How £170 Bln of Energy-Aid Could Upend BOE's Outlook

This article from Bloomberg may be of interest to subscribers. Here is a section:

According to a Bloomberg News report, Truss has drafted plans to cap annual electricity and gas bills for a typical household at or below the current level of £1,971 ($2,300). That would have a significant impact on inflation, which our baseline scenario forecasts will reach 15% in January. Mechanically inputting the cap freeze into our forecast shows inflation peaking in July (at 10.1%) and then falling back at a faster pace -- approaching 2% within a year.

The cost of implementing that measure would be a whopping £130 billion over the next 18 months, according to Bloomberg News. If we then add fresh support to businesses, which may total £40 billion based on draft government plans, the full size of the package could reach 7% of GDP. That’s a massive fiscal boost, close to the level of government support seen during the pandemic.

But it’s early days. There’s a high probability that the reported plans will face significant push-back from the Treasury or from within the Conservative Party -- especially as these measures would be poorly targeted. A key question will be how the energy cap is funded. It could be clawed back from households later, keeping energy prices higher for longer, or purely financed by government borrowing. The latter option would create a significant hole in the government’s finances -- even if the cap delivers around £30 billion of savings from lower inflation-linked debt payments in 2023-24.

Another possibility is the government intervening in wholesale energy markets. That could dampen the impact on the public finances, because it would open up the possibility of reducing bumper profits from some electricity producers. The snag here is it would be akin to a windfall tax, which Truss has previously said she would not pursue.

7% of GDP is a lot of money to spend on standing still. The fact the £170 billion price tag coincides almost identically with the excess profits for energy companies quoted last week. It suggests the government is aware of what sector can be targeted should financing this stimulus become an issue.

The important consideration is price caps quickly bring down headline inflation. Historically, caps kill supply growth because companies will not invest at unprofitable levels. That’s why inflation tends to rebound instantly when they are abandoned. It is also why onerous windfall profits are counterproductive. However, without windfall taxes, much of the price cap funding will be a fiscal transfer to energy companies which implies higher taxes for consumers.

Liz Truss continues to double down on her claim to cut taxes. That’s going to put upward pressure on interest rates. Spending on this scale during an inflationary period tends to be punished by investors. Gilt yields lurched to a new high today, above the psychological 3%.

Liz Truss continues to double down on her claim to cut taxes. That’s going to put upward pressure on interest rates. Spending on this scale during an inflationary period tends to be punished by investors. Gilt yields lurched to a new high today, above the psychological 3%.

The FTSE-250 is steadying in the region of the March and July lows.

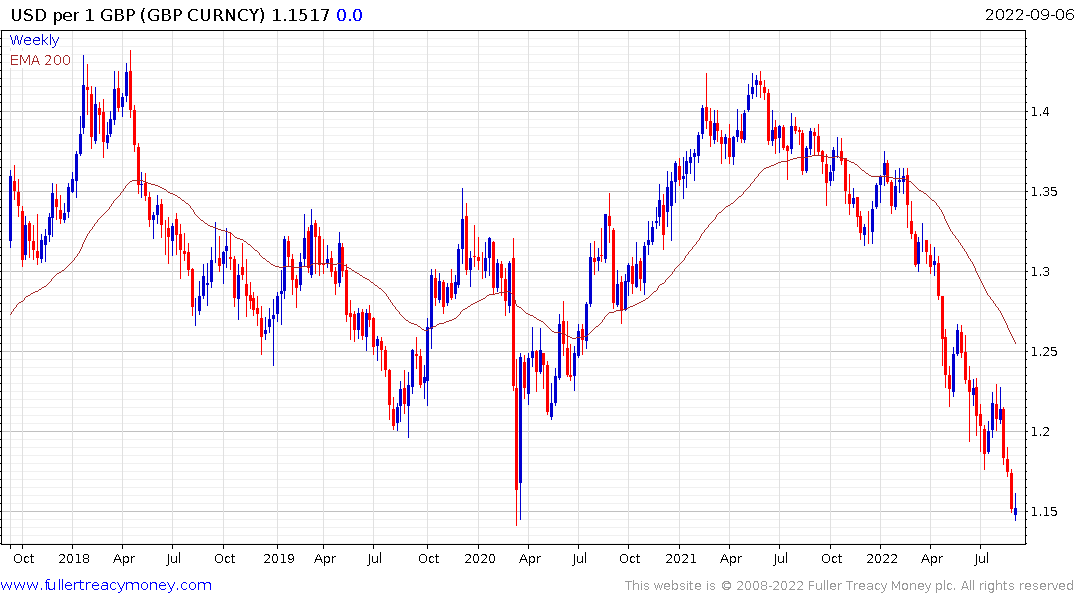

The Pound has found short-term support versus the Euro but remains in a consistent downtrend against the US Dollar.

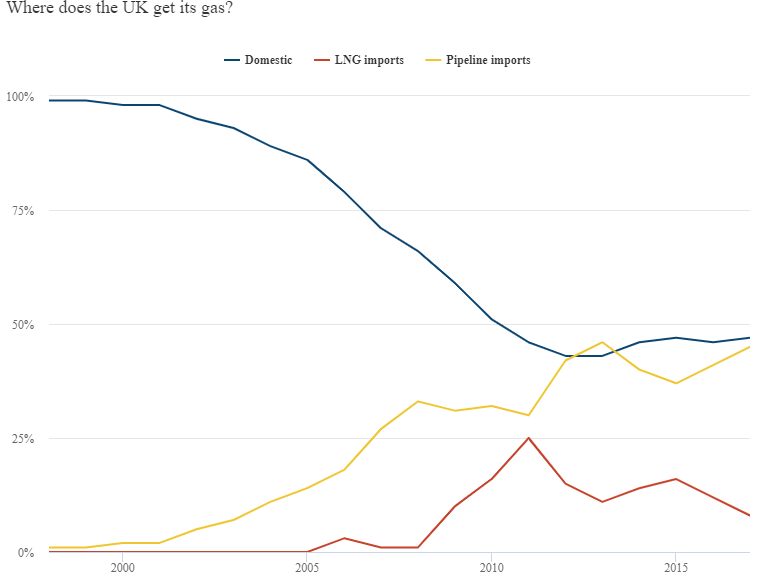

The end of energy independence with gas peaking in the early 2000s, oil in 2005 and electricity in 2010 is the big long-term challenge. The only way the UK is going to get back to a position of relative strength is to solve the energy problem.

Boris Johnson was in favour of existing nuclear and new nuclear. There are geothermal deposits in Cornwall, shale deposits in the old coal fields and renewables have already cut demand for gas over the last decade. Concurrently, there are plans to build a thousand-mile cable to transport solar electricity from Morocco. One way or another, cheap domestic energy is a prerequisite for improving living standards and improving industrial productivity. .

Boris Johnson was in favour of existing nuclear and new nuclear. There are geothermal deposits in Cornwall, shale deposits in the old coal fields and renewables have already cut demand for gas over the last decade. Concurrently, there are plans to build a thousand-mile cable to transport solar electricity from Morocco. One way or another, cheap domestic energy is a prerequisite for improving living standards and improving industrial productivity. .