The End of the Incessant U.S. Big?

This article by Kevin Muir at East West Bank may be of interest to subscribers. Here is a section:

According to Bloomberg’s Brian Chappatta, Friday was the last day U.S. corporations could deduct pension contributions at the 2017 corporate tax rate of 35 percent and will now only be eligible for the new 21 percent rate.

There has been considerable debate amongst the fixed-income community regarding the amount of curve flattening that has been the direct result of corporations accelerating their pension contributions. In fact, Brian’s article is named, “The Yield Curve’s Day of Reckoning is Overblown”and is mostly a rebuke of the idea that this factor has been the driving force to the recent flattening.

I don’t agree with all of Brian’s conclusions - but hey - that’s what makes a market!

The U.S. has been flattening at a vicious pace, while most other major bond market curves have been treading water.

.png)

The yield curve spread has widened from 20 basis points to 26 over the last week. That is not enough to break the downtrend but it does suggest a moderation in the trend of curve flattening. The transition from being able to write down 35% of pension contributions to 21% is a significant evolution for corporations and it makes sense that they would accelerated contributions to plans ahead of the move. The biggest question is how many people were buying treasuries in sympathy with the view that pension contributions were supporting the market?

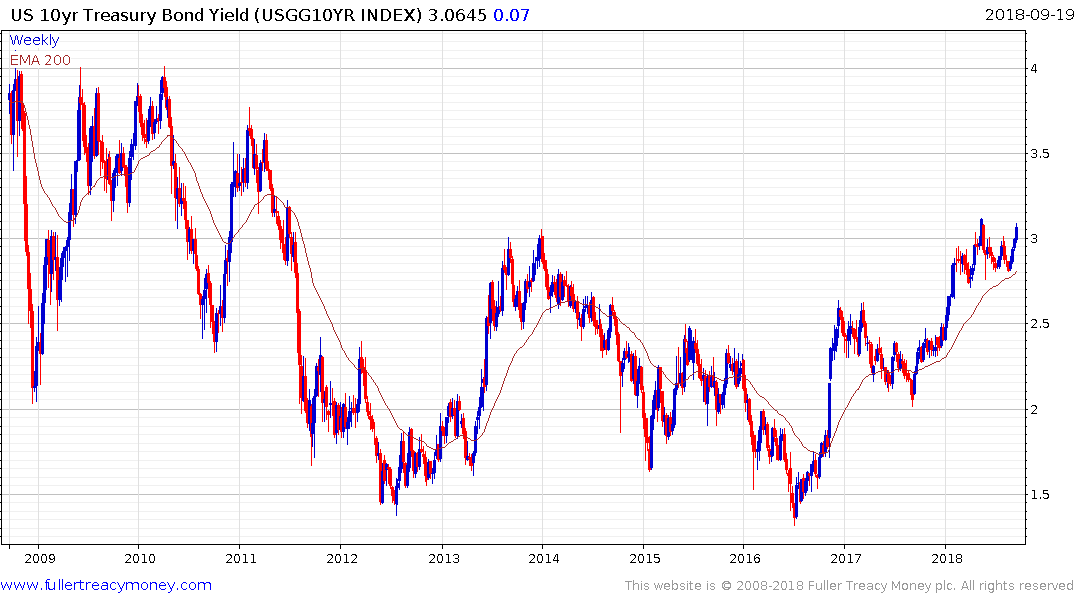

10-year Treasury yields have been ranging for much of the year between 2.8% and 3%. A range can be considered a time when the imbalance between supply and demand returns to equilibrium. That suggests the bullish and bearish arguments have pretty much cancelled one another out. The big question now is whether the move above 3% yesterday is going to be sustained?

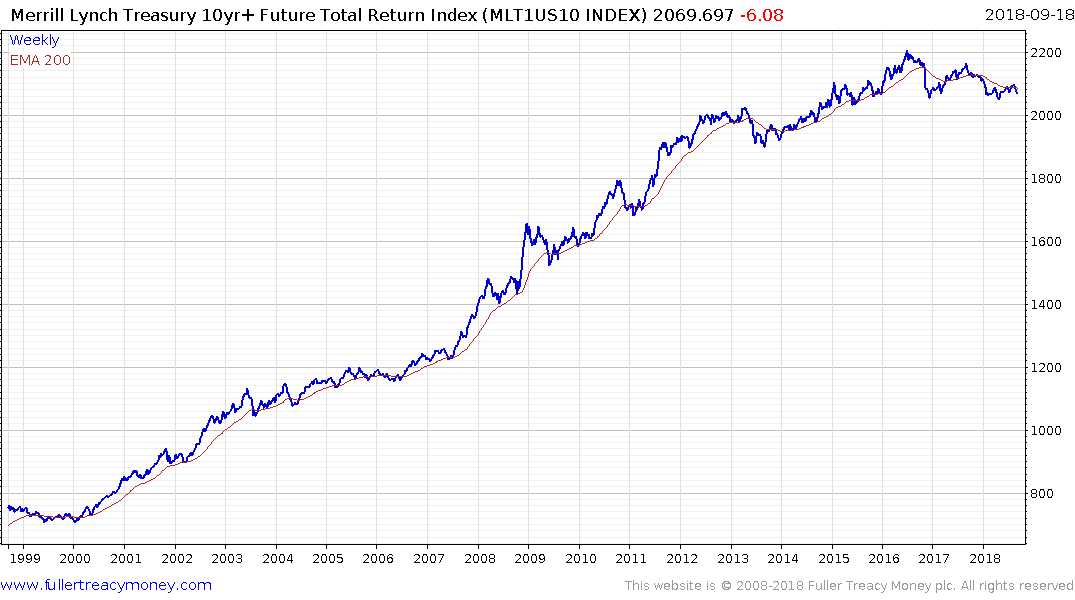

The much biggest picture is the Merrill Lynch 10-yr+ Treasury Futures Total Return Index is rolling over. When the most consistent trend in the world becomes inconsistent that sends a very clear message that the secular trend of contracting yields is on borrowed time. That suggests the path of least resistance is for higher yields.

An additional measure to monitor is the TIPS yield because there is no new supply planned. The yield has been ranging below 1% since 2013 and hit a new recovery high yesterday. A sustained move above the psychological 1% would signal a return to medium-term supply dominance.

It is easy to be mired in the minutiae of short-term moves but the bigger picture is of a secular bull market, one of the longest in history, slowly but surely ending.

Meanwhile the S&P500 Banks Index bounced impressively today from the region of the trend mean and remains in a generally consistent medium-term uptrend.