PE Daily: Private Equity's IPO Boom

This article from Dow Jones may be of interest to subscribers. Here is a section:

Private-equity firms are taking portfolio companies public at record levels, capitalizing on a highflying market as the economy rebounds from the pandemic-induced recession, Maria Armental reports for WSJ Pro Private Equity. In all, 105 private equity-backed companies priced initial public offerings in the U.S. in the first six months of this year, according to data provider Dealogic. The total has already surpassed the 89 U.S. IPOs by sponsor-backed companies in all of last year and is more than triple the number of such exits in 2019.

Midmarket-focused Nautic Partners aims to raise $2.5 billion for its 10th buyout fund, Preeti Singh reports for WSJ Pro Private Equity, citing a public document from Rhode Island's public pension system. If the Providence, R.I.-based firm hits its target, Nautic Partners X LP would be about 60% larger than its predecessor, Nautic Partners IX LP, which closed with almost $1.57 billion in March 2019. The fund's sponsor is expected to commit as much as $100 million to the new pool, documents from the pension system and its investment consultant said.

Ordinary people would have a way to join the wealthy as investors in private-equity funds under a proposal from two members of the House of Representatives, part of a wave of recent government efforts to expand access to alternative investments, Chris Cumming reports for WSJ Pro Private Equity. A bill introduced in the House on June 30 by Rep. Anthony Gonzalez (R., Ohio) and co-sponsored by Rep. Gregory Meeks (D., N.Y.) would amend the Investment Company Act of 1940 to prohibit limiting the amount a closed-end vehicle can invest in private funds.

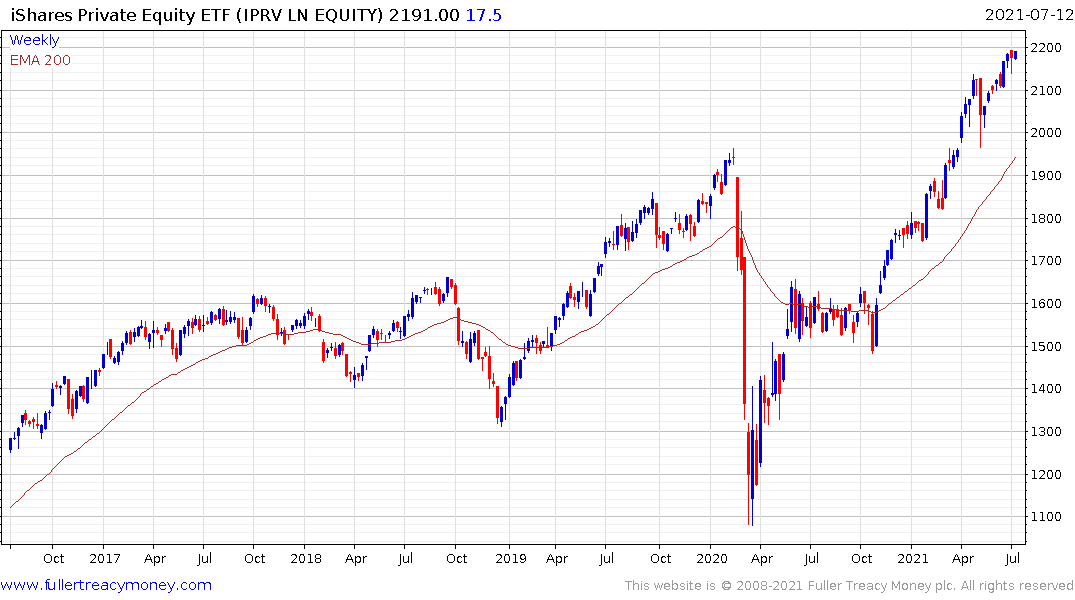

The decline in real yields have been the single biggest factor in the success of private equity. Investing in companies that will not turn a profit for years is a lot easier when the cost of funding is both low and falling. That ensures that debt can be refinanced at successively lower rates and the time to profit can be pushed out even further. That also allows valuations to increase as the enterprise value of the company jumps.

Since correlation tends to increase with liquidity, private assets are attractive in modern portfolio theory because they are illiquid. The failure of WeWork and the strife that caused for the Vision Fund, alerted the whole sector to the law of big numbers. For a private company to truly justify a valuation of $100 billion it needs revenues and profits. It’s much better to list than face the pressure of failing in sourcing a multi-billion revenue raise. The result is that many companies with no real prospect of profitability are listing in record numbers. There will of course be some that succeed but careful evaluation is required to tell the difference.

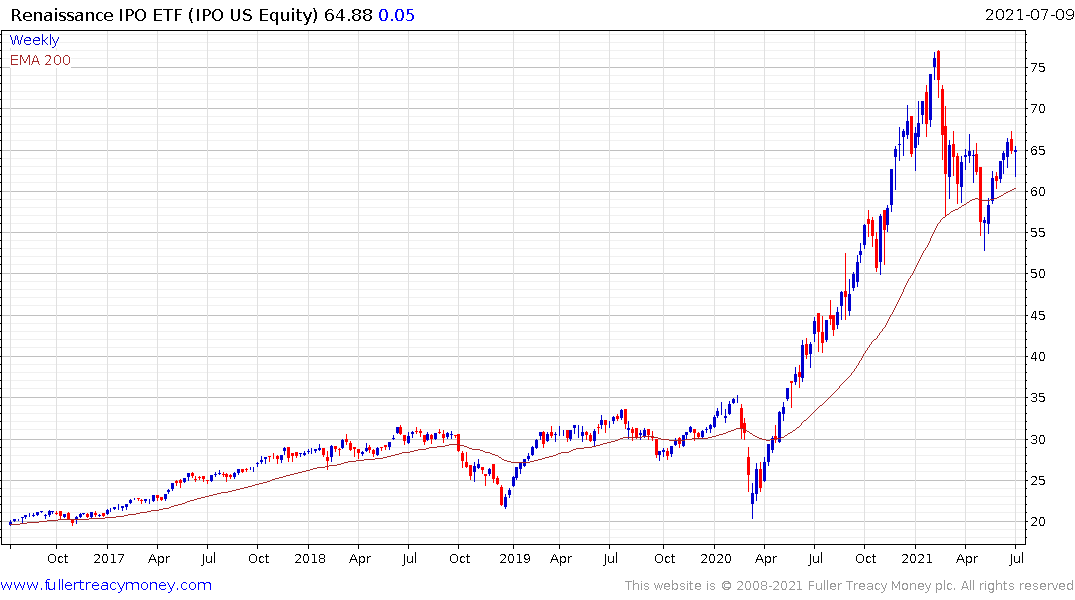

The Renaissance IPO ETF continues to pause in the region of the trend mean.

The big question for the private equity sector is how long the downtrend in bond yields will persist? With established private equity holders eager to sell and retail investors looking to make up lost ground, there is cause for caution. If bond yields fail to breakout, then long duration assets will be fine.

The big question for the private equity sector is how long the downtrend in bond yields will persist? With established private equity holders eager to sell and retail investors looking to make up lost ground, there is cause for caution. If bond yields fail to breakout, then long duration assets will be fine.

However, the 10-year Treasury continues to firmed from the region of the trend mean and a sustained move below it will be required to question the medium-term recovery. That at least raises questions about investing in long duration illiquid assets at this stage of the cycle.