London House Prices Fall Most Since Financial Crisis

This article by Jill Ward for Bloomberg may be of interest to subscribers. Here is a section:

In London, values fell for a sixth consecutive month. If the provisional estimates are confirmed, the average price of a home in the capital was less than 582,000 ($773,000), the lowest since the end of 2015.

The downbeat picture was confirmed in a separate report from Rightmove Plc, which said asking prices in London fell an annual 2.5 percent in October. While they rose 3.1 percent on the month, driven by owners of more expensive properties, achieving these prices is far from assured as buyers now have more choice, according to Rightmove director Miles Shipside.

Values at the top end of the market have come under the most pressure, with prices falling in almost half of London’s 33 boroughs in the year through August, according to Acadata. It illustrates the toll being taken by Brexit uncertainty, higher property taxes for landlords and the prospect of the Bank of England raising interest rates for the first time in a decade.

Increasing supply is finally beginning to come to market in London at just the same time that property taxes have risen and the Bank of England’s looks likely to raise rates.

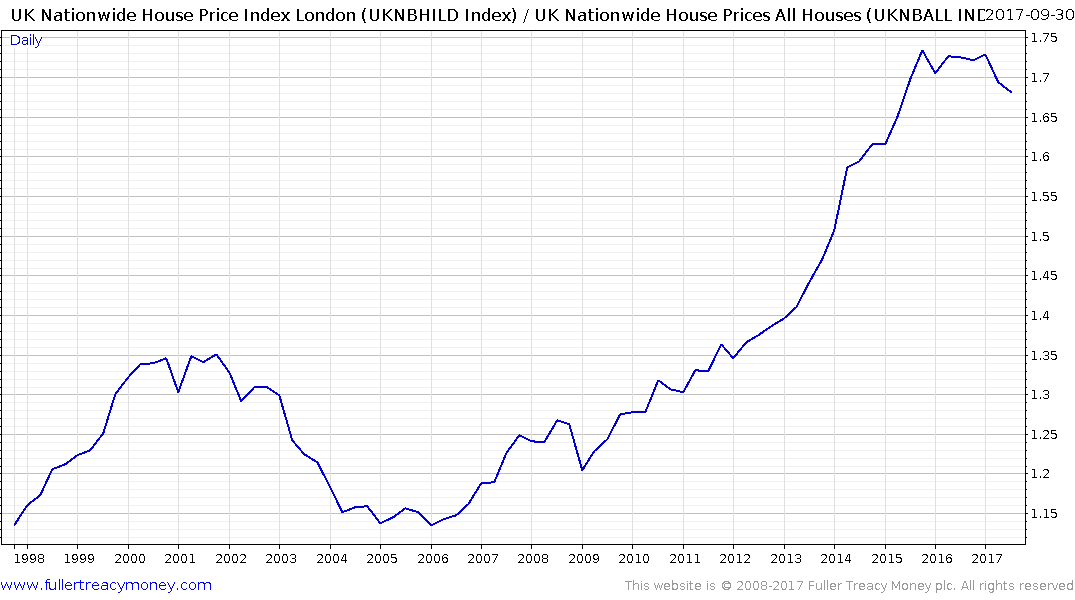

London property prices outperformed the UK average by a wide margin over the last decade but that trend is looking increasingly top-heavy; suggesting both a relative and absolute decline cannot be ruled out.

.png)

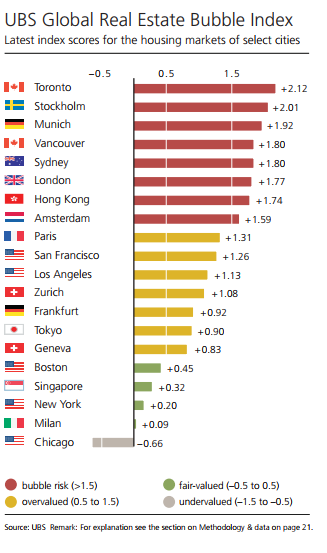

This report from UBS highlights the fact that along with Toronto, Stockholm, Munich, Vancouver, Sydney, London, Hong Kong and Amsterdam are among the most expensive markets in the world.

Here is a section:

Looking back at boom-bust periods of housing markets in the last 35 years, we infer that fundamentals matter. Nine out of 10 real estate crashes of at least minus 15% were preceded by a distinct overvaluation signal based on the UBS Global Real Estate Bubble Index methodology. Real-time calculations derived from it for the period 1980 to 2010 estimated the likelihood of a crash after a bubble-risk warning signal within the subsequent 12 quarters at 50–60%. This compares to an ex-ante probability of a real estate crash of about 12% in a given quarter during that time.

The caveat is that the model has delivered warning signals too frequently and too early for some markets, especially in recent years when the unprecedented quantitative easing programs of central banks distorted market incentives. Risk-averse investors would have missed out on exceptional capital appreciation opportunities. Nevertheless, taking less risk in overheated markets has historically paid off on average: they delivered worse returns over a full boom-bust period than more balanced markets did.

Uncertainty around Brexit and what it means for foreign investors represents a unique challenge for London property and suggests continued easing is likely, at least until greater clarity on what the country’s position relative to the EU is going to be.

Back to top