Not With A Bang But A Whimper (and other stuff)

Thanks to a subscriber for this report by Ben Inker and Jeremy Grantham for GMO which may be of interest. Here is a section:

At GMO we have put particular weight for identifying investment bubbles on the statistical measure of a 2-sigma upside move above the long-term trend line, a measure of deviation that uses only long-term prices and volatility around the trend. (A 2-sigma deviation occurs every 44 years in a normally distributed world and every 35 years in our actual fat-tailed stock market world.) Today’s (November 7) price is only 8% away from the 2-sigma level that we calculate for the S&P 500 of 2300.

13. Upside moves of 2-sigma have historically done an excellent job of differentiating between mere bull markets and the real McCoy investment bubbles that are likely to decline a lot – all the way back to trend – often around 50% in equities. And to do so in a hurry, in one to three years.

14. So we have an apparent paradox. None of the usual economic or psychological conditions for an investment bubble are being met, yet the current price is almost on the statistical boundary of a bubble. Can this be reconciled? I believe so.

15. There is a new pressure that has been brought to bear on all asset prices over the last 35 years and especially the last 20 that has observably driven the general discount rate for assets down by 2 to 2.5 percentage points. Tables 1 and 2 compare the approximate yields today of major asset classes with the average returns they had from 1945 to 1995. You can see that available returns to investors are way down. (Let me add here that many of these numbers are provisional. We will try to steadily improve them over the next several months. Any helpful inputs are welcome.) But I do believe that readers will agree with the general proposition that potential investment returns have been lowered on a wide investment front over the last 20 years and that stocks are generally in line with all other assets.

Here is a link to the full report.

I agree that the topic of bubbles is central of what our job as analysts is. If we can succeed in identifying the latter stages of a bubble, we can avoid the worst effects of the subsequent bear market, so that we are in the privileged position of having ample liquid capital with which to participate when a new bull market evolves. The big question now is to what extent the major stock market indices exhibit bubble characteristics.

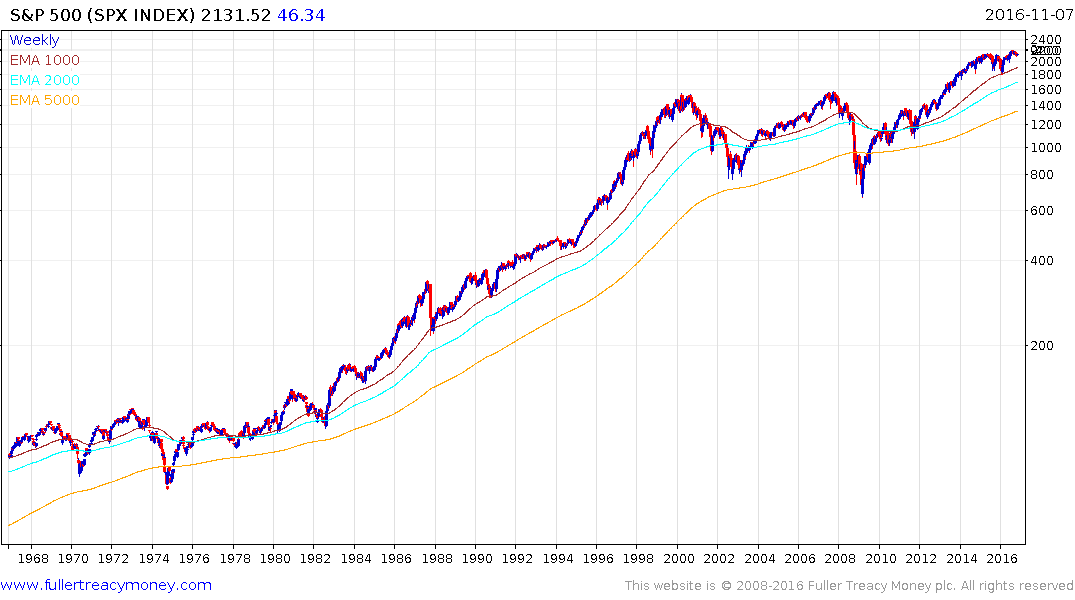

The S&P500 broke out of a long-term range in 2013 and spent 18-months ranging before breaking out to new highs again in July, but it has not improved on that performance subsequently. The above charts show the 1000, 2000 and 5000 day moving averages which represent approximately 5, 10 and 25 year averages respectively.

.png)

During periods of time when the Index has been through a generational long mean reversion the three MAs converge. This happened in 1945, 1976 and 2012.

If we ask ourselves a simple question, is it possible for prices to range following a breakout before resuming the overall uptrend? The simple answer is yes and so far that is what the S&P500 is doing. Could it result in a failed upside break if the breakout is not sustained? The simple answer is yes and we know what that would look like.

Fundamental valuations are not absolute because the dividend discount model is itself influenced by interest rates. Therefore the discount rate has an outsized influence on what people are willing to pay for any investment vehicle.

There is a logical fallacy in the argument propounded in the above report. You cannot on one hand highlight that the stock market has bubble characteristics and on the other predict returns will be disappointing because animal spirits are absent and because the discount rate is permanently lower. If market history teaches us anything it is that nothing lasts forever. It is true that the discount rate has been low for a long time, and for longer than most people anticipated, but it is a logical fallacy to say it will stay that way indefinitely.

An enormous quantity of debt has been issued to avoid a recession and to take advantage of lower rates and the expectation that the discount rate will never rise. What if refinancing costs are higher in future? What if the historic default rate is higher than we have seen in 35 years? These are the really big questions and will have repercussions for every asset class.

.png)

Inflation is the age old solution to debt problems. Nominal stock prices tend to rise with inflation and gold cannot simply be lent into existence, but bonds bought at high prices will still only redeem at par. Of course none of these issues unfold all at once however I think that the complacency and institutional groupthink associated with the view that the discount rate will never rise is perhaps the clearest signal of all that a bubble is clearly in evidence in the fixed income markets.