Snap Bulls Bring on Bevy of Upgrades After Its First Beat

This article by Beth Mellor and Jeran Wittenstein for Bloomberg may be of interest to subscribers. Here is a section:

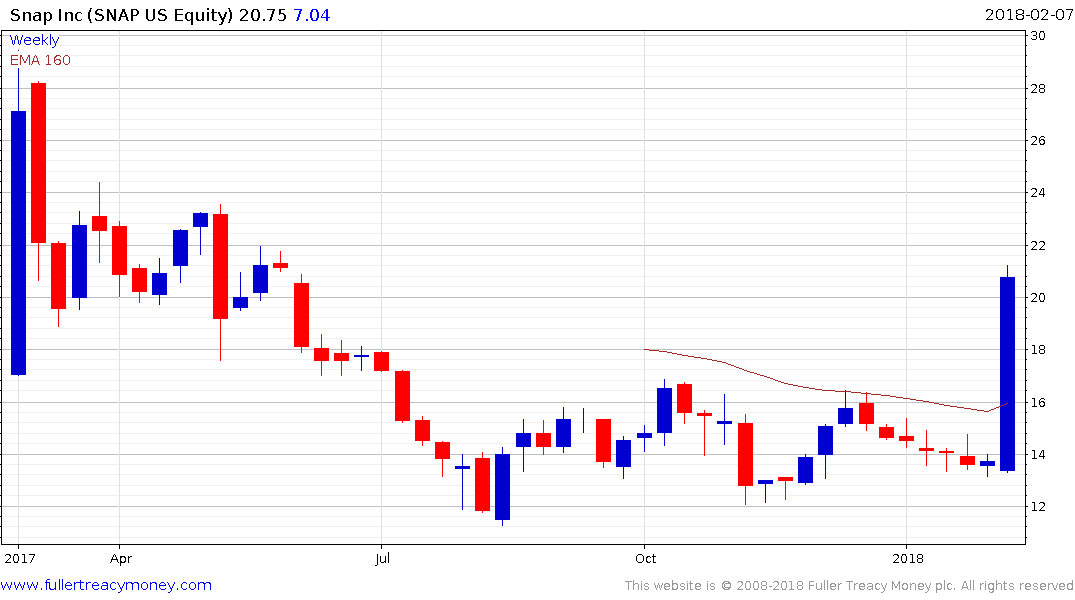

Snap Inc.’s first earnings beat as a public company, prompted at least five upgrades from analysts after the social-media company reported fourth-quarter revenue and daily active users ahead of estimates. The results blindsided short sellers who prompted upgrades from at least five analysts, and garnered a Street-high price target of $24 from Bank of America Merrill Lynch.

Analysts lauded the reacceleration of daily active user growth and advertising revenue growth, better-than-expected average revenue per user and the impact of the app redesign.

Still, some remained skeptical, with Morgan Stanley noting the potential that revenue trends could slow in 2018, while Susquehanna downgraded the stock amid competitive pressures from Facebook Inc.’s Instagram.

Snap climbed as much as 33 percent at 9:45 a.m. in New York, trading above its $17-per share IPO price for the first time since July. Here’s a roundup of what analysts are saying about Snap’s results.

Snap is used primarily by teens and tweens so it has appeal as a portal to the social interactions and advertising models of young people. Meanwhile Instagram is battling the company as it attempts to copy some of the Snap’s features while trying to appeal to the younger generation.

Snap is somewhat different to other emerging tech companies because it outsources hosting and offsite advertising while the majority other companies do that inhouse. The upshot of this policy is that it has to pay out substantial proportions of cash flow to Google Cloud Services. Today’s announcement it is losing less money than anticipated is to be welcomed but the question of whether the outsourcing strategy can ultimately be profitable remains unanswered.

Snap broke out of a five-month range today and a sustained move back below $15 would be required to question medium-term scope for additional upside.

Alphabet has closed the majority of its overextension relative to the trend mean in what is a reasonable similar sized reaction to those posted over the last eight years. It will now need to hold above $1000 if medium-term scope for continued upside is to be given the benefit of the doubt.

Facebook has been marching higher in a rhythmic manner since 2013 and is now testing its progression of higher reaction lows. There have been occasions, most notable in 2015 and 2016 when it traded below the trend mean for brief periods but it subsequently rallied powerfully following these reactions. Therefore, a sustained move below the trend mean would signal a major trend inconsistency and potential top formation.