Lithium and cobalt a tale of two commodities

Thanks to a subscriber for this report from McKinsey which may be of interest to subscribers. Here is a section:

Here is a link to the full report.

Here is a section from it:

As a result, the recent price spikes for lithium and cobalt have resulted in many battery producers working to reduce the overall material needed per kWh and additionally focus on less cobalt-intensive chemistries. Consequently, NMC chemistries have become automotive OEM’s preferred technology in recent years. In the last few months, NCA technologies have pulled ahead; Tesla, which used the NCA technology for its Model S, now deploys a higher performing version for the Model 3 with even less cobalt than an NMC 811 and is working towards reducing the volume of cobalt contained in future batteries.

Exhibit 3 shows the impact of increasing cobalt and lithium prices on the battery pack price, which demonstrates that while lithium prices do influence battery cost, overall battery economics are more sensitive to cobalt prices. It is important to note that while changes in battery raw materials prices will only increase vehicle costs by approximately USD 100 per vehicle, and hence will likely not be a “show stopper,” there is increasing concern regarding raw material availability (especially that of cobalt). This concern is increasing the focus on low cobalt batteries and, as a result, the high-performing, low-cobalt, high-nickel NMC 811, and perhaps even the newly proposed NMC 9.5.5 battery (with 9 parts of nickel, and 0.5 of cobalt and manganese).

An industry can progress from a developmental stage to global domination if it is held hostage by commodity prices. That is the fallacy which proponents of the bull market in cobalt have been lured into accepting. The simple fact of the matter is that if cobalt is rare and the global industry needs lots of it, then either the global industrial expansion stalls or it finds a way to progress without cobalt.

Cobalt dropped below its trend mean this week. It’s p&f chart is a picture of how accelerating trends eventually roll over and reminds me of uranium’s peak in 2005.

Lithium remains the primary feedstock for batteries and it is relatively abundant so there is less of an argument for substitution. In fact, investment in additional sources of supply are coming to fruition with increasing volumes reaching market which has weighed on related equities.

Orocobre which is close to a pureplay on lithium is currently holding in the region of A$5 which represents the upper side of the underlying range. It needs to continue to hold that level if medium-term scope for continued upside is to be given the benefit of the doubt.

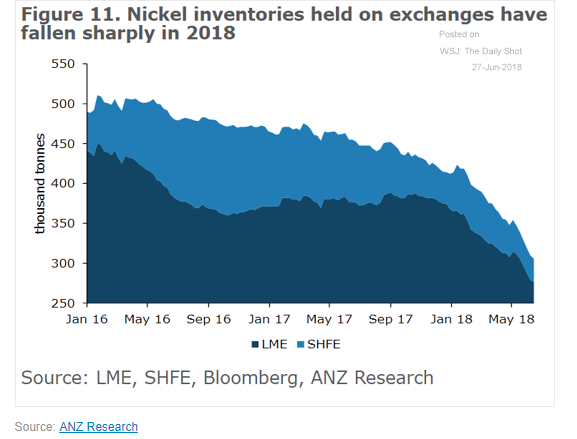

If cobalt is a potential loser from the evolution of battery technology, nickel could be a winner since there is a dearth of nickel sulphide supply. LME nickel contracts accept lower qualities of nickel than are required for batteries so some investment in additional higher-grade mining or refining will be required to meet demand from the battery sector. At present Nickel inventories are the lowest in years on the LME and in China.

ETFS Nickel has paused in the region of the April peak near $15 and some consolidation is underway. However, a sustained move below the trend mean would be required to question medium-term scope for continued upside.