Musings from the Oil Patch June 14th 2016

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section on electric car demand:

As electricity is gaining importance in the nation’s energy mix, the role of electric vehicles is being promoted by environmentalists who see them as a way to end the use of petroleum. These same groups are pushing electric cars as the perfect vehicle for autonomous vehicles that are envisioned as a way to reduce the number of cars needed in future economies, with concomitant less use of petroleum fuels. As they build their case, we have been overwhelmed by articles praising the increase in the number of electric vehicles in today’s vehicle stock and how they will (need to) grow in order to fulfil the UN climate change agreement.

A recent electric car article offered the chart in Exhibit 3 (next page) showing how the number of these vehicles in the world have grown. The chart reflects the cumulative total between 2010 and 2015, showing dramatic growth. Because it is cumulative, the growth is deceiving. More important is the penetration rate of electric vehicles into the world vehicle fleet.

As the chart shows, the global industry has over 1.2 million electric vehicles on the world’s roads – but that is out of an estimated one billion vehicles. The point is that for all the dramatic growth (which presentation charts can make look impressive) in the number of electric vehicles on the roads, they barely register as a component of the global vehicle fleet total.

An interesting area for research into the success of electric cars is to see how many of them are owned by governments – federal, state and municipal – along with ones purchased by utility companies in an effort to demonstrate their environmental sensitivity. Our guess is that in the U.S. these buyers would account for the largest portion of the electric vehicles on the road. That would suggest that real consumers – not those motivated by making political statements – are not embracing electric vehicles, despite the concerted efforts of governments to promote them through mandates and financial

If we look at the dark green portion of each bar that represents the number of electric cars in the United States, the country has gone from a minimal number in 2010 to 400,000 vehicles in 2015. Yes, that is dramatic growth, but the 2015 number is less than half the number President Barack Obama called for to be on America’s roads. More telling is the difference between the height of the dark green portion of the bar in 2014 and 2015, showing that the industry added slightly over 100,000 vehicles. That number comes in a year when the U.S. auto industry produced and sold over 17 million vehicles. The penetration of electric cars into the American vehicle stock is paltry as 400,000 units barely registers in a fleet of about 300 million vehicles on the road.

Here is a link to the full report.

Electric vehicles (EVs) are on an exponential growth curve. However we are still in the very early stages of that growth where big numbers do not equate to large numbers of vehicles on the road. For example Tesla’s orders for more than 400,000 Model 3s is equivalent to the entire US fleet of EVs on the road today. With that kind of growth rate it’s important to keeps one’s feet grounded in reality.

The lithium required to feed the growth in the electric car market is pressuring the ability of companies to supply the market so prices are rising. However that does not mean that EVs are going to replace cars next year. Range anxiety has not yet been overcome and SUVs and pick-up trucks are still by far the best sellers in the US market. That won’t always be the case but it could be a decade before the EV market has multiplied enough to put a dent in demand for the combustion engine.

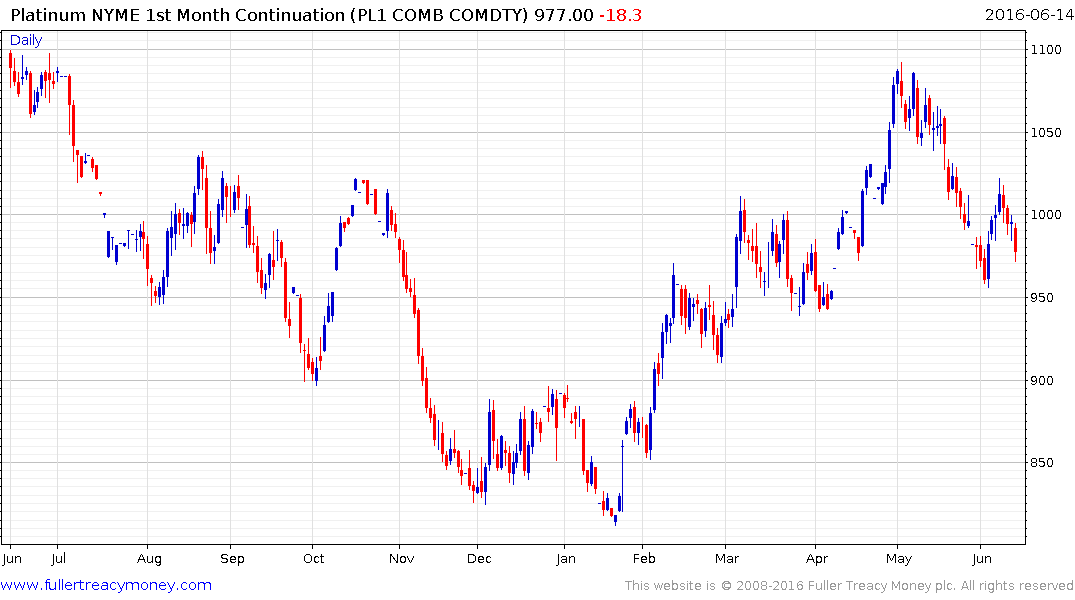

The relative weakness of platinum is a reflection of the lack of a demand growth story for catalytic converters but I wonder if the market is a bit premature in reaching that conclusion. Gold is almost back testing its relative peak against platinum and while there is a good long-term story about why platinum might stay cheaper the question is whether that is relevant today.

Platinum posted an upside key reversal early this month to check the pullback from the May peak near $1300. It has now fallen back to test that low and a similar upward dynamic will be required to signal a return to demand dominance.