The Credit Strategist

Thanks to a subscriber for receiving permission to post this edition of Michael Lewitt’s ever interesting report. Here is a section on junk bonds:

Junk bonds may be rallying but it has little to do with corporate credit quality, which keeps deteriorating. As of the end of August, 113 companies had defaulted on their debt in 2016, already matching the total number of defaults from 2015. The year-to-date default count was also 57% higher than a year earlier. In case anyone is paying attention (it appears they are not), the last time defaults were this high was in 2009 when 208 companies failed during the financial crisis. Standard & Poor’s is now projecting that the annual default rate will hit 5.6% by June 2017 with 99 junk-rated companies expected to default in the 12 months ending June 2017. That would significantly exceed the 79 U.S. companies that defaulted in the previous 12-month period ending June 2016, which resulted in a 4.3% default rate. While low oil prices are a major contributor to this ugliness, energy companies only accounted for 57% of the defaults in the 12 month period ending in June 2016. That means that there is plenty of distress to go around

Even more disturbing is the fact that defaults are rising rapidly while many leveraged companies continue to enjoy low borrowing costs courtesy of the Federal Reserve. If interest rates were remotely normalized, the default rate would already be well above 5% and heading to the high single digits. None of this appears to bother investors, who are chasing yield in the rare places they can find it, which is always in all the wrong places. As a result, the normal spread-widening that occurs when defaults spike is not occurring, which is a very unhealthy phenomenon because it signals high levels of risk-taking and complacency on the part of investors.The history of the modern junk bond market teaches that most returns are earned in compressed periods after the market suffers a sharp sell-off. The rest of the time, investors are pushing water uphill as they invest in securities that offer poor-to-mediocre risk-adjusted returns until the point when the bottom falls out and they suffer catastrophic losses. There is good reason why very few credit hedge funds or other large investors made any money in junk since mid-2014, when the market began a sharp sell-off that coincided with the slide in oil prices and the slowdown in China. This sell-off ended early this year when the market began to rally based on the realization that the Federal Reserve lacks the intellectual capacity to understand the consequences of its own policies or the moral courage to change them. But investors are chasing zombies because numerous companies are not generating enough cash flow to reduce their debts or repay them when they mature. Instead, they are just living on fumes and waiting for the day of reckoning when their debt matures and they can’t pay it back. More of them will hit the wall when their debt comes due and they can’t refinance it at a reasonable interest rate because they are financially infirm. Standard & Poor’s is telling us that more of these companies are heading to the boneyard. Investors should be selling rather than buying this risk.

Here is a link to the full report.

I don’t think there is any argument that central bank measures to inflate asset prices through, previously unimaginably, low interest rates and outright purchases of bonds have had a distorting effect on asset prices. In fact that was the whole purpose of the policies in the first place. After-all quantitative easing was conceived to avoid an even more calamitous crash and succeeded on many fronts. The problem is that we are now more than seven years into an era of extraordinary monetary policy and the self-sustaining robust growth that could upend dire warnings of overvaluations has been slow to appear. In fact because much of the G7 is contending with weak growth the extent of the dislocation in valuing bonds has increased.

Perhaps that’s the most important point. A bubble is inflating in the bonds markets. Negative yields are a nonsense, yet investors are falling over themselves to buy them. In fact this is one of the most important characteristics found in all bubbles. Crowds are tolerant of contradiction. When the bubble bursts, and it will eventually burst, investors will look back and think how they could ever have been so silly. As investors we have to ask an even more relevant point which is whether the bull market is over?

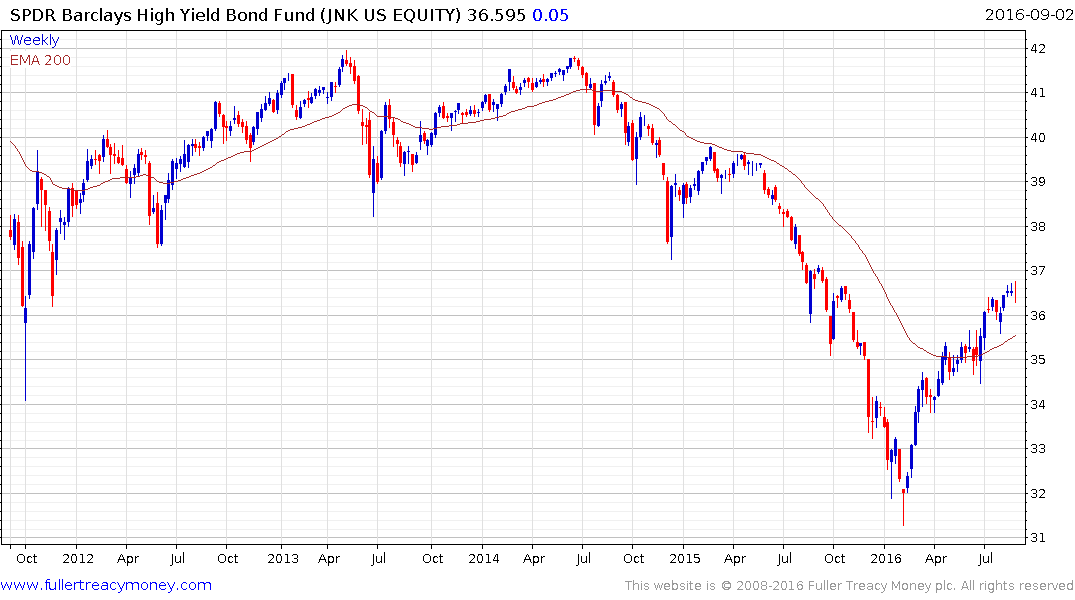

The dislocations occurring in valuations are truly troubling but we cannot yet conclude the bond bull market is over. The $12.4 billion SPDR Barclays High Yield ETF (JNK) accelerated to its February low and has rallied along with oil prices to trade back above the trend mean, even though it does not hold a large number of energy holdings. A break in the progression of higher reaction lows would be required to question the consistency of the rebound.

Back to top