Musings from the Oil Patch December 15th 2015

Thanks to a subscriber for this report by Allen Brooks for PPHB which may be of interest. Here is a section:

What seems evident from the chart is that when the labor force participation rate fell below 66%, the rate of increase in oil consumption slowed and eventually declined. That decline was partially triggered by the fall in labor force participation, but there was also a small event known as the Great Recession, aka the Financial Crisis. While the oil consumption decline bottomed out and has actually shown a small increase since, driven largely by an increase in gasoline use, the participation rate has sunk lower. With the Labor Department’s projection calling for a further meaningful decline in the labor force participation rate over the next ten years, without low oil and gasoline prices, it is hard to see how energy consumption grows in any meaningful amount. That is the bad news from the Labor Department’s supposedly upbeat job creation forecast. The low U.S. economic growth outlook this forecast calls for unfortunately is being repeated in another major oil consuming region – Europe - where the combination of weak economic activity is combining with unfavorable demographic trends to drag down that region’s future economic growth rate. This is merely one of numerous headwinds for the global oil and gas business, and a factor that will make the industry’s recovery that much more challenging and likely requiring more time.

Here is a link to the full report.

Demand growth is not nearly as volatile as supply when assessing the prospects for global energy use. However there is no denying that the evolution of the services sector is less energy intensive while urbanisation and rapidly rising standards of living are more energy intensive. Therefore on a global basis the demand growth argument depends more heavily on emerging market growth than developed markets like the USA or Europe.

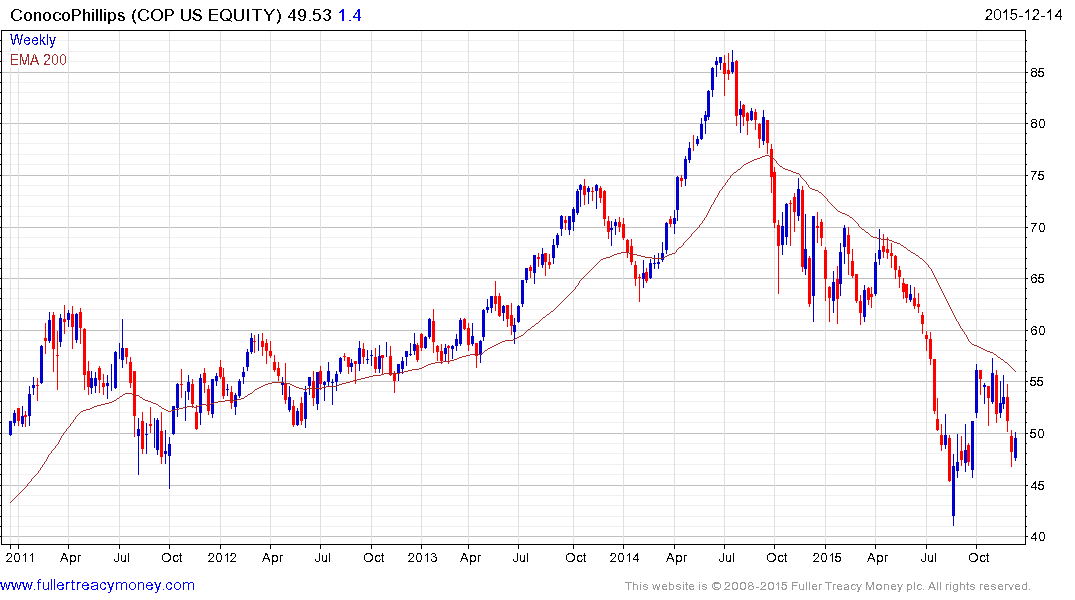

Oil prices improved on yesterday’s performance and major oil companies rallied impressively to confirm at least near-term support above their respective lows. Exxon Mobil (Est P/E 20.24, DY 3.7%) Chevron (Est P/E 26.94, DY 4.63%) and ConocoPhillips (Est P/E N/A DY 5.85%) all share this characteristic.

![]()

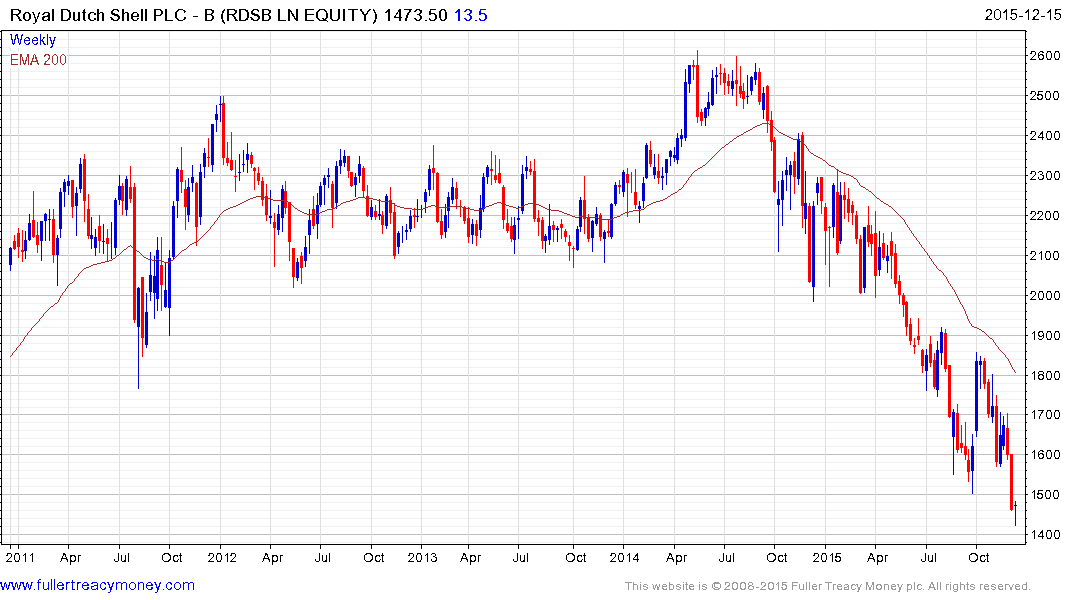

Royal Dutch Shell (Est P/E 12.17, DY 8.41%) has almost halved since 2014 and a short-term oversold condition is evident as it tests the 1400p level. A sustained move below that level would be required to question potential for a reversionary rally.