The World Turned Upside Down

Thanks to a subscriber for this edition of John Mauldin’s note which may be of interest. Here is a section:

* the excess liquidity provided by the world’s central bankers,

* serving up a virtuous cycle of fund inflows into ever more popular ETFs (passive investors) that buy not when stocks are cheap but when inflows are readily flowing,

* the dominance of risk parity and volatility trending, who worship at the altar of price momentum brought on by those ETFs (and are also agnostic to “value,” balance sheets,” income statements),

* the reduced role of active investors like hedge funds – the slack is picked up by ETFs and Quant strategies,

* creating an almost systemic “buy on the dip” mentality and conditioning.

when coupled with precarious positioning by speculators and market participants:

* who have profited from shorting volatility and have gotten so one-sided (by shorting VIX and VXX futures) that any quick market sell off will likely be exacerbated, much like portfolio insurance’s role in a previous large drawdown,

* which in turn will force leveraged risk parity portfolios to de-risk (and reducing the chance of fast turn back up in the markets),

* and could lead to an end of the virtuous cycle – if ETFs start to sell, who is left to buy?

It’s 30-years since the 1987 crash which has likely been a contributing factor in why so many bearish reports have been hitting my desk in the last week.

These are all important points and if we look back at previous bull markets new financial innovations have tended to be contributing factors in the severity of pullbacks whether that is index futures or CDOs. ETFs, tracking just about everything, are a major financial innovation that have gutted the active management sector. That is a good thing since why should anyone pay outsized fees for below par performance? However, there are obvious imbalances being created by the mass move to passive investing since it lacks discrimination and pays little attention to valuations or earnings. Those are factors that don’t tend to matter as much in the short term as they do in the medium term and are likely to exacerbate the severity of a future pullback.

Inflation is the missing ingredient that could upset the complacency described in the above report because that would force central banks to accelerate the pace of quantitative tightening which would raise the cost of leverage and therefore reduce position sizes in automated trading systems.

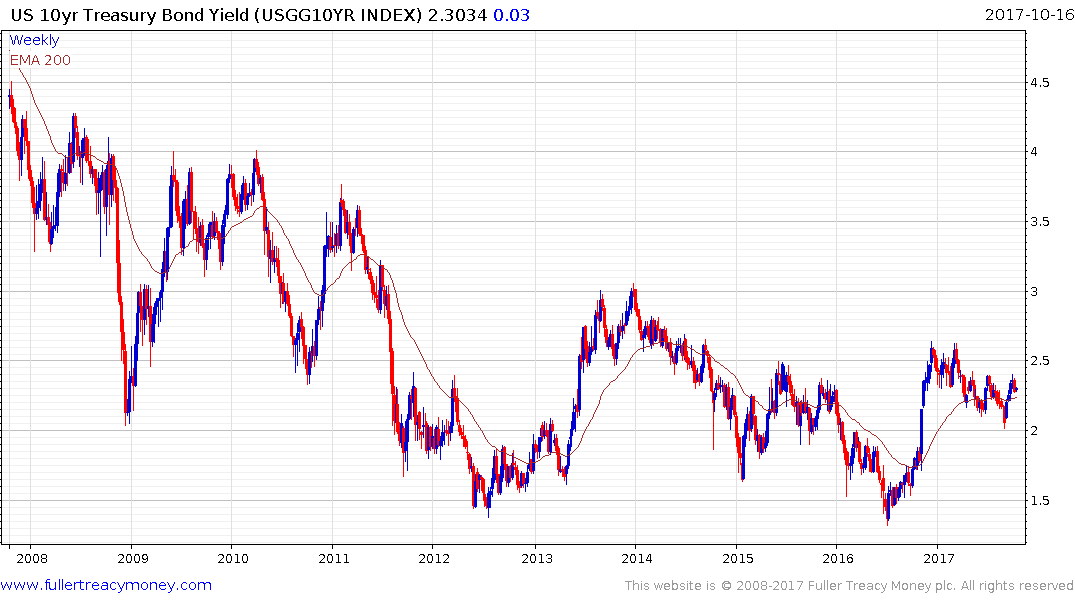

The bond market is an important arbiter on the timing of when we are likely to get a larger reaction. US Treasury yields pulled back from the 2.4% last week but steadied today. A sustained move above that level will be required to begin to suggest a return to supply dominance.