Martin Spring's On Target

Thanks to the author for this edition of his wide-ranging report which may be of interest to subscribers. Here is a section on the outlook for stock markets.

There are no signs yet of imminent recession. Morgan Stanley says: “Consumer

confidence remains high and spending on services remains healthy.” There’s no significant weakness yet in “early-cycle” industries such as advertising or casinos.

We can expect the Fed to err on the side of caution in raising interest rates. Future earnings growth of around 10 per cent sounds fine to me. And nearly all commentaries about Trumpian policies are infested with emotion and ignore positive outcomes.

The fundamentals of the world economy remain sound. The US remains the world leader in the new technologies that drive much of the growth. China, we’re told, is “slowing down”… but to an incredible 6.2 per cent a year. India is doing even better. Europe, despite its crazy politics, doesn’t seem to face any credible major threats to its prosperity and abundant welfare systems.

All of which suggests that what the markets have been experiencing is nothing more than a major correction. Sentiment has been shocked by the speed and dimensions of the trend reversal. Those with lots of cash will hold back and not recommit till they see positive news. This suggests the probability that markets will soon stop falling, but they’re not likely to bounce back strongly for a while, and to trade in a range for some months to come.

But what if I’m wrong with my relative optimism? What if the current stock-market weakness is not merely a correction, a pause for consolidation after years of excitement, but an ominous signal of something much worse to come?

The Economist recently ran a speculative report on the subject of The Next Recession. Its big fear is that governments won’t be up to the job of taking swift action to deploy the many policy tools available to underpin economic growth and to drive recovery.

The traditional stimulus policy of easing credit won’t be available because interest rates are already too low, while going to the extreme of negative ones – charging interest on bank deposits or bonds -- is (probably correctly) viewed as too dangerous.

Here is a link to the full report.

Personally, I’m not convinced by the argument that central banks will not be able to ride to the rescue the next time we have a recession because interest rates are already too low. The simple fact is that when you control the money supply, and hold vast swathes of the bond market there is no limit to the number of extraordinary monetary and fiscal levers that can be deployed if the need arises. As we have learned over the last decade, just because it has never been done before does not mean it can’t be.

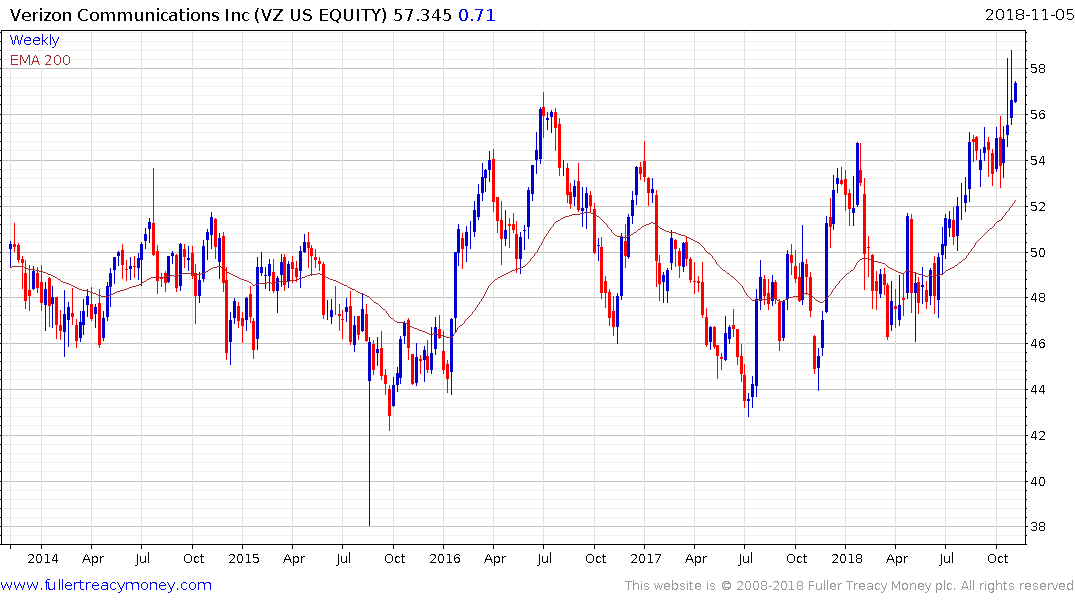

The one clear conclusion we can draw from stock market activity right now is that a clear rotation is underway from previously high-flying technology companies and into strong cash flow reliable dividend paying companies. In other words, risk appetite is clearly favouring defensive shares.

Verizon, a telecoms company with a 4.2% yield, broke out of a five-year range last week.

Meanwhile, the Philadelphia Semiconductors Index has clear Type-2 top formation characteristics.

The market reaction to the result of the Midterm elections this week will give us some insight into whether the S&P500 can push back above the trend mean. If it can then we can conclude this episode is more similar to the medium-term correction in 2015 and 2016. I suspect 2500 is an important psychological Rubicon for the market.