Long Run Crop Price Outlook: $6 Corn and $13 Soybeans

I met Michael Devlin from Cere Partners at last week’s Contrary Opinion Forum and had a long chat about the merits of farmland in a diversified portfolio. Here was kind enough to send me their outlook for corn and soybeans which they farm in Indiana. Here is a section:

Brazil has been expanding its soybean acreage for 20 years, but $16.00 soybeans made the economics attractive on even marginal ground, which may not yet be fully conditioned to neutralize the naturally high acidity. Consequently, we witnessed the second biggest expansion of Brazilian soybean acreage ever. (See Exhibit 3) Furthermore, $7.50 corn made not only 1st-crop corn attractive in Southern Brazil, but also 2nd-crop or safrinha corn. In some parts of the world, including major parts of Brazil, farmers are often able to get 2 crops by planting a soybean variety with a shorter growing season, and then immediately planting the second crop (often corn, cotton, or sorghum). "is acreage is able to rotate annually to whichever crop offers the best economics. But second-crop corn is risky. Farmers are gambling that the rainy season will continue until the corn is mature. However, at $7.50 or even $6.00 the economics have been compelling and in Brazil there was a major expansion of second crop corn in 2012 and 2013. For the first time ever, second crop corn (safrinha means “little crop” in Portuguese) was bigger than first crop corn, comprising 56% of the total production.

Where $7.50 corn (and $16.50 soybeans) signals an expansion of acreage, Ceres believes $4.50 corn (more precisely $10 soybeans) signals a reduction of acreage. Mato Grosso State in West Central Brazil grows approximately 10% of the global soybean crop. But Mato Grosso soybeans must be hauled more than 1,000 miles by truck over poor roads to get to market. Net of transportation costs, the price farmers receive for soybeans is significantly below the price quoted in Chicago.

Currently the “basis” on bids for 2014 soybeans is reportedly ~$3.00 under Chicago. So $10 soybeans in Chicago (the ~price equivalent to $4.50 corn) translates into $7 soybeans in Mato Grosso. But $7 is the breakeven price for the average producer in the state (See Exhibit 4) according to IMEA, the Mato Grosso Institute for Agricultural Economics. Put another way, half of the soybean producers in Mato Grosso, comprising ~5% of worldwide soybean production, would be below breakeven in a $4.50 corn/$10 soybean environment. $10 soybeans might not have an immediate elect on soybean acreage because Brazilian farmers typically buy inputs and market their crops in advance. So it could take $4.50 corn/$10 soybeans lasting a full year for soybean acreage to drop significantly.

Additionally, at $4.50 corn, we would anticipate much less corn acreage in the second crop. Based on crop budgets from IMEA it will cost ~$2.50 to grow a bushel of second crop corn in 2014. "is breakeven at ~$5.00 corn given that IMEA estimates it costs another $2.50 a bushel to truck corn from the interior to the major grain exporting ports. Second crop corn would at best be a breakeven proposition at $4.50-$5.00. We would see some acreage planted as farmers need a cover crop, but it will be significantly less than we saw in 2013.

Here is a link to the full report.

Farmers respond to higher prices by planting more in an effort to capture as much benefit as possible. Inevitably supply increases. In the period from 2006 relatively high historical prices have been sustained for lengthy periods of time. The weak Dollar, high cost of energy, inclement weather, expensive nutrients and rising labour costs all contributed to this situation but the effect has been that supply increased nonetheless.

Corn is now back testing the 2009 lows near $3 and is oversold by any measure. An open question at this stage is whether lower energy prices will ameliorate the upward pressure on the cost of production seen over the last decade and whether a firmer Dollar will contain speculation over the lengthy medium-term. In the upcoming planting season however, the attraction of corn at $3.50 is not the same as it was at double the price this time last year so there is potential that prices are close to a meaningful low.

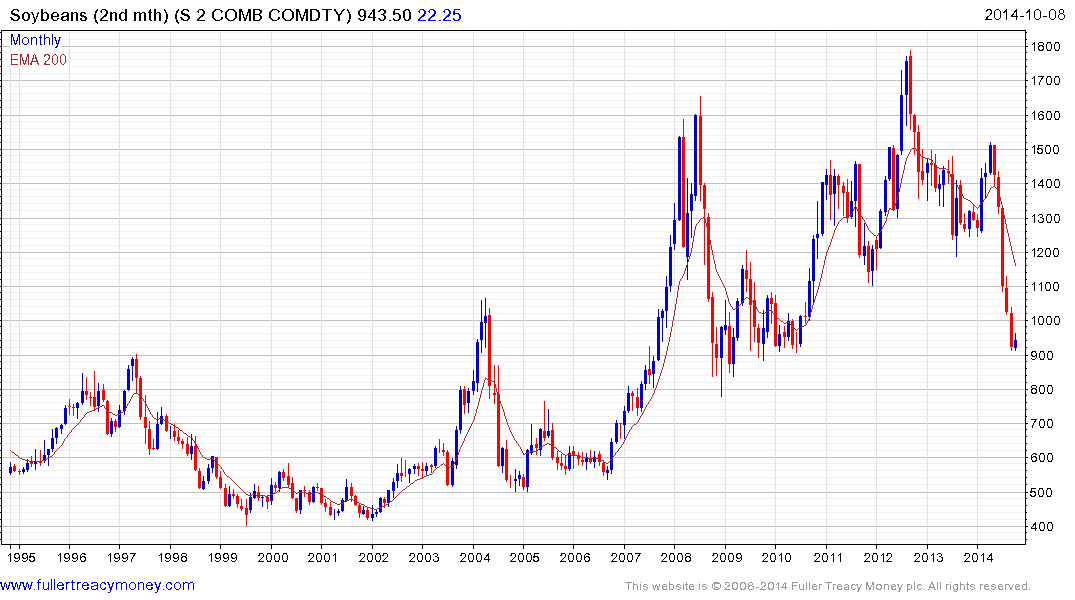

Soybeans has also fallen precipitously to form a deep oversold condition and is back testing the 900¢ area. It has at least paused this week but will need to hold the low above 900¢ to begin to suggest short covering is a short-term possibility.

Back to top