Scrap Metal's Lament: Few Scrap

For now, supply isn't looking likely to rise any time soon.

"There's no house construction, there's no commercial construction," said Jeff Millhollin, head of scrap operations at Pacific Steel & Recycling in Great Falls, Mont. Pacific Steel has locations in seven states, from Rapid City, S.D., to Yakima, Wash.

Many consumers had already depleted any supplies of scrap that were sitting around their garages, backyards, farms and ranches in 2008, when prices for many metals were much higher than they are today, and scrap fetched even higher premiums.

Now, with unemployment high, consumers are holding onto big-ticket items longer.

"They don't throw their old stuff away," Mr. Adams said. "If they don't buy a new one, they fix the old one."

Even scrap dealers are feeling the pinch. The containers that hold scrap are often made of metal, and they can cost $4,000 to $5,000. Now, when a container gets a hole, dealers are likely to try to patch it, said Scott Sherr, the president of Diamond State Recycling Corp. in Wilmington, Del. "I don't know a scrap dealer who's ordered new containers," he said.

Eoin Treacy's view The global economy has returned to growth

and even laggards such as the USA and European countries have exited recessions,

contributing to higher demand for industrial commodities and helping to support

metal prices. This has also helped to support demand for scrap metal but this

source of supply is thinning out which could be a bullish sign for iron-ore

and steel related shares.

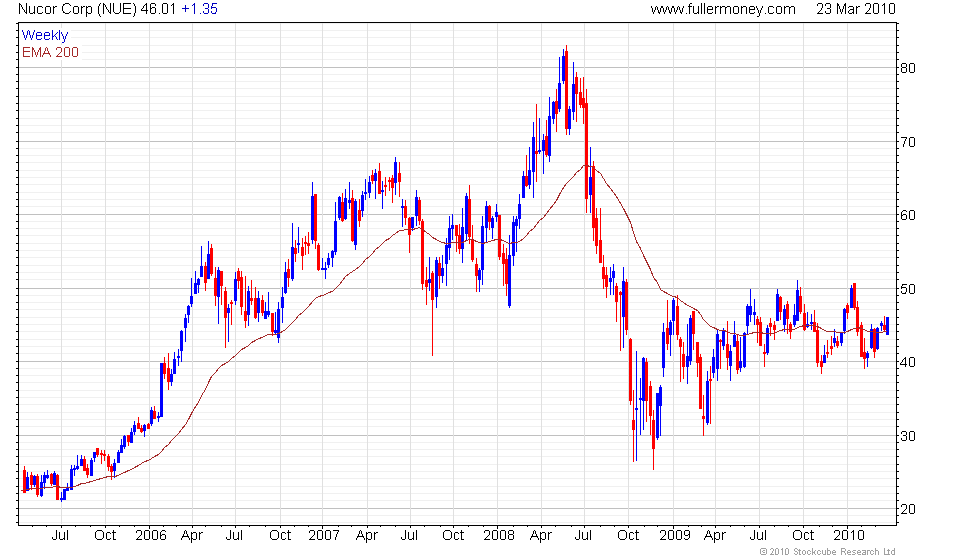

Scrap

steel companies such as Nucor, Gerdau

Ameristeel and Schnitzer Steel Industries

all bottomed in late 2008, but lost upward momentum a year ago and remain in

relatively lengthy ranging phases. The drying up of fresh supplies of scrap

has likely impacted demand for these shares and contributed to their underperformance

relative to the wider market and industrial commodity sector.

Metalico

has one of the better chart patterns in the sector and recently found support

in the region of the mean, defined by the 200-day moving average. It would need

to sustain a move below $4.50 to question scope some further higher to lateral

ranging.

There

are considerable differences in the performance of global steel companies which

would appear to be influenced by domestic stock market activity, scale, production

of niche or specialist items as well as access to energy and raw materials.

Arcelor

Mittal remains in a relatively consistent step sequence uptrend and is currently

rallying, having tested the upper side of the previous range and the mean. A

sustained move below €37 would be required to question scope for further

higher to lateral ranging.

Tenaris

posted a large weekly key reversal in late February and continues to consolidate

in the region of €15. It remains somewhat overextended relative to the

MA but the current reaction is no larger than previous congestion area trading

ranges and a sustained move below €13.75 would be required to question

the medium-term bullish outlook.

Posco

has been performing more or less in line with the wider Korean market. It continues

to consolidate above KRW500,000 and a sustained move below that level would

be required to question medium-term upside potential.

Both

Nippon Steel and JFE

Holdings remain in yearlong ranges from ¥300 - ¥400 and ¥3000

- ¥4000 respectively, Sustained upward breaks from these ranges would be

required to indicate returns to demand dominance.

United

States Steel Corp bottomed a year ago and has tripled. It found support

in the region of the upper side of the base in February and continues to rally.

A sustained move below $40 would be required to limit scope for further higher

to lateral ranging.

Allegheny

Technologies has had a smaller absolute move to United States Steel but

is currently outperforming. It moved to a new recovery high today and a downward

dynamic would be required to check momentum beyond a brief pause.

Cia

Siderurgica Nacional remains in a consistent medium-term uptrend. It recently

found support in the region of the mean and broke upwards to new recovery highs

last week. A sustained move back below BRL59 would be required to trigger an

MDL stop and begin to question the consistency of the advance.

Tata

Steel has found support in the region of the mean on a number of occasions

over the last year. A sustained move below INR500 would be required to question

scope the ranging uptrend to continue.

Bao

Steel lost momentum from August, having failed in the region of CNY10. It

continues to sustain the progression of higher reaction lows and a sustained

move below CNY7.25 would be required to question potential for additional higher

to lateral ranging.

Evraz

Group bottomed in November 2008, broke upwards from its base in May 2009

and continues to trend steadily higher. The share remains an impressive absolute

performer and moved to a new recovery high last week. A sustained move below

28p would be required to question potential for continued higher to lateral

ranging.

Of the

iron-ore miners BHP Billiton remains the

clear leader, moving to a new all time high last week. While some consolidation

in the region of the highs would not be unexpected, a sustained move below 1800p

would be required to question the consistency of the medium-term uptrend.

Rio

Tinto moved to a new recovery high today and a downward dynamic would be

required to check potential for some additional upside. A sustained move below

3000p would be needed to question the medium-term uptrend.

CVRD

found support in the region of the mean in February and has rallied back to

test the January high near BRL55. A downward dynamic would be needed to question

scope for a successful upward break.

In conclusion,

the clear leaders in the steel related sector are iron-ore producers which continue

to move to new all time and recovery highs. There are a number of steel companies

with impressive chart patterns but the degree of commonality is much less compelling

and each company needs to be judged on its individual merits. US scrap related

companies, generally, remain laggards.

{kind=link}