PBoC cuts RRR to avoid over-tightening

Thanks to a subscriber for this report from Deutsche Bank which may be of interest. Here is a section:

The PBoC announced it will cut reserve requirement ratio (RRR) by 1 ppts for most banks by next week. RRR will be reduced to 16% for big banks and 14% for mid and small banks (Figure 1). This will inject some 1.3tn new liquidity into the banking system. Banks are asked to pay off some 900bn balances from the medium-term lending facility (MLF) on the same day. Net liquidity injection of about 400bn will largely go to small city and rural banks. Lastly, the PBC asks these banks to use the new funding mainly for lending to small businesses.

We believe the RRR cut should not be seen as a change of monetary policy stance. The economy is doing well; growth stayed strong at 6.8% in Q1, supported by consumption and property investment (see our note here). Hence there is no need to loosen monetary policy. Indeed the OMO rates were raised just last month (Figure 2). We do not expect PBC to cut policy or OMO rates in the coming months. If anything, OMO rates may be raised further.

The main purpose of the RRR cut, in our view, is to avoid over-tightening on small banks and small businesses. The PBoC will continue to tighten financial regulations and deregulate interest rates under the leadership of the new government. This will lead to higher funding costs, particularly for smaller banks who do not have large deposit base and rely on wholesale funding. Meanwhile, tightening financial regulations, including the expected new regulation on asset management, will affect the shadow banking business. Banks are pressured to move their off-balance sheet lending back on balance sheet (Figure 3). Small businesses are more severely affected in this process, as they have limited access to regular bank loans and rely more on shadow banking. The RRR cut will mainly benefit smaller banks and, with the guidance on lending, will help relieve financing difficulties faced by small businesses.

Here is a link to the full report.

This statement is the first signal since Xi became dictator that the Chinese administration is paying attention to the market and role of investors in reflecting the outlook for the economy. The cut to the reserve requirement demanded of banks is a positive step for the sector since it has been in a corrective phase since the beginning of the year.

The FTSE China A600 Banks Index bounced today from the 14000 level and upside follow through tomorrow will be required to signal confirm a low of at least near-term significance.

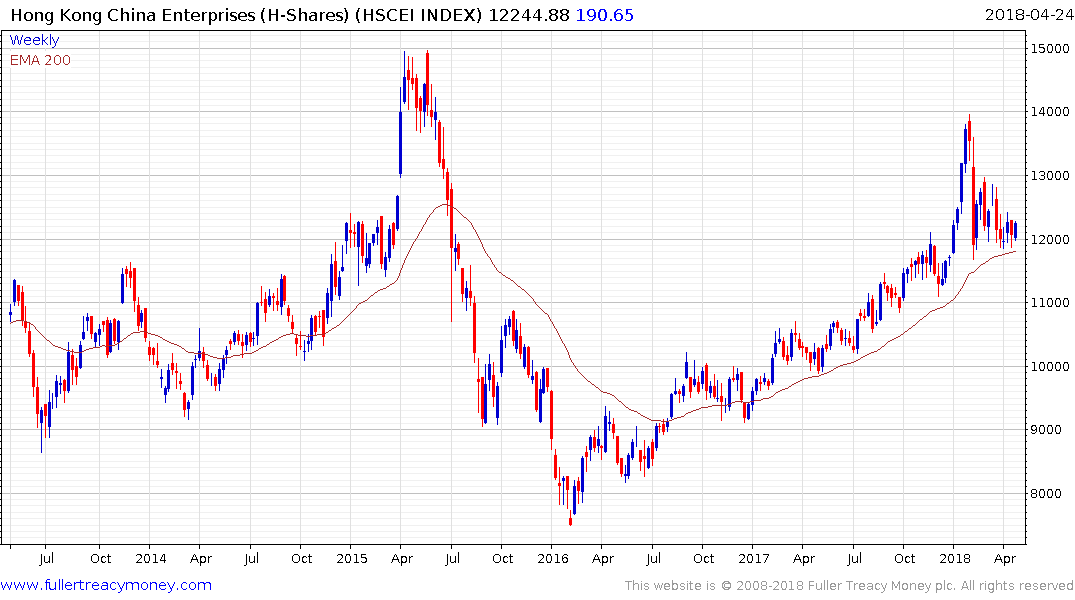

The China Enterprises Index (H-Shares) bounced from the region of the trend mean today but needs to follow through on the upside to break the downward bias evident since early this year to confirm a low of more than short-term significance.

The recent strength of Chinese government bonds is out of step with the weakness on global sovereign bond markets. However, this condition potentially gives us some insight into the demand for a haven, stock market investors have been seeking; during what has been one of the deeper corrective phases evident anywhere.