Our Market and Economic Observations Heading into 2022

Thanks to a subscriber for this report from Bridgewater which may be of interest. Here is a section:

Equity team co-heads Atul Narayan and Erin Miles on other equity markets catching up with the US: Looking ahead, it feels that things are primed for the equity markets that have lagged the US (China, Japan, the UK, Europe, etc.) to catch up. There are several factors at play. First, COVID has been a material relative support to US equities from all channels—favorable sector tilt, less virus economic impact, more support from falling rates (versus, say, Japan, where yields are pegged), and compressing risk premiums, given safe-haven appeal for US equities, especially the FAANMGs. We would expect the COVID impact to gradually fade in the coming year and this to be a relative support for the markets outside the US.

Second, China is showing early signs of moving toward easing after a year when the structural goals (deleveraging, rebalancing, common prosperity, etc.) were prioritized. This again will be a bigger relative support for economies like Japan, Europe, and EMs that are a lot more exposed to China. Finally, if you look back over the last 100 years, it’s almost always been the case that the winners of a given decade end up being laggards in the next one because of the degree of exuberance (and pessimism) that gets priced in following the winning (and losing) stretch. Given how stretched the relative positioning and pricing is today (for logical reasons), we expect the US versus rest of world diff to finally start to revert after a decade-long off-the-charts performance. The main things we are watching closely are the evolution of COVID globally, China’s policy stance, and the retail flows in the US, which were the biggest support for US equities over the past year and a half.

Here is a link to the full report.

Based on valuations alone, there is a strong risk-adjusted argument for favouring ex-US assets. I also find the argument that a recovery for China’s economy would have a more positive effect on the Ex-US basket to be reasonable. However, momentum remains a tailwind for Wall Street which has been supported by the relative strength of the Dollar all year.

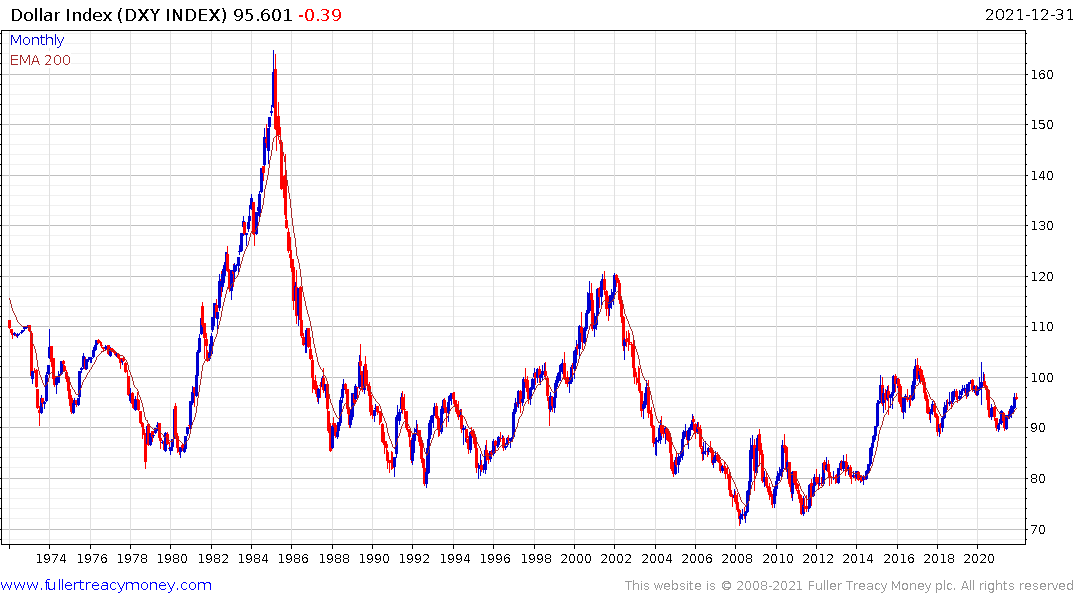

This long-term chart of the MSCI Ex-US Index/MSCI US ratio helps to confirm that the times when ex-US assets do best is when the Dollar Index trends lower.

The inclination to pursue value in the hopes that Europe, Japan, China and everything else can play catch up with Wall Street is tempting and more than a few institutions have made it their primary theme for 2022. I consider this kind of thinking as part of the attraction of value arguments. However, for investor interest to surge, they will need a push out of what has been working for the last 13 years.

The catalyst for change would the Dollar Index breaking down from the six-year range and the FANGMANT groups relative performance to roll over. Until that happens, the ex-US basket can trend higher but is unlikely to outperform in a big way.