Precious Metals: Navigating uncertain times

Thanks to a subscriber for this report from RBC Capital Markets which may be of interest. Here is a section:

Here is a link to the full report and here is a section from it:

Central banks remain ready, willing, and able to support highly accommodative monetary policy. As part of two unscheduled FOMC meetings, the Fed has reduced interest rates by a total 150bps to 0%-0.25%, announced $1.5T in term financing and $0.7b in new quantitative easing—so far. The Fed and global central banks are positioned to continue delivering highly accommodative monetary policy. These trends extend a supportive monetary policy framework that has been in place since 2007, and reaffirm questions regarding central banks’ ability to remove existing accumulated assets, a positive for longterm gold prices. We note that in spite of extraordinary recent monetary policy easing actions and proposed expansionary fiscal policy, real rates and the US dollar have demonstrated material strength, both headwinds for gold (slides 10 & 12).

• Poor liquidity and deflation risk are short-term factors for consideration. Despite strong physical gold demand and a supportive policy backdrop during the 2008 crisis, gold prices declined in part due to margin selling as evidenced by the futures market (slide 26), in our view a function of reduced liquidity. Today, net long futures positioning is near all-time highs and represents a short-term risk (slides 27-28). Separately, the immediate implications of COVID-19 introduce reduced inflation and potential deflation risks, a consequence of declining consumption, delayed growth, higher unemployment, and higher savings rates. These factors are negative for various assets, including gold, but could be counteracted by successful stimulus measures and the effect of behavioral changes that accelerate economic recovery. With improved visibility that potential liquidity-related gold selling has abated, and virus countermeasures more well-understood, the short-term outlook has the potential to improve.

• Despite neutral YTD gold price performance, gold equities have performed poorly. Year-to-date, gold prices have increased 1% while gold equities have declined by 21%. At current spot gold prices, North American gold equities generate a FCF/EV yield of 5.1% in 2020, compared to the S&P500’s 4.7%. We highlight current underlying S&P500 estimates reflect aggressive YoY growth estimates (slide 16), despite a risk of declines under a potential recession scenario. We continue to highlight gold equities have delivered positive structural changes, including balance sheet repair and improved operating costs, where we calculate financial liquidity risks are unlikely to emerge today, absent gold price declines below $1,200/oz (slide 40). We calculate the relative valuation merits of the sector could be eroded, should gold prices decline below $1,400/oz (slide 38).

.png)

The Dow/Gold ratio has clearly broken its decade-long uptrend. In the last month it has broken below the 1000-day MA. That’s a monumental event because it has never happened in a secular bull market before. This has been achieved by the gold price going nowhere while the stock market has collapsed by approximately 30%

.png)

The question that should be front and centre today is whether the bull market, as in the secular bull market, is over. Is this a major market top rather than a medium-term top? I suspect we are somewhere in between because equity bear markets are usually associated with energy bull markets and that is not looking likely. The bigger question is about the likelihood of helicopter money.

The problems with companies having built up debt loads in service to buying back shares represents a significant issue when the hollowing out of balance sheets. With no income coming in the buyback party is over. That lays bare the value of options, management teams have accrued, while the financial health of companies has deteriorated. The corporate bond market totals $10 trillion and very little is held by dealing desk because of regulatory constraints. So, we have an illiquid market on the cusp do downgrades into junk which is even more illiquid. That means buybacks are no longer going to be a support for the market.

![]()

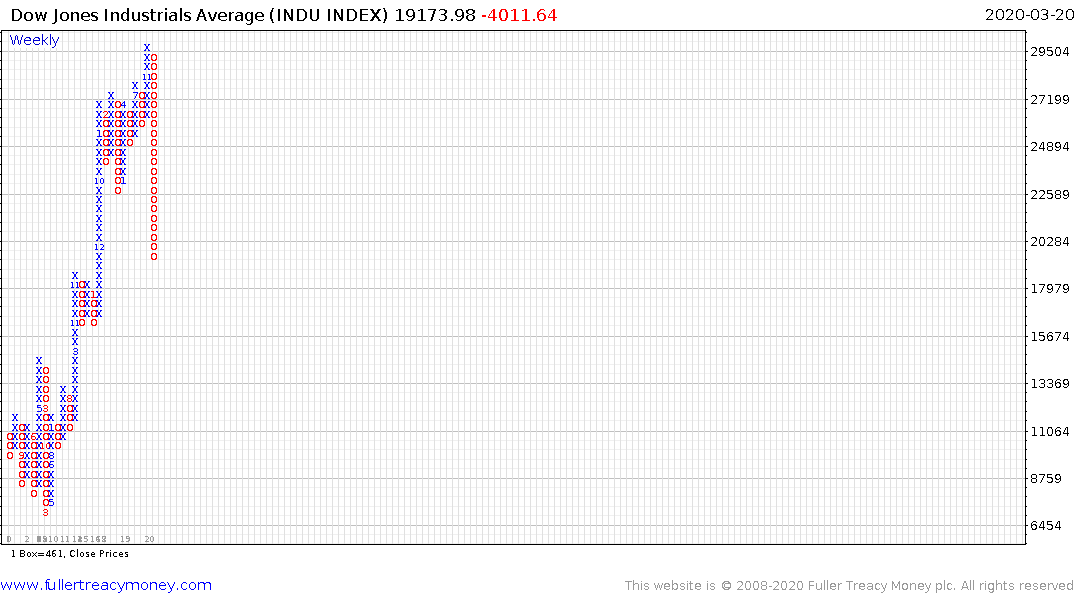

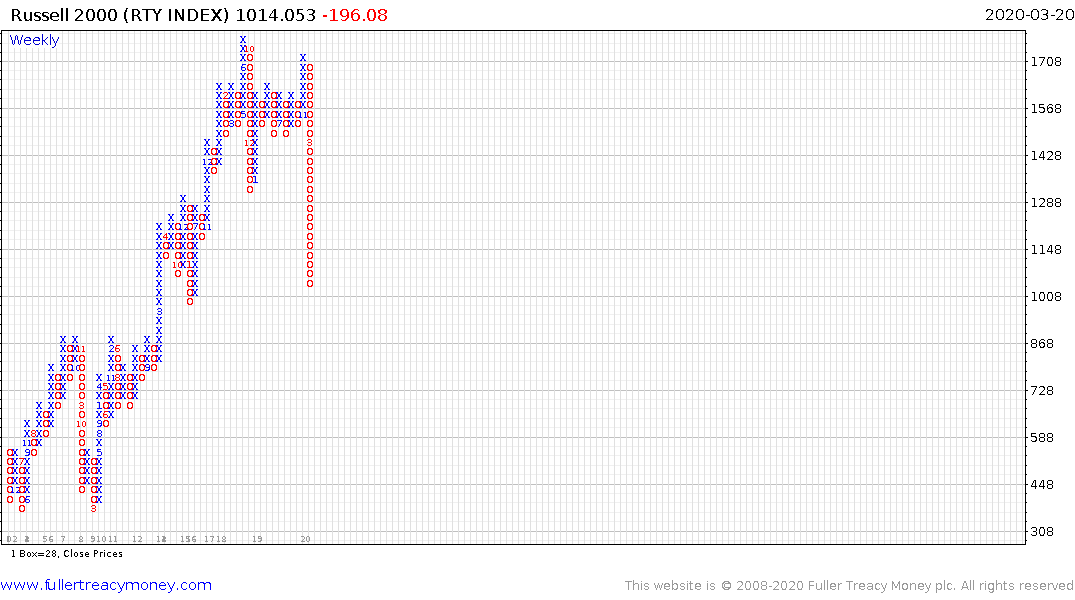

The Dow Jones Industrials Average is trading well below the 1000-day MA. So is the Transportation Average. So is the Russell 2000.

Investors are concentrated in “large cap equity” sector. That is a euphemism for the FAANMGs. The Nasdaq-100 is the only one of the main indices that has not broken below the 1000-day MA. Many of the big tech companies have abundant cash, do not buy back shares, are founder managed and are less impacted by declining foot traffic.

The unappreciated risk these companies face is their provision of cloud services to loss making companies. There are obviously going to be some that benefit from the more demand for working at home and cybersecurity but venture funding drying up sets the clock ticking on cash burn rates for startups who are among the biggest clients of cloud service providers.

My biggest concern right now is there is an almost pervasive willingness to buy the dip. That is not how markets bottom. Instead people are usually completely disillusioned by a decline and are unwilling to participate because they are too afraid of additional losses. We are not there yet.

Back to top