No Bazooka, Many Pistols - Stimulus Lifts 2% GDP

This is compelling headline from Chan Shu, formerly a senior economist at the Bank of International Settlements which helps to emphasise the new Chinese approach to stimulus. Here is a section:

What’s missing? The government hasn’t so far set out a clear plan to defuse mounting debt risks. Also, a lack of direct support targeting vulnerable households and businesses may make it harder to restore confidence.

A statement from the July meeting of the Communist Party’s Politburo indicated the top leadership recognized the importance of “formulating and implementing plans to resolve local debt.” But the steps taken so far — such as a debt swap of 1 trillion yuan for local government financing vehicles — pale in comparison to the size of the problem.

A reduction in tax burdens for households – higher deductions for expenditure on childcare and education — is a positive move but probably too modest to have a material impact on growth. Broader and bolder support measures are required to revive confidence.

Some stimulus is better than none, but the broad question is how dependent is the Chinese economy on credit and leverage? It is well understood the incremental benefit China accrued from infrastructure peaked more than a decade ago.

To avoid the middle-income trap, they had to greatly enhance productivity. There is no doubt some progress was made on that front, but total debt in the economy has tripled from $17 trillion to $51 trillion. They doubled down on infrastructure and property despite the falling rate of return.

The credit impulse was highly cyclical over the last decade and granted investors some confidence that China’s willingness to provide successive rounds of assistance was a permanent condition. That is no longer true. The measure has been inert for almost two years. It’s a clear confirmation of the piecemeal approaching stimulus.

The credit impulse was highly cyclical over the last decade and granted investors some confidence that China’s willingness to provide successive rounds of assistance was a permanent condition. That is no longer true. The measure has been inert for almost two years. It’s a clear confirmation of the piecemeal approaching stimulus.

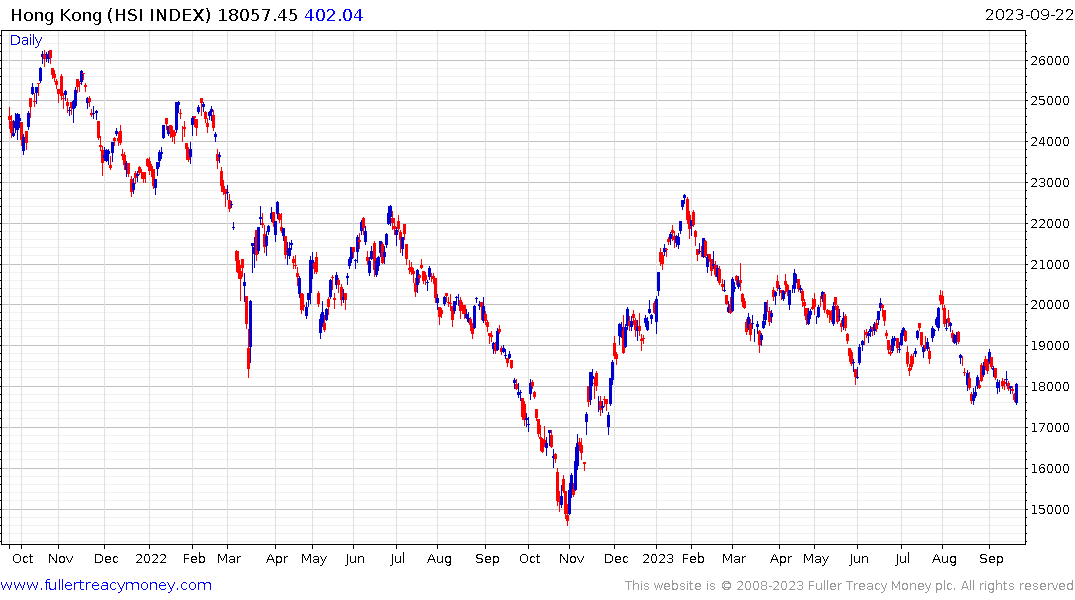

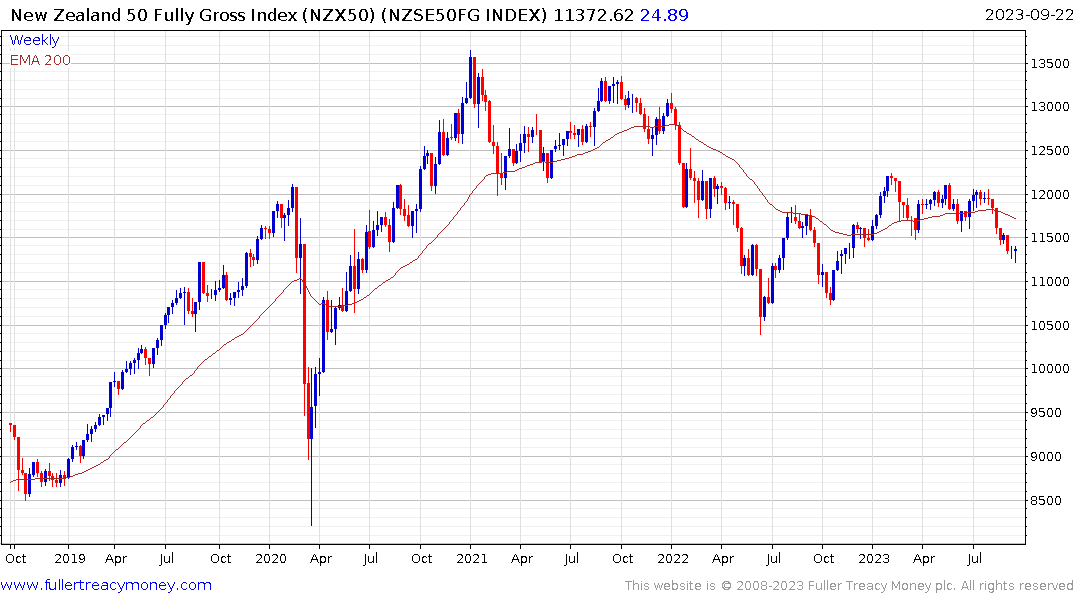

Nevertheless, the Hang Seng Index posted an upside key day reversal today and both Australia’s S&P/ASX 200 and the New Zealand Fully Gross 50 both rebounded from their respective intraday lows. That suggests lows of at least near-term significance have been found. The proximate reason is the USA and China are likely to sustain semi-cordial relations as both sides race to insure themselves against decoupling.

Let’s think about some of China’s successes. They have rapidly automated the manufacturing sector and have world class infrastructure. Some of the infrastructure spend went into battery factories, solar manufacturing capacity and wind turbines. China is now highly competitive in producing electric vehicles.

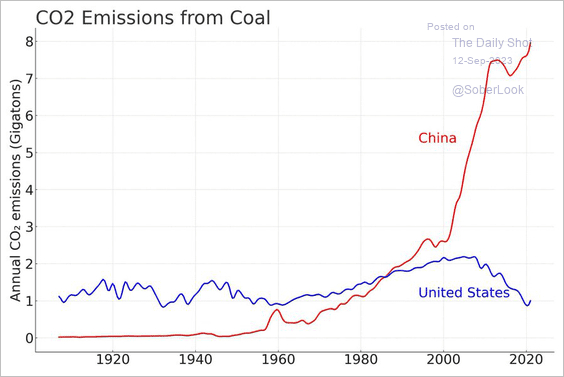

The issue that is likely to move centre stage over the coming months and years is China produces everything the green agenda seeks to curtail carbon emissions while simultaneously burning eight times more coal than the USA.

China’s carbon emissions are more than double the USA’s and more than triple the EU’s.

As the EU steps up protectionist efforts to preserve its automotive industry surely some enterprising politician is going to ask the simply question “why are we bending over backwards to buy everything from China to curtail emissions when their emissions are triple ours?”

Back to top