The Emerging Markets Hat Trick: Time to Throw Your Hat In?

This article by Rob Arnott and Brandon Kunz for Research Affiliates may be of interest to subscribers. Here Is a section:

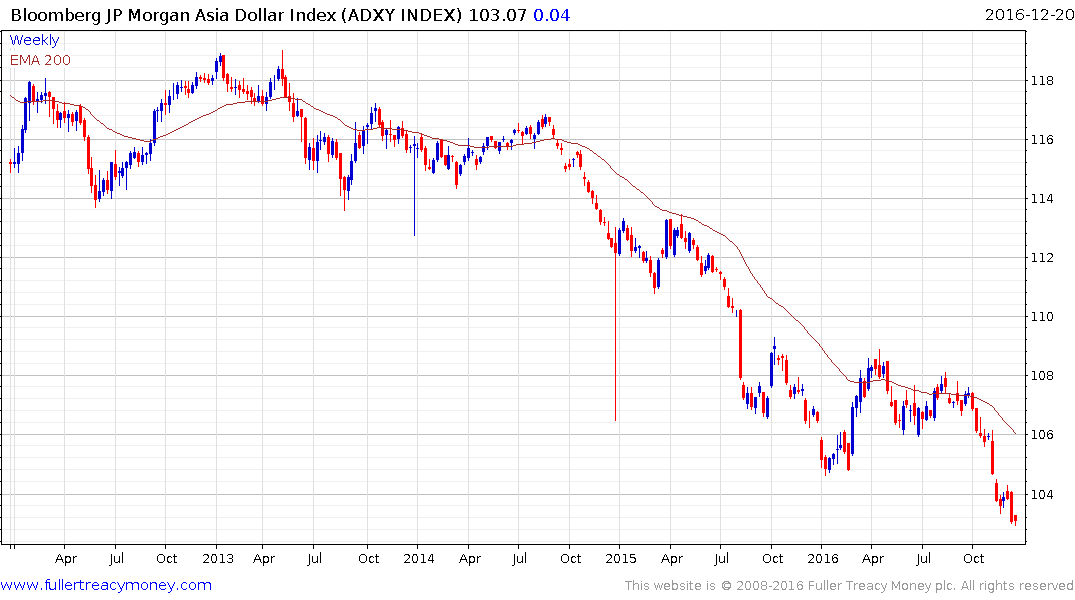

A common link between EM equities and EM local debt is the currency exposure. Based on our relative purchasing power parity (PPP) model, EM currencies tumbled from 25% above fair value in 2011 to 30% below fair value in January of this year. Even after this year’s rebound they remain about 19% cheap to the US dollar. If EM currencies’ relative valuations strengthen just halfway back to historical norms, such a move would translate into a near 1.0% tailwind to yearly returns over the next decade.

Although EM currencies, represented by the JPMorgan Emerging Local Markets Index Plus, have rebounded since January 2016, they continue to trade near the discounts associated with the 1997 “Asian Contagion” and 1998 Russian debt default. EM currencies can certainly get cheaper before they revert toward historical norms, but they might just as easily snap back quickly to fair value. Our relative PPP reversion expectations with high EM cash rates, a faster growing working-age population, and continued productivity growth as EM economies “borrow” technological advances from developed economies, all support our projected real return for EM currencies of 3.9% a year over the next decade.

The strength of the US Dollar represents a major shift in the status quo for many emerging markets, but most especially commodity exporters and comes at a time when budgets were already constrained by a multi-year bear market in commodity prices. US denominated debt has obvious risks for companies lacking substantial Dollar denominated income sources and that is likely to remain a headwind. The other side of the coin is that local currency debt is increasingly attractive for the same companies but the cost of that debt will likely rise.

The bullish case cannot be discounted because as currencies trend lower against the US Dollar competitiveness improves. Foreign investors are likely to continue to favour the Dollar as long as it is trending higher but the siren call of cheap valuations, higher yields and the potential for currency appreciation when the Dollar eventually peaks will represent a powerful catalyst for interest in emerging markets.

Between now and then the challenge of widening emerging credit spreads from what are historically tight levels needs to be overcome. Developed market interest rates have been so low for so long that many people continue to believe they will never get back to competitive levels. The risk is that inflation picks up and emerging market debt issuers are forced to pay a higher coupon in order to compete.

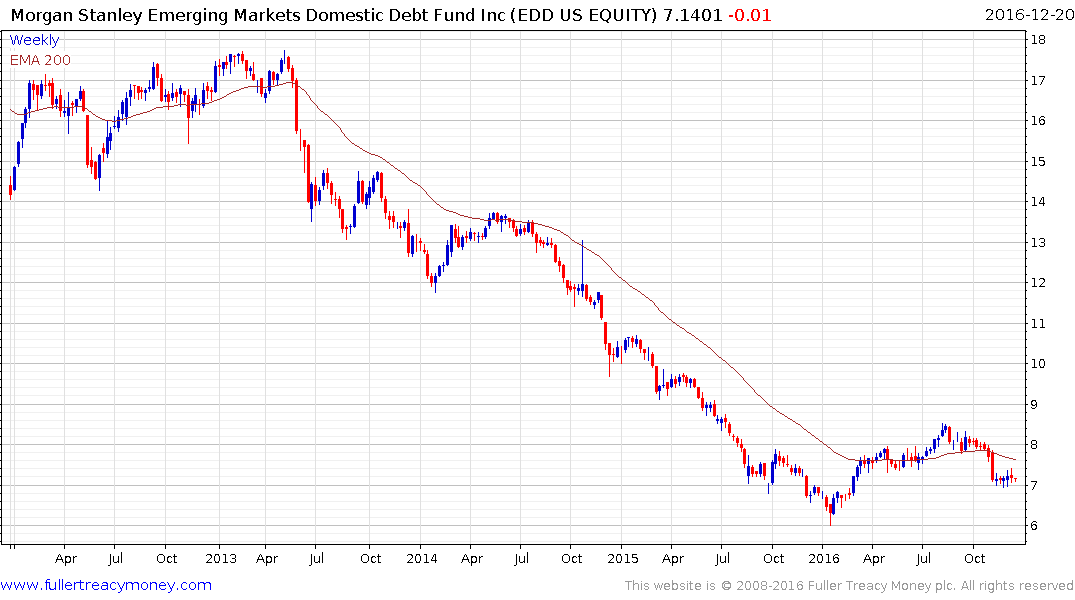

The Morgan Stanley Emerging Markets Domestic Debt Fund is trading at a discount to NAV of 13% and trended lower for three years before finding medium-term support near $6 in January. Base formation is potentially underway but a sustained move above $8 will be required to confirm a return to demand dominance beyond scope for short-term steadying.