State of Venture

This report from CBInsights may be of interest to subscribers. Here is a section:

$143.9B Total funding for Q1’22. Global funding to startups reached $143.9B in Q1’22, a 19% drop compared to the record-breaking Q4’21 — the largest percentage fall since Q3'12. However, Q1’22 was still the fourth-largest quarter for funding on record and its total was 7% higher than the same quarter in 2021.

113 New unicorns. Q1'22 saw the birth of 113 new unicorns globally — a 5-quarter low and a slight drop from the 115 unicorns born a year ago in Q1'21. US and Europe accounted for most of the new unicorns, with 67 and 20 unicorn births, respectively. The highest-valued new unicorn was the US-based visual collaboration company Miro, with a valuation of $17.5B.

49% Of all funding goes to the US. US-based startups received 49% of global funding in Q1’22, with a quarterly total of $71.2B. Despite accounting for almost half of all dollars invested, Q1’22 US funding marked a 5-quarter low for the country. US-based startups also drove a significant proportion of the deal activity, accounting for 37% of all deals in Q1’22.

160% Climb in valuations. So far in 2022, companies raising new financing have gained a median valuation increase of 2.6x compared to their prior financing rounds. Median valuations of early and mid-stage deals also trended up, reaching $34M and $343M, respectively. For late-stage deals, however, the median valuation dropped to $1,054M in 2022 YTD — barely above the $1B mark crossed for the first time in 2021.

-45% Drop in public exits. The number of exits via SPACs and IPOs decreased by 45% QoQ in Q1’22, while M&A activity remained elevated with 2,983 deals in total. US-based startups accounted for 40% of all exit activity in the quarter, followed by Europe at 34%.

120 Tiger funded cos. Top investor. Tiger Global Management continued to be the most active investor in Q1’22. The firm invested in 120 companies, up from 107 in Q4’21. The largest investment Tiger participated in was a $1B Series D round to Checkout.com with 12 co-investors.

91 IPOs in Asia, more than any region. Asia led globally in terms of IPOs, which were down for every region this quarter. Asia based companies accounted for 9/10 of the top IPOs in Q1'22, including 8 China-based companies. The largest IPO came from South Korean LG Energy Solutions, which exited at a valuation of $98B.

-30% Decrease in megaround funding. Mega-rounds accounted for less total funding and fewer deals this quarter, consistent with broader VC trends. At $73.6B, total megaround funding represented just over half of all venture dollars invested in Q1'22, down from 59% in Q4'21.

71% Jump in Philadelphia funding. Quarterly funding is down across all major cities and tech hubs in the US, except for Philadelphia, Atlanta, and Dallas. Among them, Philadelphia and Atlanta based startups saw the largest jumps in funding at 71% and 30%, respectively.

20% Of funding goes to fintech. 1 out of every 5 dollars in funding went to fintech in Q1’22, despite investment in the sector shrinking quarter-over-quarter. The retail sector came second, accounting for 17% of all venture funding in Q1'22.

Here is a link to the full report.

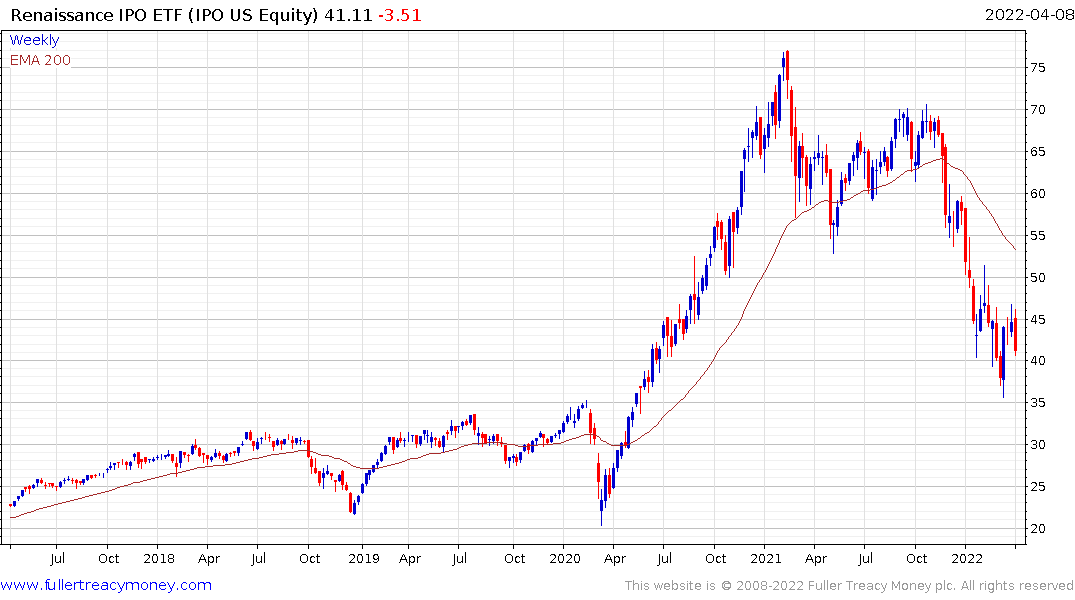

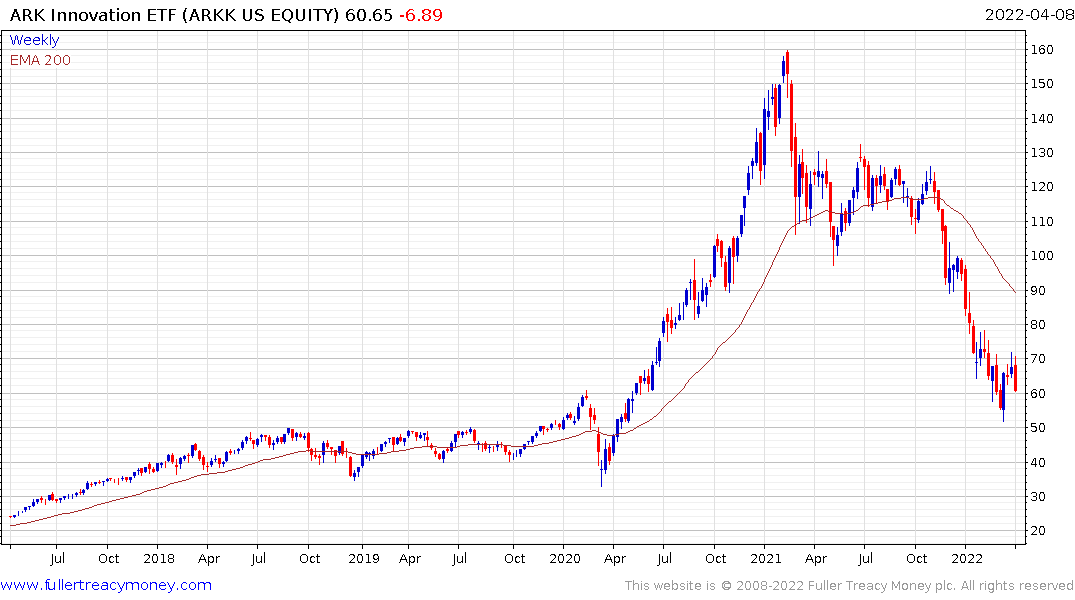

Discount rates don’t matter until they do. SPAC, IPO and every other “innovation” focused asset has experienced a deep pullback over the last six months. That’s entirely due to jumps in yields which reintroduced a discount rate to valuations.

There has been a feeding frenzy in the private markets for over a decade with large institutional funds and pensions investors coming in to pay premiums for positions in late-stage startups. That demand allowed many companies to stay private for much longer than normal. Institutions were eager to capture as much growth potential as possible before an IPO because that gave them some uncorrelated asset exposure.

In 2019, WeWork’s demise scared late-stage investors and the pace of IPOs picked up. Nevertheless, the jump in yields has begun to weigh on valuations. That suggests some of the late-stage investors like pensions are the biggest losers. Their selling of liquid assets like bonds may be part of the reason yields are surging.

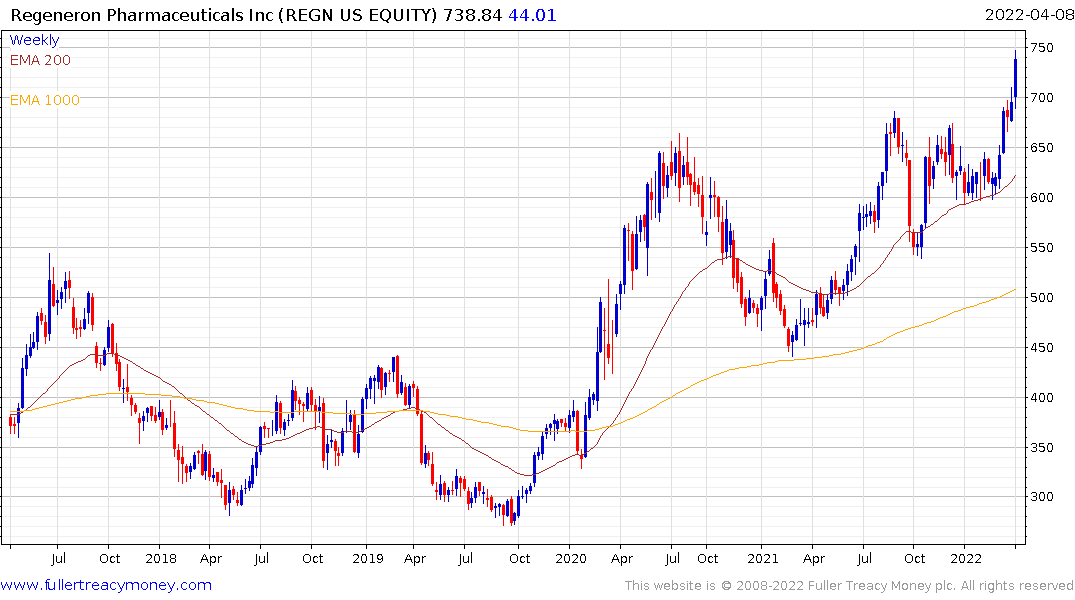

Innovation is not a myth. Small companies are cropping up all the time and trying to create solutions to problems or attempting to outcompete larger players. Talent is migrating from larger private companies to startups as potential exits are scaled back and options are worth less. As interest rates rise, competition within the innovation sector heats up and revenue growth wins out over near-term global ambitions. Growth with income will become fashionable as long as yields are rising.

At present that favouring some of the larger biotech companies like Vertex Pharmaceuticals and Regeneron.