Last Lifelines Crumble for Many Greek Families as New Conflict With Creditors Looms

This article by Nektaria Stamouli for Wall Street Journal detailing the human cost of Greece’s economic retrenchment may be of interest to subscribers. Here is a section:

The three-way conflict simmered throughout 2016. Eurozone policy makers say its resolution can’t be put off much longer. Prime Minister Alexis Tsipras is considering the option of snap elections if the creditors don’t soften their positions.

?The IMF is holding a hard line partly to put pressure on the eurozone to lighten Greece’s debt burden, say people involved in the negotiations. IMF officials have said Greece’s economy is already overtaxed.

New taxes that came into effect on Jan. 1 are squeezing household incomes further. Economists say even-higher income taxes—in the form of lower tax-free income allowances—could add to a mountain of unpaid taxes. Greeks currently owe the state €94 billion ($99 billion), equivalent to 54% of gross domestic product, and rising, in taxes that they can’t pay. Three in four Greeks can’t pay household bills on time, according to the 2016 European Consumer Payment Report, a private-sector survey.

Extended families often rely on grandparents’ pensions. Further cuts in that lifeline could end hopes for a return to economic growth. Unemployment remains more than double the eurozone’s average at 23%. About 74% of the jobless have been out of work for more than a year and thus receive no benefits.

Here is a PDF of the above article.

Greece got itself into a world of trouble by fudging economic statistics to gain entry to the euro. By succeeding in that endeavour it paid scant regard to its ability to pay back the vast quantities of money subsequently borrowed and the generous social programs it funded.

However the reality now is that Greece is a nation state with no chance of recovery and its fate is tied inextricably to the German electoral calendar. Regardless of how much pressure the IMF puts on Greece to cut deeper in order to encourage the EU to grant debt relief nothing is likely to happen until at least October because mercy towards Greece would virtually ensure Angela Merkel loses her job.

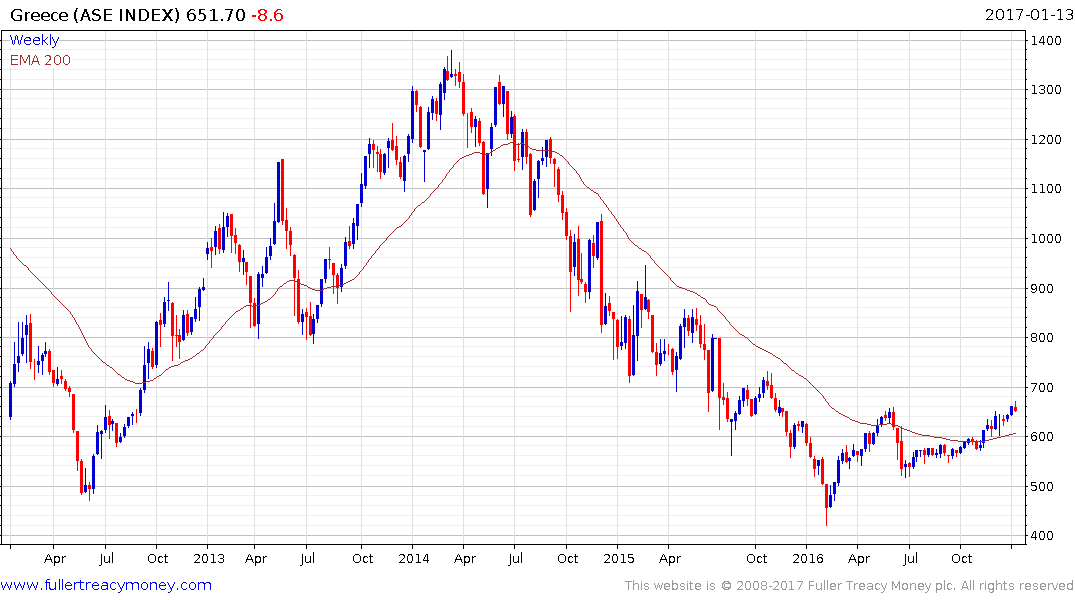

Greek government bond yields show no sign the ECB has abandoned the market.

The stock market failed to hold the lows posted in January 2016 and is now trading back above the trend mean. That suggests investors are willing to wager a lot of the bad news is already in the price and that perhaps Greece will benefit from a possible turn towards fiscal stimulus if populist parties prevail in French, Dutch and/or German elections.

Back to top