Pariah status

This has been an extremely difficult period for mining companies, not least as the major iron-ore and diversified mega-cap companies have ramped up supply into a falling market in order recapture market share. From an investor’s perspective, one is left with a dilemma. Many are asking whether it is better to hold on in the hope prices will recover. Others have been disappointed in their attempts to buy only to see prices fall even further. Against a background where technology shares such as Apple, Google, Amazon and Facebook have accounted for the majority of stock market returns this year, underperforming sectors such as commodities have fallen into relative obscurity.

A number of trends have accelerated lower this month and, as anyone who has attended The Chart Seminar knows, this is an ending signal. The question then is whether this is a short-term or potentially medium-term signal. It is simply too early to tell but there is short-term scope for a reversionary rally.

In order to get a more satisfactory answer to this question I performed a search on Bloomberg, focusing on the mining sector, looking for companies with a market cap greater than $100 million and a dividend yield greater than 3%. I wouldn’t normally search for companies with such a low market cap but I believe it is justified at this stage considering how low some shares are trading relative to their peak values. In looking at dividend yields one has of course to consider potential for the dividend not only to be cut, but eliminated. Here is the list of 40 companies, globally, that meet the criteria.

Coal above all others has attained pariah status as environmental concerns, low natural gas prices, accelerating technological innovation and oversupply of steel have coalesced to sap demand. A number of companies have already gone bust but prices have continued to accelerate lower for the survivors. Peabody Energy is now trading at a price to book of 0.21. Some might argue that the equity will be worth nothing if the company goes bust. With a credit rating of B- to CCC its 2018 6% bullet bonds are trading at a yield of 46% so default is priced in. With negative earnings over the last six quarters the dividend was discontinued following the results on Tuesday.

If one were to buy today you could look like a hero or a fool three months from now so is the risk really worth it? Realistically, if one wishes to gamble a casino would probably offer more fun. I clicked through the results of the filter for companies that are paying dividends but exhibit evidence of demand dominance.

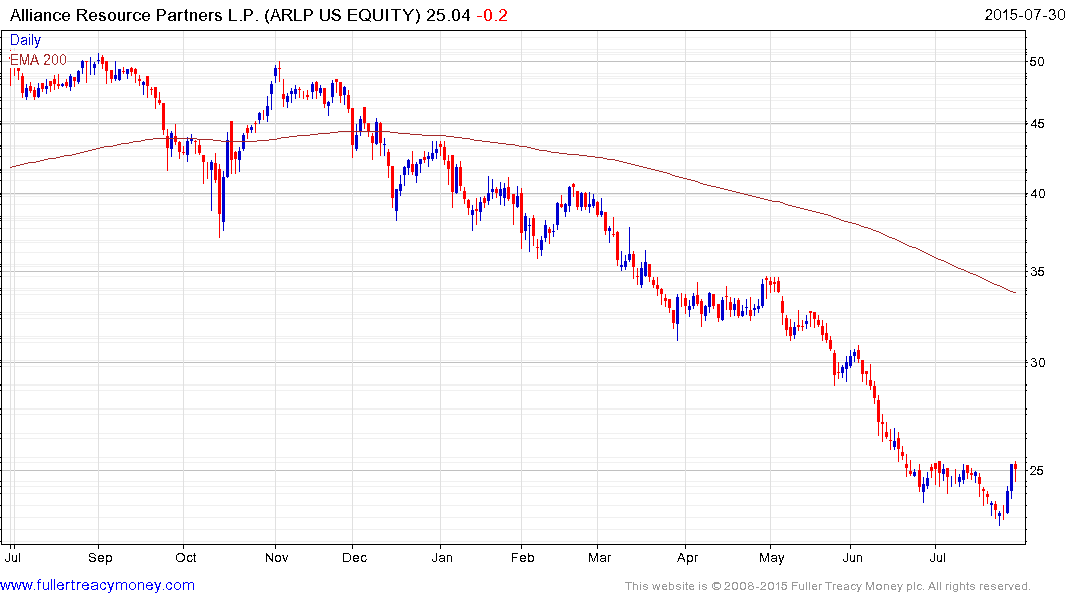

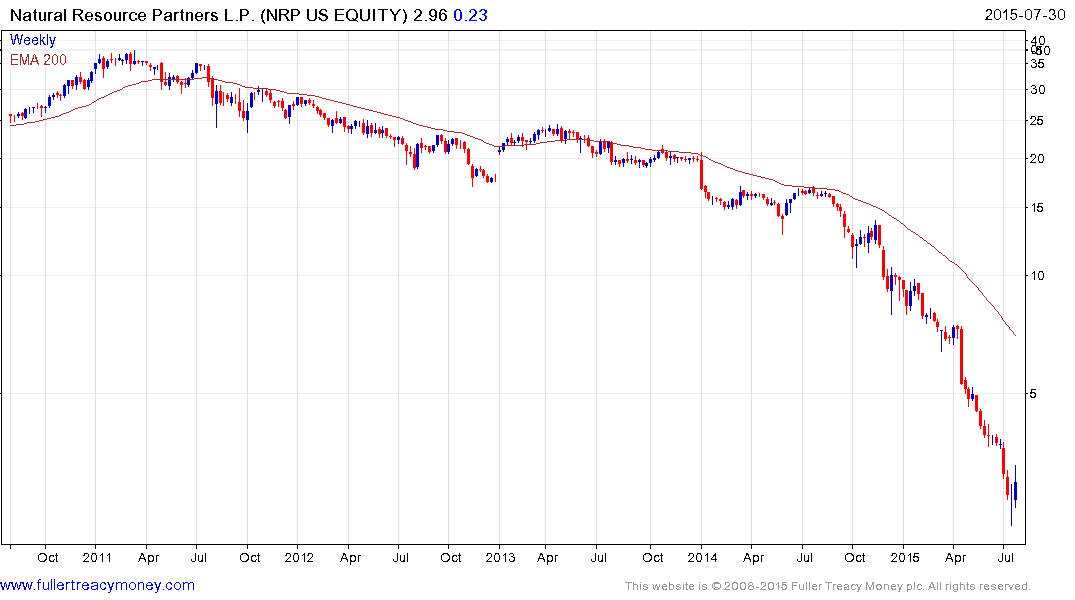

That’s a difficult prospect within the coal sector but both Natural Resources Partners (Est P/E 4.63, DY 11.76%) and Alliance Resource Partners (Est P/E 6.88, DY 10.87% held their dividends this week and have bounced. However it is still too early to say that anything other than short-term support has been found.

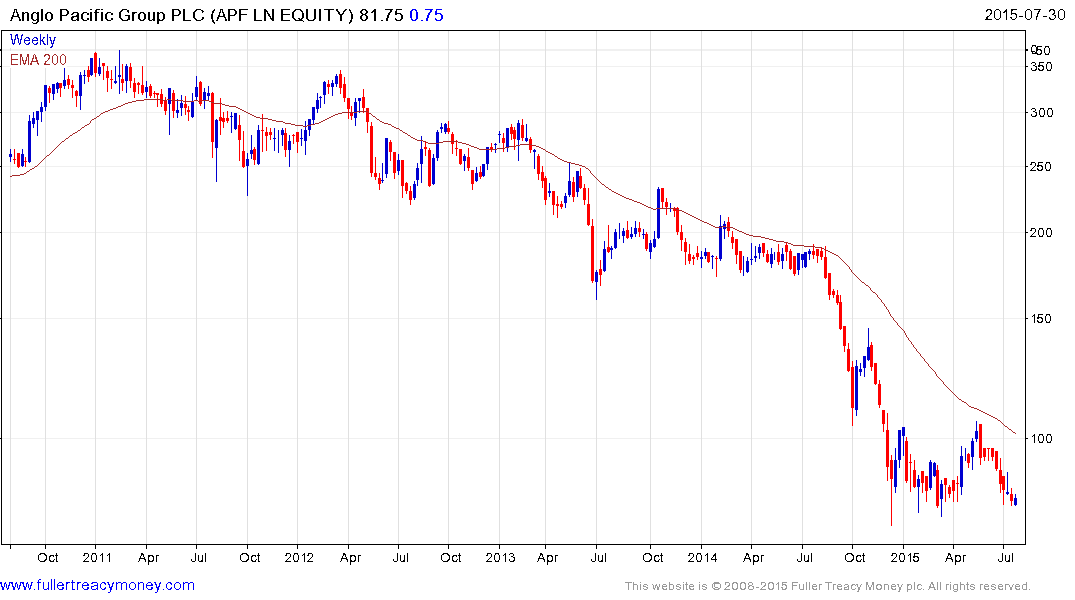

Anglo Pacific Miners is a UK listed royalty streamer for BHP Billiton and Rio Tinto’s Australian coal assets and currently yields 9.79% on an estimated P/E of 31. The share exhibits an incremental progression of higher reaction lows over the last seven months and has paused in the region of 80p over the last month. A sustained move below that level would be required to question the base building hypothesis.

Australian listed Sedgman Ltd is an engineering services company focused on the coal sector with a market cap of A$179.4 million. The share (Est P/E 12.95, DY 9.95 Gross) has been forming as base over the last two years and is currently testing the upper boundary.

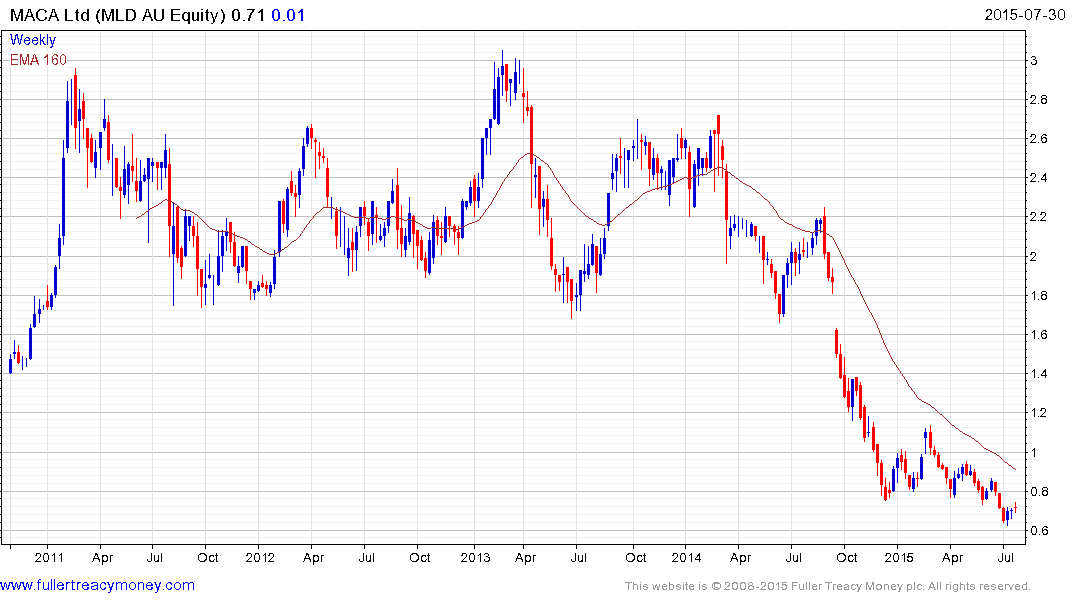

Elsewhere in the mining services sector MACA Ltd (Est P/E 2.74) is also worthy of mention. The company paid special dividends of 80% in 2014 which has distorted the valuations. The share has performed more or less in line with the major miners and broke down to new lows four weeks ago.

Within the gold mining sector, companies that pay attractive dividends have been favoured by investors for much of the last few years and that is likely to continue until such time as a momentum fuelled uptrend in the gold price occurs.

UK listed Highland Gold’s (Est P/E 3.58, DY 10.47%) assets are in far eastern Russia and it has a market cap of £139 million. The share hit a medium-term low in December and has been ranging higher in a process of mean reversion. A sustained move above 50p would begin to suggest a return to demand dominance beyond the short term.

.png)

UK listed Pan African Resources is another interesting chart. The share (Est P/E 7.09 DY 12.74%) has halved in an 8-week decline and is looking deeply oversold and steadied this week, posting an upside key day reversal today. Upside follow through tomorrow would confirm a low of near-term significance.

Canadian listed Centerra Gold (Est P/E 19.36, DY 2.49%) has held a progression of higher reaction lows since late 2013 and rallied this week to confirm support above the C$5 area. A sustained move below that level would be required to begin to question medium-term scope for continued higher to lateral ranging.

Within the Copper sector Canadian listed Nevsun Resources (Est P/E 13.04, DY 4.42%) has held a progression of higher reaction lows for over two years and bounced this week to confirm support in the region of C$4.

In conclusion this is still an incredibly volatile environment and there is precious little evidence just yet that a low of more than short-term significance has been found for the wider sector. However as the above charts demonstrate there are a small number of shares that have so far managed to buck the trend