Jeremy Grantham Warns of a 17% Plunge in the S&P 500 This Year

This article from Bloomberg may be of interest to subscribers. Here is a section:

Grantham views the process of further stock market pain playing out now as similar to the popping of bubbles following other rare “explosions of investor confidence” such as in 1929, 1972 and 2000. While many are attributing last year’s slide in stocks to the war in Ukraine and the surge in inflation, or reduced growth from Covid-19 and ensuing supply chain problems, Grantham believes the market was due for a comeuppance regardless.

While the first and “easiest” leg of the bubble’s bursting is over, Grantham says that the next phase will be more complicated. Seasonal strength in the market in January and during the current period of the presidential cycle could keep the market buoyant in the early part of the year. “Almost any pin can prick such supreme confidence and cause the first quick and severe decline,” he wrote. “They are just accidents waiting to happen, the very opposite of unexpected. But after a few spectacular bear-market rallies we are now approaching the far less reliable and more complicated final phase.”

Here is link to the full note.

I was at dinner last night with some very successful elderly investors who chastised me for being too bearish. Their contention was that the lows were posted in October and the market always bottoms ahead of earnings. So let’s consider the argument that the October nadir is unlikely to be exceeded.

The biggest bullish argument is high yield spreads are contracting. If there were truly imminent risk in the credit markets, it is reasonable to expect investors to be leery of buying bonds even at nominal rates approaching double digits.

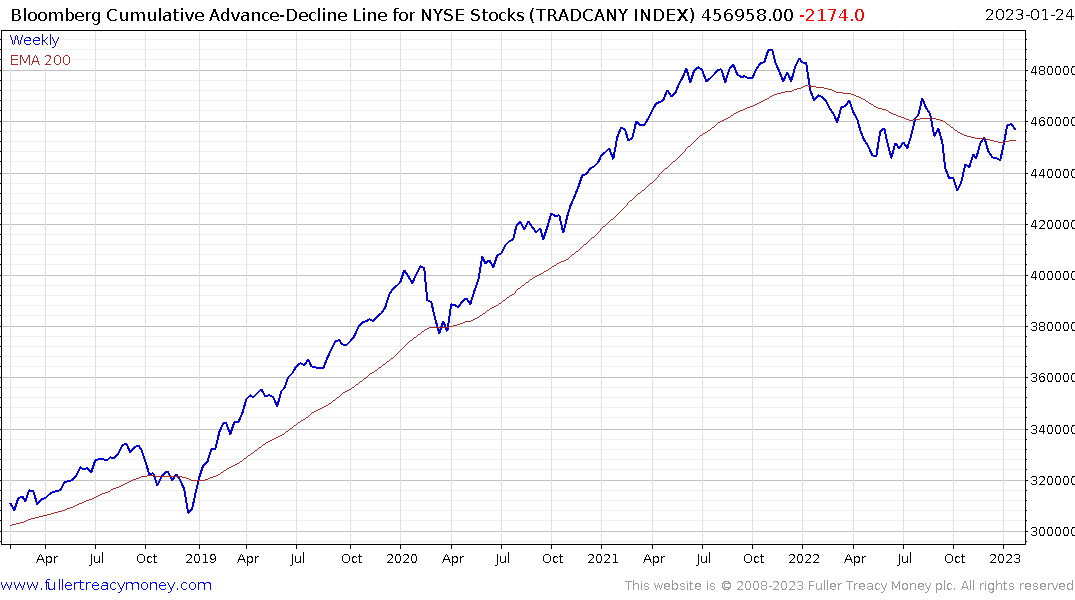

The second argument is the Advance-Decline Line for the NYSE has now broken its downtrend. Together with the steep recovery in the number of stocks trading above their 200-day MAs, that confirms more stocks are rising than falling.

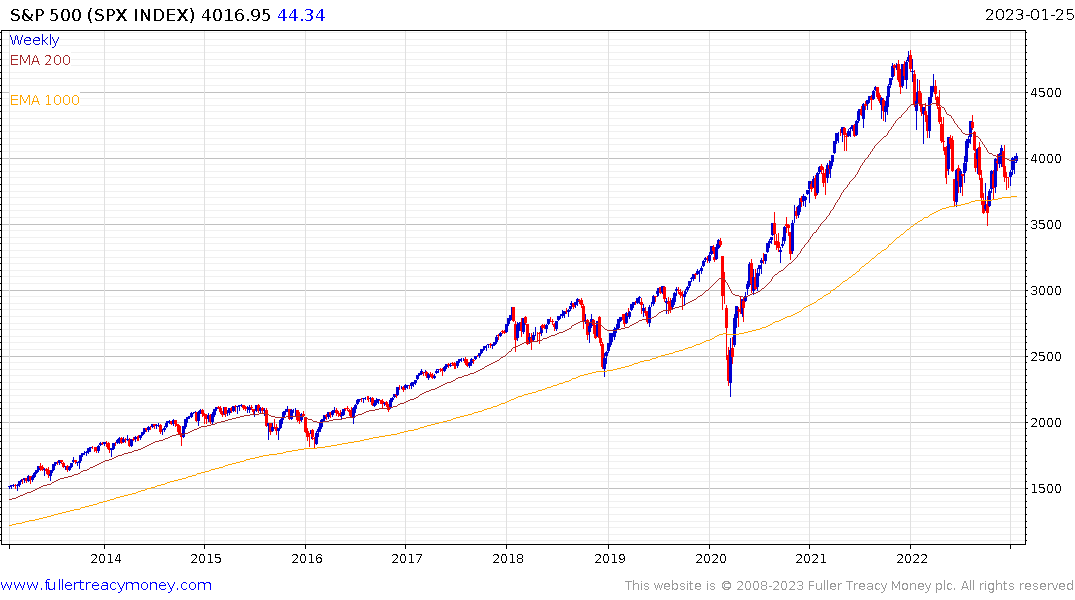

The next argument is the market has fallen enough, support has been found in the region of the 1000-day MA and the secular bull market is still intact. This has been nothing more than a medium-term correction in an ongoing bull market.

The next argument is the market has fallen enough, support has been found in the region of the 1000-day MA and the secular bull market is still intact. This has been nothing more than a medium-term correction in an ongoing bull market.

Together these arguments are enough to sustain the current rebound in stock prices. The S&P500 could even rally as high as 4500. After that the big questions resurface.

The pace of monetary tightening is breathtaking. The pace of quantitative tightening is twice as fast as it was in 2018/19, money supply growth is negative, and the debt ceiling issue is drawing down the Treasury’s general account at the Fed. This all contributes to tighter liquidity.

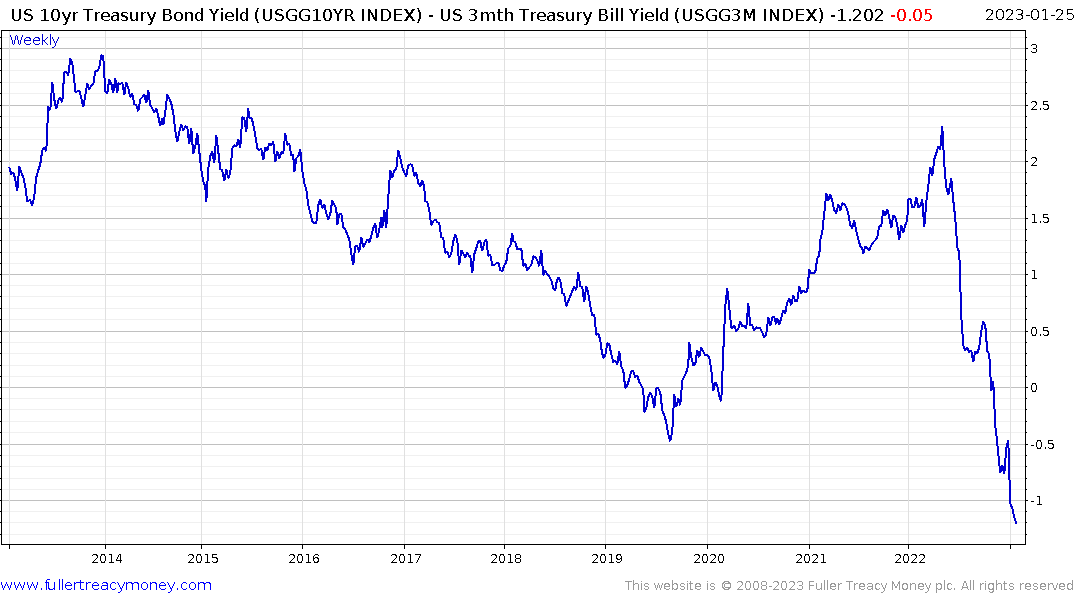

The yield curve is inverted at every point from 6-months to 10-years. The Muni curve was inverted at the end of 2022 and is now at 6 basis points and the junk yield curve is trending lower.

The yield curve is inverted at every point from 6-months to 10-years. The Muni curve was inverted at the end of 2022 and is now at 6 basis points and the junk yield curve is trending lower.

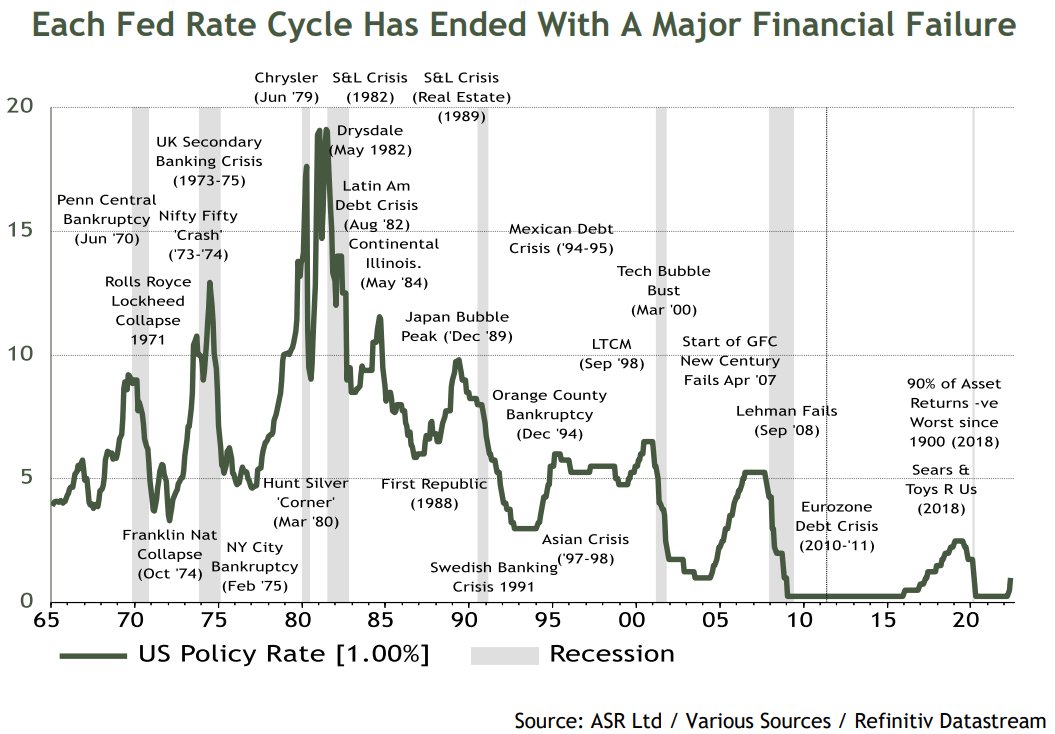

The only two things that will force the Federal Reserve to relent from holding rates at elevated levels are spikes in unemployment or a significant credit event. My bet is a credit event in private markets. Then, how much pain the regular economy experiences depends on how long high rates are sustained for.

The only two things that will force the Federal Reserve to relent from holding rates at elevated levels are spikes in unemployment or a significant credit event. My bet is a credit event in private markets. Then, how much pain the regular economy experiences depends on how long high rates are sustained for.