Oil Climbs as Global Refining Crunch Drives Record Fuel Cost

This article from Bloomberg may be of interest to subscribers. Here is a section:

Oil climbed as a global squeeze on refined products continued to pull fuel prices higher with Russian diesel exports falling sharply.

West Texas Intermediate traded near $110 wrapping up another week of tumultuous trading where lowered liquidity exacerbated price moves. Diesel exports from Russia dropped in April from their prewar level as oil buyers seek to punish one of the world’s biggest suppliers. Investors have also been keeping a close eye on China as authorities in Beijing denied rumors that the city will go into lockdown even as new Covid-19 cases climbed.Fuels are currently the bullish driver for crude, especially as Russian diesel exports drop, said Dennis Kissler, Senior Vice President of Trading, BOK Financial. “The path of least resistance still looks higher for all petroleum products as demand continues to outstrip supplies.”

Diesel and jet fuel prices have been making headlines this year because they are at record levels. The war in Ukraine and Europe’s reliance on Russia for 70% of its diesel have been blamed for this development. However, there is an additional consideration I have not seen mentioned elsewhere.

The IMO 2020 shipping emissions regulation pushed 3.2 million barrels of oil equivalent demand out of bunker fuel and up into the middle distillates. That’s the point in the barrel where both diesel and jet fuel originate. This article from Winston.com may be of interest.

To date, the CI reduction requirement is “expected to achieve a reduction fleet-wide in compliant ships of about 11% from 2019 levels by 2026.” The IMO stated that this is aligned with its 2018 initial GHG strategy to target a sector-wide carbon intensity reduction of 40% between 2008 and 2030, on its way to a 50% GHG emissions cut by 2050.

Additionally, the IMO adopted the EEXI, a goal-based technical measure of existing vessels similar to the Energy Efficiency Design Index (EEDI).[4] Because the shipping industry relies on exceptionally high-cost, long-life capital assets, change is necessarily implemented on a phased-in basis. The amendments are expected to enter into force in November 2022. Shipowners must also ensure their ships are surveyed annually by classification societies using the EEXI. Shipowners and operators have until January 1, 2023 to investigate the options to reduce fuel consumption by their ships’ engines. The first annual EEXI and CII reports will be due that year. The first annual reporting on carbon intensity will be completed in 2023, and the first ratings will be in 2024.

The additional new regulations set to move into place this year will result in ships slow steaming to avoid having to install expensive scrubbers. That will stretch journey times by about 9% which means more ship demand to do the same work and more time to do it.

This is positive for oil prices since it creates demand for valuable products that are only available through the refining process.

This is positive for oil prices since it creates demand for valuable products that are only available through the refining process.

Brent crude rebounded impressively this week to test the most recent of the lower rally highs. These kinds of wedging patterns are usually resolved with large dynamic moves. At present, the most likely direction for such a move is higher.

The Baltic Dry Index continues to extend its rebound and remains on a recovery trajectory.

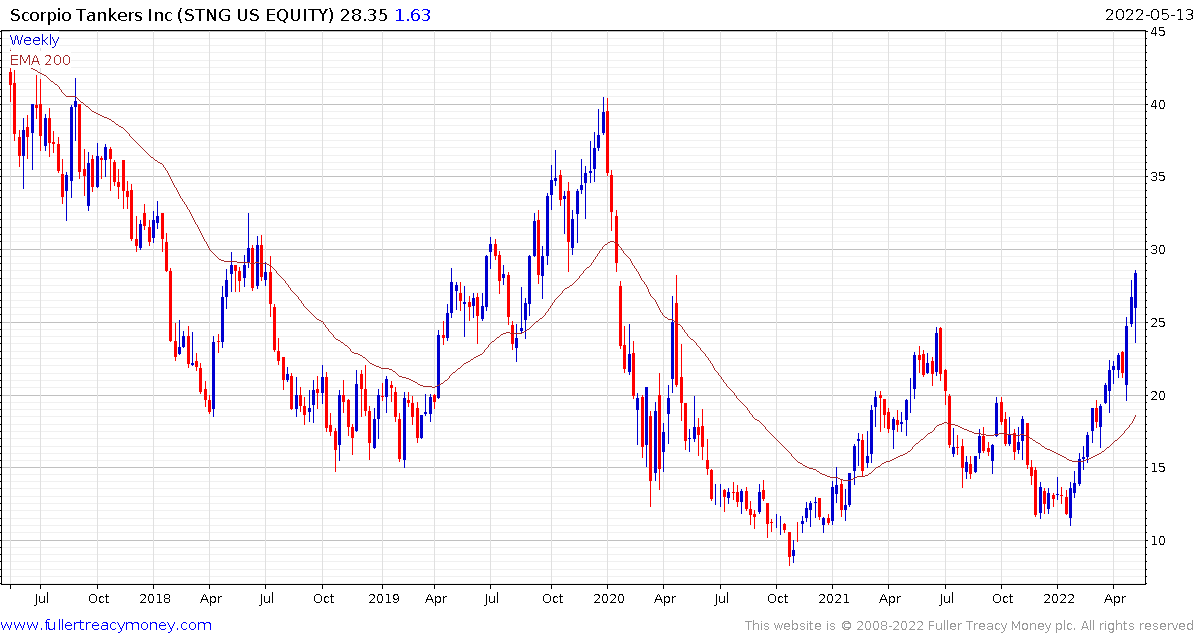

Scorpio Tankers and Ardmore Shipping both rebounded impressively from their reaction lows this week.