Mean Reversion and other Misconceptions about Profit Margins

Thanks to a subscriber for this interesting report from the The Jerome Levy Forecasting Center on the contributing factors behind the relationship between profits, margins and profit sources. Here is a section:

When it comes to conventional wisdom about macroeconomic profit margins, investors beware.

First of all, do not expect margins to “revert to the mean”. A profit margin is not a random variable. Its behavior is complex and sometimes hard to predict, but that does not make it random. Throughout history, when the aggregate profit margin has been unusually far from its historical mean, it would have been unwise to expect it to revert. One would often have ended up waiting for many years, and sometimes for decades.

Second, looking to the future, each step of the way profit margins will depend on profits, which will depend on the profit sources. Global structural financial issues, public policy, business trends, technology, demographics, sociology, and other influences on the profit sources – and not a simple probability distribution – will determine what happens to profits and profit margins.

Third, interpreting profit margins depends a great deal on context. For example, recent years’ wide margins have accompanied by a low ratio of profits-to-equity, which is what ultimately matters to shareholders.

Fourth remember that the influences on aggregate profits margins are different from influences on the margins of individual firms. Competition can certainly compress margins within a firm or industry, but aggregate profit margins are not “competed away” in the business sector as a whole. Rather, changes in the profit sources are what increase or decrease aggregate profit margins.

Here is a link to the full report.

There has been considerable debate about the elevated level of US Corporate Profits over the last few years with some analysts predicting what would be a cataclysmic mean reversion while others have been more sanguine. This is the first report I’ve seen attempting to look through the figures to identify the factors behind corporate profits that are contributing to this condition and I commend it to subscribers.

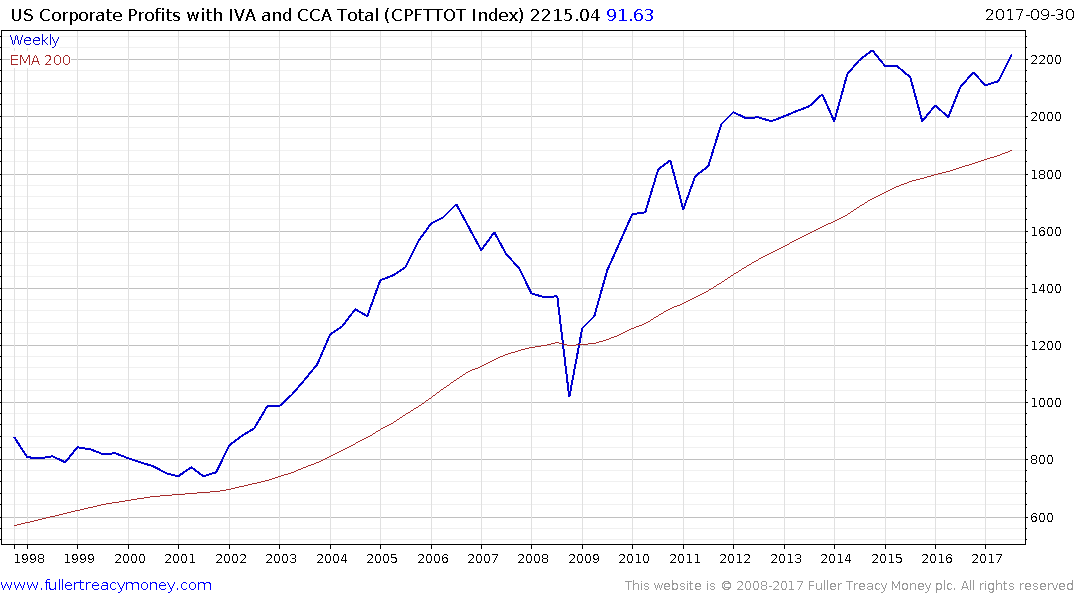

US Corporate Profits are reported with at least a quarter lag and will next be updated on December 20th. The Index has been largely rangebound for the five years which has meant the advance in stocks has been supported by valuation expansion. It is reasonable to conclude that the recovery in profitability from the 2009 lows is attributable to massive monetary and fiscal stimulus and that the hiatus over the last few years has also been influenced by the end of quantitative easing.

The measure is firming now with the announcement of another fiscal stimulus amid what is still a low interest rates environment despite the Fed’s projection today that it will hike three times in 2018.

Stock markets remain steady while the Dollar pulled back sharply today, particularly against the Yen, not least because fiscal stimulus is not especially bullish for the currency.