Market and Volatility Commentary

I asked around for this note from Marko Kolanovic for JPMorgan back in June but it finally turned up in my inbox today. Despite the fact the trading advice is dated, the discussion of the animating factors behind low volatility remain valid and I commend it to subscribers. Here is a section:

Low Volatility is not a new normal or fundamentally justified – it is result from macro de-correlation and massive supply of volatility through yield generation products and strategies. Finally, Big Data Strategies are increasingly challenging traditional fundamental investing and will be a catalyst for changes in the years to come.

And

What is really driving the low volatility? As we discussed recently low correlations (driven by quant flows, sector and thematic trading) are temporarily reducing volatility by 2-4 points, and a massive supply of volatility pressures implied and extension realized volatility by another 2-4 points. We estimated that supply from yield seeking risk premia strategies grew by $1Bn vega (30% of the S&P500 options market). In addition to these, large inflows in passive funds put further pressure on volatility. Keep in mind that passive investors almost never sell. Quant investors don’t take large directional bets and don’t overreact either (at least not for the same reasons humans do). Regardless of those, we think current low levels of volatility is not a new normal and will not last very long given the amount of leverage, rising rates, and the approaching reduction of central bank balance sheets.

Here is a link to the full note.

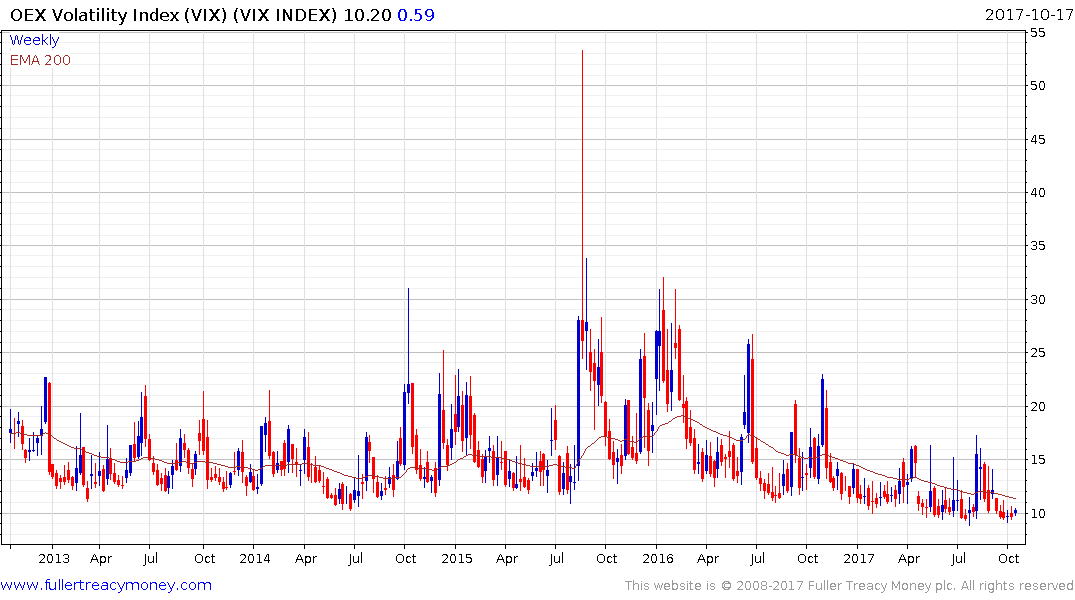

Volatility has not increased to any meaningful extent since April but there have been occasional pops on the upside which have not been sustained. These occurred in May, June and August so it has been two months since the last one.

The S&P500 has rallied by about the same amount as it has done on previous breakouts, in the context of what has been a consistent step sequence uptrend this year. Potential for another pause and consolidation, that unwinds the short-term overbought condition, have increased.

The important point to consider is that the VIX is calculated as an average of options prices available on the Index and low volatility tends to result in a bunching of prices around the current level. Therefore, even a small move in the underlying Index can have an outsized move in volatility. Heavily leveraged short volatility trades coming under pressure tends to have an outsized effect on short VIX ETFs like SVXY or XIV.

From a broader perspective, the fact less than 10% of trades are now made by those following a fundamental value oriented strategy versus the rising influence of passive and quant funds represents an increasingly obvious contradiction in the market because liquidity and momentum have historically been parasitic on the price discovery of fundamental analysis. If that is now declining to the point of obscurity it increases the potential for misallocations of capital.

If we are now in the 2nd psychological perception stage of a bull market, characterised as acceptance, the evolution of artificial intelligence backed trading systems has the capacity to push the crowd into the euphoria stage. Rising interest rates and the shrinking of central bank balances on aggregate would represent challenges to that hypothesis so are particularly worth monitoring.