Kuroda Departs Leaving $11.7 Trillion Experiment to Successor

This article from Bloomberg may be of interest. Here is a section:

“Kuroda will be recognized as having been an outstanding central bank governor who has been quite innovative,” former International Monetary Fund chief economist Kenneth Rogoff said. “The BOJ under Kuroda has forcefully adopted more or less every idea there is for raising inflation expectations, but until recently, to no avail.”

At Kuroda’s last Group of 20 meeting in Bengaluru, India, in late February, central bankers and finance ministers from across the globe rose to their feet to applaud the ever-smiling governor. European Central Bank President Christine Lagarde was one of the first to clap, according to people familiar with the matter.

“Haruhiko Kuroda is a master of his trade. He steered the monetary policy of Japan through challenging times. These are big shoes to fill for any successor – and times are certainly not getting any easier,” said Swiss National Bank President Thomas Jordan. “It was always a pleasure to have in-depth discussions with him over dinner, ranging from culture to economics to politics.”

I don’t think there is nearly enough of questioning whether it was possible for Japan to create inflation when the global economy was in a disinflationary trend for decades. Japan is a highly open, developed economy. The money created by the Bank of Japan did not stay at home but was invested abroad in an aggressive manner. That leakage did not create the upward pressure on wages to break the deflationary trend. Against a background of demographic contraction and the related lack of credit demand it was likely impossible to create an inflationary trend.

Perhaps the greatest the proof point that an open economy can’t do it alone, is it was only when other central banks adopted Japan’s playbook that inflation took off. The big question at present is how committed to yield curve control the new Bank of Japan governor will be? It seems to me that is a backward way of thinking. It is better to think about whether the inflationary trend can persist without literally handing free cash to the population.

The IMF is predicting low growth over the coming 5 years as the pandemic excesses are paid down. That could be a generally benign environment for bonds because the secular stagnation theme is likely to be revitalised. That of course assumes excessive money supply growth is avoided or very temporary during the next recession.

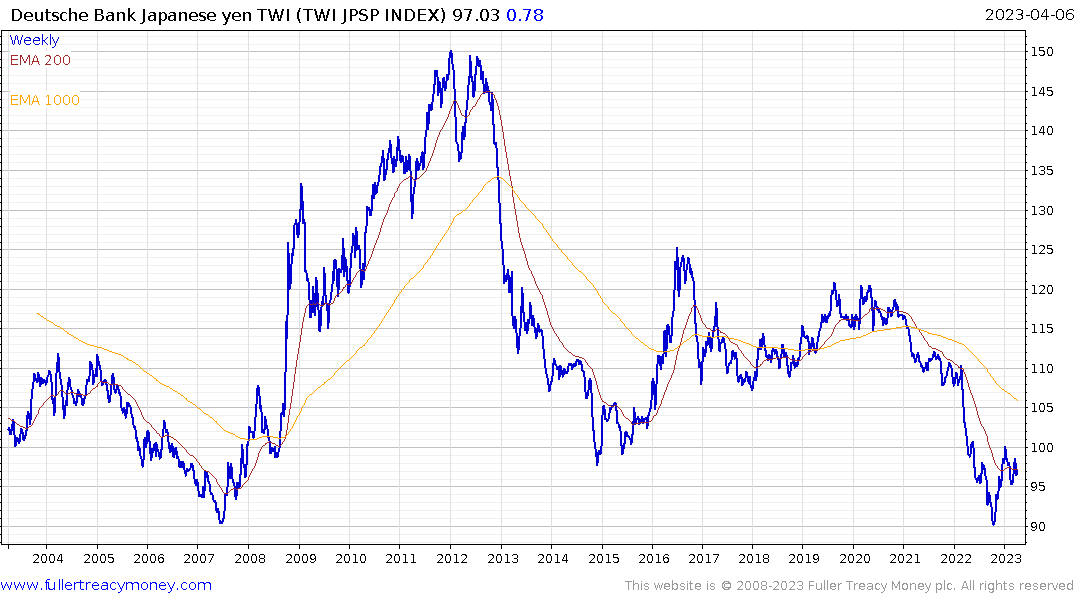

The Deutsche Bank Yen Trade Weighted Index is firming from the region of the 2008 lows. Firmer action supports the view the fountain of liquidity emanating from the Bank of Japan may be coming to an end.

The Deutsche Bank Yen Trade Weighted Index is firming from the region of the 2008 lows. Firmer action supports the view the fountain of liquidity emanating from the Bank of Japan may be coming to an end.

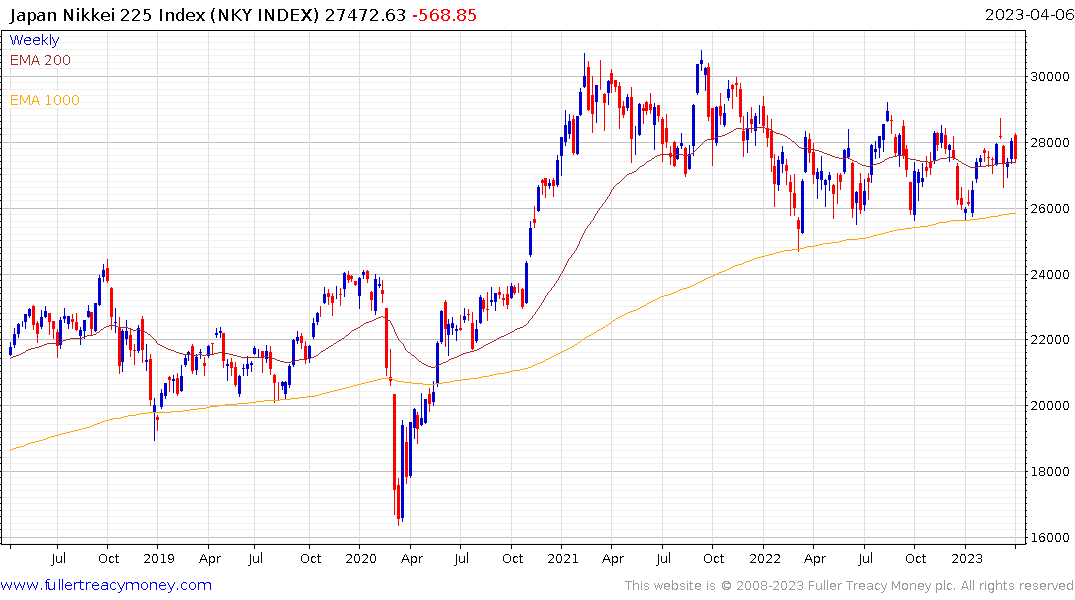

Meanwhile the automotive sector remains under stress and the Nikkei-225 is weakening within a yearlong range.

Meanwhile the automotive sector remains under stress and the Nikkei-225 is weakening within a yearlong range.