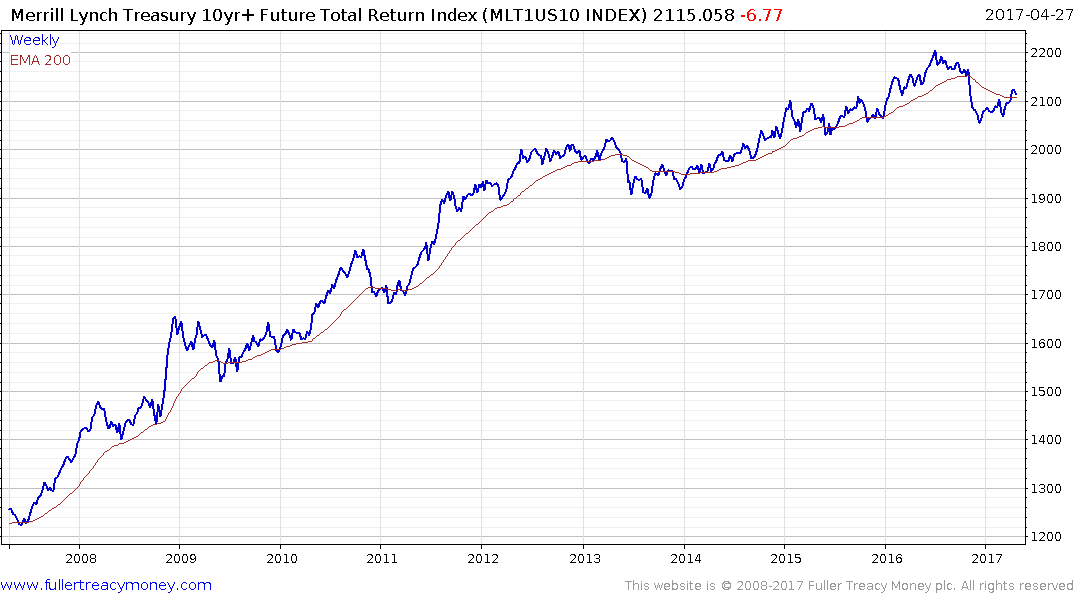

The Merrill Lynch 10yr+ Total Return Index is, in my opinion, the best barometer of the health of the secular bull market in bonds. It has so far held the break back above the trend mean, posted last month, and will need to encounter resistance in region of 2150 if the medium-term bearish outlook is to be sustained.