Iron ore price craters 8%

This article by Frik Els for Mining.com may be of interest to subscribers. Here is a section:

According to data released by the World Steel Association on Friday, Chinese output, which exceeds that of the rest of the world combined, in October rose 9% from the year before to a record 82.5m tonnes for the month. For the first 10 months Chinese furnaces pumped out 7.6% more steel. Numbers from China's National Bureau of Statistics have production jumping 14% compared to last year.

The ramp up comes ahead of winter production cuts mandated by Chinese authorities and healthy margins for the country's steelmakers, which have now evaporated.

In a note released before the recent pullback Capital Economics chief commodity strategist Caroline Bain, predicted more pain for iron ore prices ahead thanks to rising supply, sluggish demand from the property sector and a shift to electric arc furnaces as scrap availability inside China continues to expand.

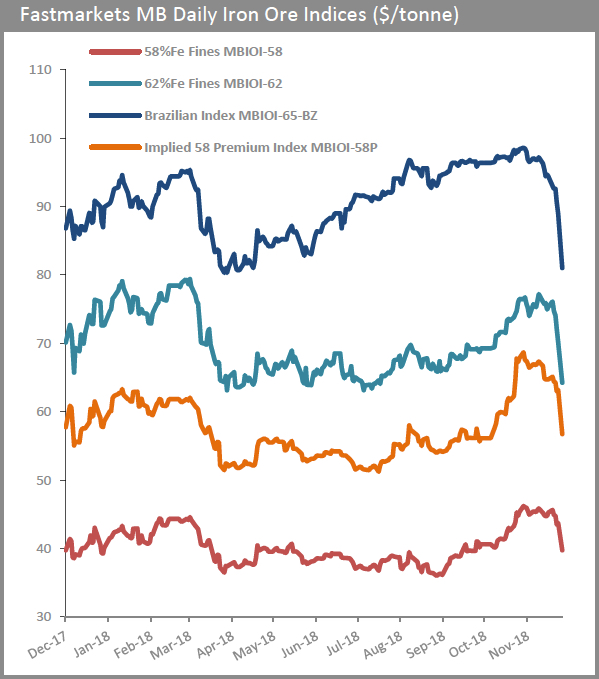

Capital Economics believes the price of iron ore had risen to levels not supported by supply and demand and is forecasting end-2019 level of $55 per tonne. One bright spot is the substantial premium paid for higher grade ore from top producers Brazil and Australia as Chinese steelmakers continue to reduce pollution.

Iron-ore demand has turned into a very seasonal business because of China’s desire to moderate emissions during the winter season when the country has been habitually blanketed in thick smog. That forces steel producers to stuff as much production into the 9 months outside the winter season as possible and contributes to less demand for iron-ore during that time. The economic slowdown and uncertainty about the property sector have been additional headwinds for the sector.

BHP is back testing the psychological 1500p level which represents a previous area of resistance and a psychological level. It will need to find support soon if the medium-term trend is to remain reasonably consistent.

Rio Tinto’s charts is similar to that of the FTSE350 Mining Index as it ranges below the trend mean. It needs to hold the 3500p level if medium-term top formation completion is to be avoided.

Vale failed to sustain the breakout above $15 in October and has returned to test the lower side of its underlying trading range. A short-term oversold condition is evident but a clear upward dynamic will be required to signal a return to demand dominance and confirm more than near-term support.

Australia’s Fortescue Metals remain in a consistent medium-term downtrend and confirmed resistance in the region of the trend mean again three weeks ago. A sustained move back above $4.30 will be required to question medium-term supply dominance.

Australia’s Fortescue Metals remain in a consistent medium-term downtrend and confirmed resistance in the region of the trend mean again three weeks ago. A sustained move back above $4.30 will be required to question medium-term supply dominance.