Only Greece Can End Its 'Groundhog Day' Misery

This article by Mark Gilbert for Bloomberg may be of interest to subscribers. Here is a section:

On Thursday, chief government spokesman Gabriel Sakellaridis said a May 31 deal was on the cards. But that same day, with a June 5 payment of 300 million euros to the International Monetary Fund looming, Managing Director Christine Lagarde warned that "we’re working very hard, but it takes two to tango. Everybody has to be realistic and be focused on not playing a game." She doesn't sound at all convinced that Greece is facing up to the fact that, without at least some additional aid from its lenders, it won't have the 1.6 billion euros it needs to pay all of its IMF bills next month.

More than four months after Tsipras took power, Greece is deeper in the hole than ever. It can't even pay for medicines; it owes international drugmakers more than 1.1 billion euros and hasn't paid some members of the European Federation of Pharmaceutical Industries and Associations since December, according to a Reuters report citing Richard Bergstrom, the group’s general director.

The Greek government's coffers were down to less than 800 million euros at the end of March, with a run rate that saw 70 percent of its cash spent in the first three months of the year.

One of the reasons Ireland was able to impose a stiff haircut on public sector workers while at the same time raising taxes and cutting services is because there was an understanding the country had been living beyond its means. By spreading the pain equally across various segments of society the administration was able to ensure disgruntled acceptance of the need for reform.

Greece’s entitlement culture has been more pervasive. The fact it falsified economic data to gain access to the Euro was an open joke back in 2003 but was an example of the administrative culture that viewed Europe as a donor rather than partner.

As an aside, this episode offers an excellent example of how crowds are willing to tolerate contradiction for prolonged periods but it is the contradiction that eventually proves the undoing of the mania.

Ahead of Euro entry Greece devalued the Drachma on successive occasions rather than embrace reform. The Euro’s strength from 2003 onwards was the first time the economy had been forced to adapt to a strong currency in decades. Dealing with its creditors without recourse to devaluation represents a major cultural shift for Greece. Electing Mr Tsipras late last year was a response to the failure of the last administration to explain how much trouble the economy is in. He has certainly had an education over the last six months.

The EU is a collegial group and they have no wish to expel Greece. However they need to see reform and an acceptance that profligacy will no longer be tolerated. Anything else would be a further threat to the group’s credibility. It is then really a decision for Greece on whether they are willing to do what is necessary to stay. As the deadline approaches for the next IMF payments the market is pricing in another temporary fix and this has to be the base case. Nevertheless, the potential for a disruptive event while unlikely cannot be ruled out.

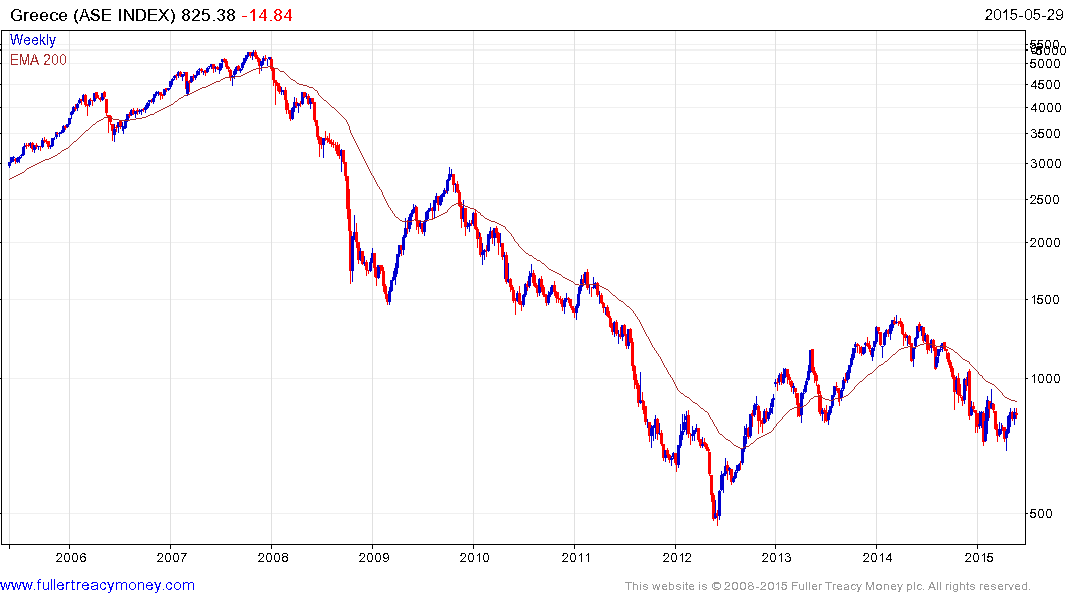

The Greek stock market fell more than 90% to its 2012 low and continues to hold above the psychological 500 level. It is now testing the region of the 200-day MA but a sustained move above 850 would be required to signal a return to demand dominance. At a time like this it is important to remember we buy stocks not companies. Banks still occupy considerable weightings in the Index and of course it is denominated in Euros. The next week will see whether investors are willing to give it the benefit of the doubt at least until we come back to discuss the debt issue in another few months.

Meanwhile major European indices such as the German DAX remain in processes of consolidation following impressive advances earlier in the year.