Not Business as Usual

Thanks to a subscriber for this heavyweight 329-page report from Deutsche Bank which may be of interest. Here is a section:

Not business as usual for the oilfield services industry

This is an industry that is still in transition, and these are companies that still need to navigate this transition. The commercial development of tight oil reserves in the US was disruptive and it derailed the normalization of the cycle. The business models that worked last cycle will not necessarily work again this cycle. We believe in the long term, the oilfield service franchises that will be the winners will be those that evolve with innovative business models, and those that acquire or invest in niche technology leaders.

Pressure pumping demand poised to recover to 2014 highs

The biggest common denominator among our top picks is exposure to pressure pumping. As US producers tailor their drilling programs to focus increasingly on their core acreage and best wells, there will be a disproportionate mix of leading edge, longer lateral wells with tighter stage spacing and higher sand loadings. This will drive the average completion intensity per well even higher, which should restore the demand for horsepower to the 2014 highs despite a lower rig count.

Here is a link to the full report.

Oil service companies have been among the primary targets for cost cutting by major oil producers. As wave after of wave of rationalization gripped the sector during the oil price collapse the major oil producers cancelled green field sites, abandoned deep-water drilling and committed to a lower for longer price forecast which dramatically altered their spending plans. The result was that the oil service sector is now a fraction of the size it attained at the oil peaks in 2008. That is before one considers the current optimism for electric vehicles, renewable energy and domestic batteries.

However, there is an additional consideration. Much of the new onshore supply from the Permian Basin and other jurisdictions is technically tricky to extract. Maximising production from tight wells requires experience technology and data mining which the established oil service companies can provide albeit now at a reduced cost.

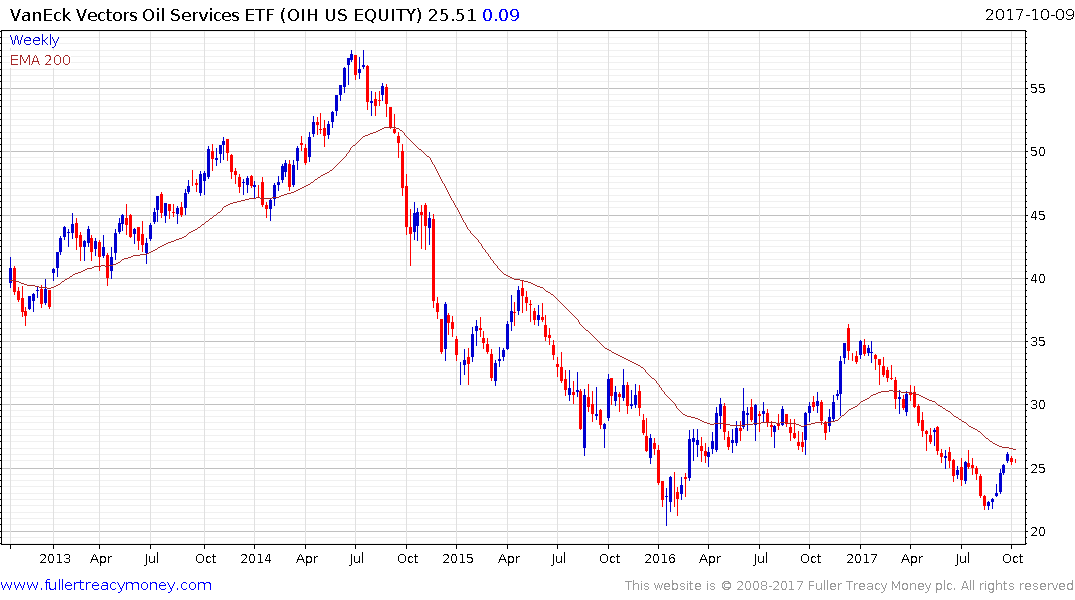

The VanEck Vectors Oil Services ETF rallied from the August low to break this year’s progression of lower rally highs and it is now testing the region of the trend mean. It will need to sustain a move above $27 to confirm a return to demand dominance beyond short-term steadying.

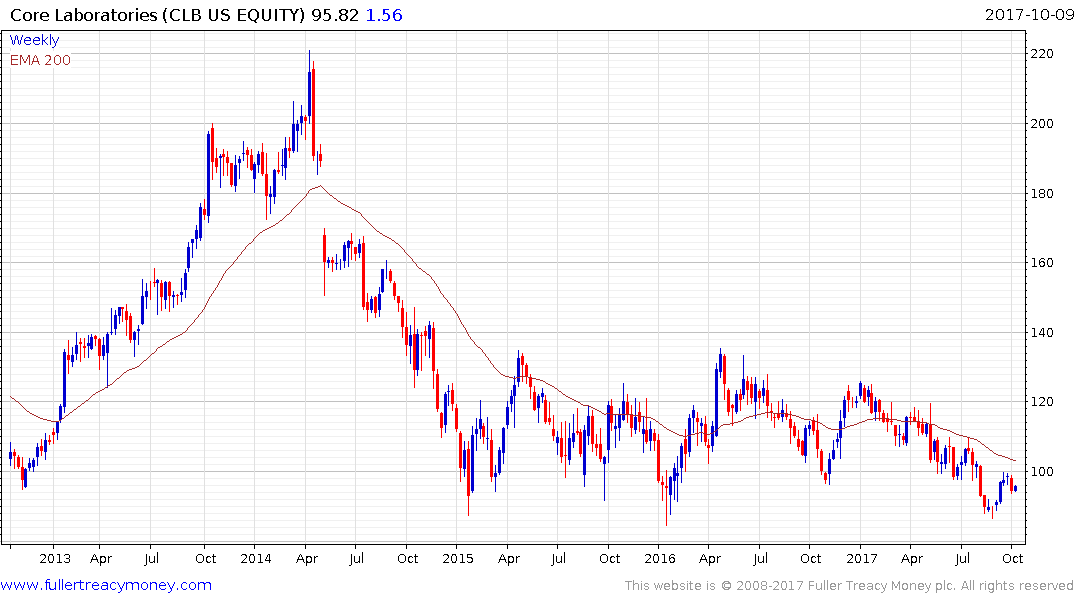

Core Laboratories has been confined to a range since early 2015 which stands in sharp contrast to the downtrends that have prevailed throughout the sector over that time. It is currently bouncing from the lower side and a sustained move below $85 would be required to question medium-term scope for additional upside.

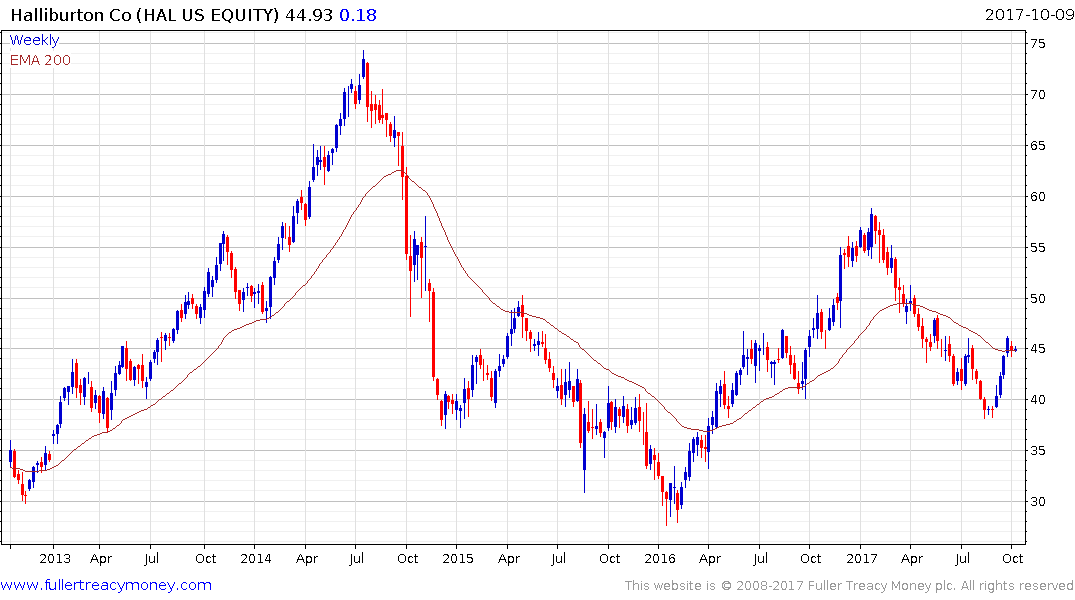

Halliburton fell less that arch rival Schlumberger and has subsequently bounced to break this year’s progression of lower rally highs. It will need to hold the $40 area if potential for additional upside is to be given the benefit of the doubt. The 10-year chart demonstrates the cyclical nature of the business with exaggerated peak to trough swings and a fresh upswing may now be underway.