More favorable 2015: Stronger demand and supply dynamics

Thanks to a subscriber for this report from Deutsche Bank focusing on Chinese property developers. Here is a section:

More favorable supply-side dynamics According to NBS, nationwide new home prices have fallen 4-6% since April, and sales have responded positively to such price cuts. On our analysis, overall residential inventory period (including properties under construction but with presale permits) has already peaked out and fallen to 16.5 months in Sep (down from a high of 21 months early 2014). As developers maintain price cuts and discounts, inventory period should continue to fall. Given significant falls in land sales (-26% YoY) and construction starts (-14% YoY) in 2014 YTD, new supply should fall further in 2H15, by then we see a return of pricing power.

Key concerns: margin pressure, corporate governance events, financing risks

Given more price cuts and slower decline in land prices than property prices, we see more downward margin pressure. And with on-going anti-corruption campaign of central government and recent corporate governance events for some Chinese developers, we see higher risk premiums and deeper valuation discounts to be applied to certain non-state-owned Chinese developers.?Our positive industry views are supported by the current cheap valuations of the China property stocks. Our top picks are those with: 1) favorable landbank vintage (i.e. management has good market expertise in timing market cycles); 2) the ability to obtain cheap financing; 3) good revenue diversification (like a sizeable and growing investment property portfolio); and/or 4) very attractive valuations.

Here is a link to the full report.

China is unwinding a property led investment policy and has been squeezing property prices for more than two years. They know as well as anyone else that to keep squeezing when prices are already falling would be a mistake which is why we now see signs of easing. A greater willingness to open up the domestic capital markets is an additional sign that credit expansion will once more be tolerated.

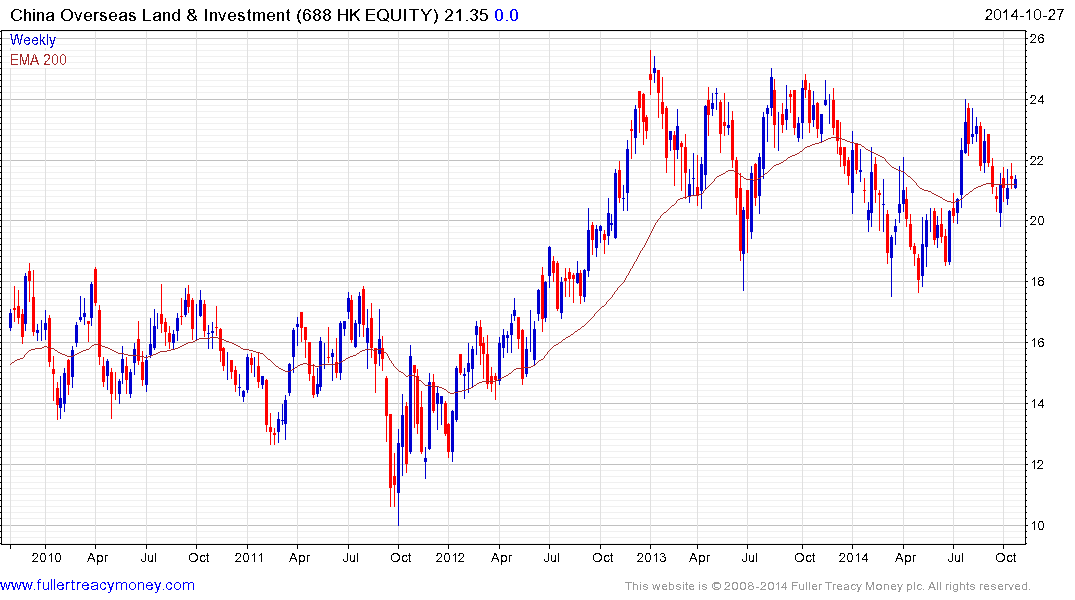

China Overseas Land (Est P/E 7.54, DY 2.3%) has held a progression of higher reaction lows since March and a sustained move below HK$20 would be required to question medium-term scope for continued higher to lateral ranging.

China Resources Land (Est P/E 8.71, DY 2.55%) rallied in July to break a yearlong progression of lower rally highs and has been consolidating in the region of the 200-day MA since.

Kaisa Holdings (Est P/E 3.38, DY 5.4%) has held a progression of higher reaction lows since late 2012 and a sustained move below HK$2.60 would be required to question medium-term scope for additional upside.