Investors Overseeing $5 Trillion Are Betting That an Economic Recession Can Be Avoided

Thanks to a subscriber for this article from Bloomberg which may be of interest. Here is a section:

Professional investors are loading up on bets that an economic recession can be avoided despite all the warnings to the contrary. It’s a dangerous bet -- for a variety of reasons.

Money managers have been favoring economically sensitive equities, such as industrial companies and commodity producers, according to a study from Goldman Sachs Group Inc. on positioning by mutual funds and hedge funds with assets totaling almost $5 trillion. Shares that tend to do well during economic downturns, like utilities and consumer staples, are currently out of favor, the analysis shows.

The positions amount to wagers that the Federal Reserve can tame inflation without creating a recession, a difficult-to-achieve scenario often referred to as an economic soft landing. The precariousness of such bets was on display Friday and Monday, when strong readings on the labor market and American services sectors drove speculation the Fed will have to maintain its aggressive policies, increasing the risks of a policy error.

“Current sector tilts are consistent with positioning for a soft landing,” Goldman strategists including David Kostin wrote in a note Friday, adding that the fund industry’s thematic and factor exposures point to a similar stance.

I am reminded of 2007 and 2008 when commodities were surging and banks beginning to roll over. At the time commodity inflation was running rampant but there was relatively little upward pressure on wages. The growing weakness in the housing sector effectively kept wage demand growth under control. Nevertheless, the spike in energy prices and overleverage in the financial system caused a significant problem.

This speech given by Ben Bernanke on June 9th 2008, discussing inflation, may also be of interest. Here is an important section:

Before turning to those issues, however, I would like to provide a brief update on the outlook for the economy and policy, beginning with the prospects for growth. Despite the unwelcome rise in the unemployment rate that was reported last week, the recent incoming data, taken as a whole, have affected the outlook for economic activity and employment only modestly. Indeed, although activity during the current quarter is likely to be weak, the risk that the economy has entered a substantial downturn appears to have diminished over the past month or so. Over the remainder of 2008, the effects of monetary and fiscal stimulus, a gradual ebbing of the drag from residential construction, further progress in the repair of financial and credit markets, and still-solid demand from abroad should provide some offset to the headwinds that still face the economy. However, the ongoing contraction in the housing market and continuing increases in energy prices suggest that growth risks remain to the downside.

One of the most effective means by which the Federal Reserve can help to restore moderate growth over time and to reduce the associated downside risks is by supporting the return of financial markets to more-normal functioning. We have taken a number of actions to promote financial stability and remain strongly committed to that objective.

The fact Ben Bernanke was still talking about a small threat of a large market dislocation in June of 2008 tells us all we need to know about the ability of central banks and economists to predict the magnitude of recessions. That does not imply the upcoming recession will be deep, but it is does not imply it will be shallow either.

The belief that a “return of financial markets to more-normal functioning” appears to still be the prevailing sentiment at the Fed, as a means to alleviate downside risks. They are intentionally siphoning money from the market in the hope of enacting a mild recession but the associated risk is a deeper contraction.

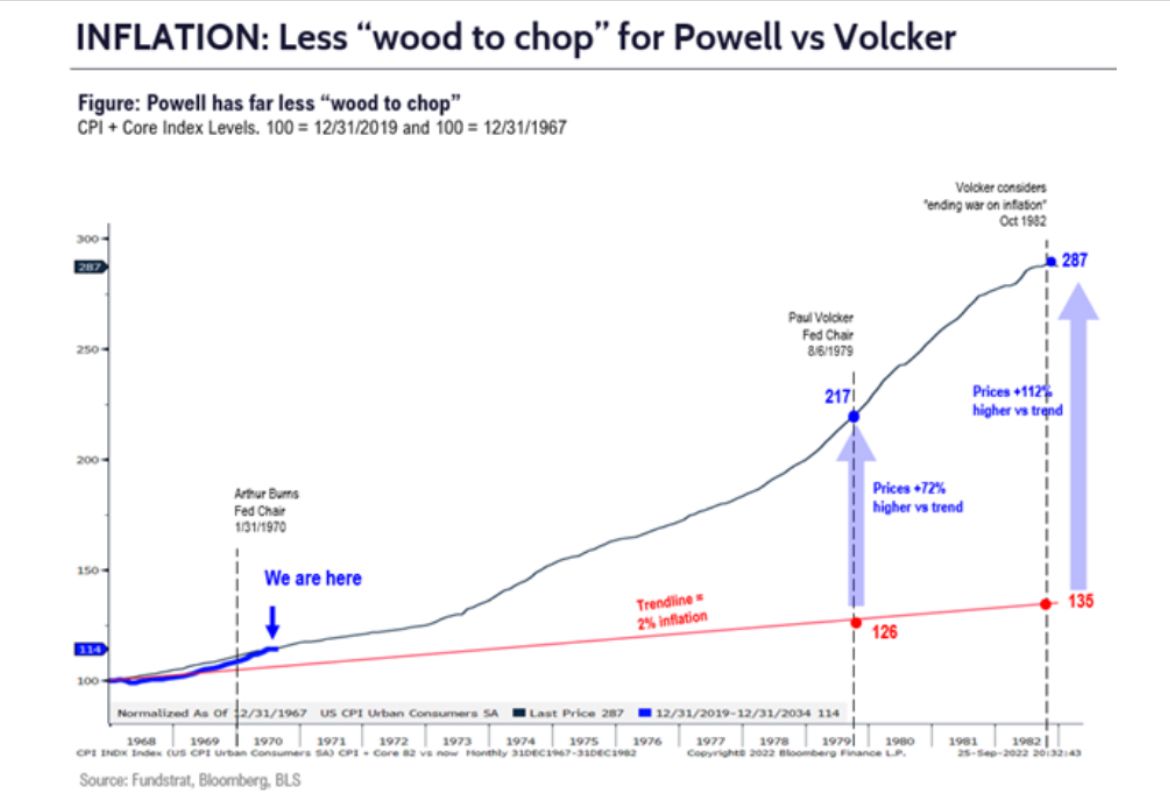

This graphic, kindly forwarded by a subscriber may also be of interest. It highlights just how large the inflation problem was in the 1970s compared to today. One has to think Federal Reserve officials are aware of the threat of inflation getting out of control. That suggests they will do whatever is necessary to quench inflation now. That suggests continuing to compress asset prices and kill excess demand.

This graphic, kindly forwarded by a subscriber may also be of interest. It highlights just how large the inflation problem was in the 1970s compared to today. One has to think Federal Reserve officials are aware of the threat of inflation getting out of control. That suggests they will do whatever is necessary to quench inflation now. That suggests continuing to compress asset prices and kill excess demand.

The risk is clear that the process gets out of control and a crash occurs. The 2008 analogue remains in play but the epicentre of risk on this occasion is with private assets. That suggests the pension, endowment and charity sectors will be most heavily affected. That will have tail risks for public cohesion because many public sector pensions will be in trouble.