Investment Strategy: "Charts of the Week"

Thanks to a subscriber for this report from Raymond James which may be of interest. Here is a section:

A link to the full report is posted in the Subscriber's Area.

Here is a section from it:

The massive shift to passive investing/ETFs benefits growth stocks at the expense of value stocks. Historically, active investors and portfolio managers have generally favored value strategies, buying stocks that are trading below a calculated intrinsic value and selling stocks that have risen above a calculated intrinsic value. However, as more money flows into products that “buy the market” or “buy a whole sector,” value is largely being thrown out the window. Instead, higher-growth stocks that are bid up to higher valuations rise in price/market cap and become even larger holdings within most of these funds, while stocks that fall in price/market cap become smaller holdings; there’s a built-in momentum factor at work that doesn’t exactly help stocks that are “undervalued.” We don’t think it’s a huge coincidence that the clear outperformance of growth over value going back to 2006 has occurred at the same time passive investing and index funds have proliferated.

On a closely-related note, it used to be costly and time consuming to buy and sell stocks, and it was near impossible for the average investor to try to duplicate an index or even to hold a large basket of stocks in a portfolio. As a result, more emphasis was placed on finding the sub-section of stocks that represented an exceptional value opportunity and then holding them until they were no longer good values (or paying an active manager to find those opportunities). Now, online brokers offer $1 commission stock trades (or less), and just last week, Fidelity rolled out two 0% management fee index funds that enable investors to own, essentially, the majority of the world stock market’s capitalization at no cost. The ability to trade so quickly and cheaply we feel has helped to cut down on holding times and has prompted investors to chase quarterly earnings growth and near-term performance, further skewing the market toward momentum and growth stocks. Moreover, the easier and cheaper investing becomes, the more money that goes directly into stocks, and since that money is increasingly going toward passive strategies and growth stocks these days, it’s almost become a self-perpetuating cycle.

With the broad stock market consistently seeing “higher than average” valuations and generally rising over the last few years, it’s simply meant there are fewer attractive value opportunities overall. Investors have, therefore, piled into stocks with greater earnings growth potential that can better justify the higher valuations. It should not come as a complete surprise that, since 2006, the periods when value has been the better performer have come AFTER meaningful sell-offs in the broad market (again see page 13). We think these sell-offs have helped create more value opportunities when they occur, and relative performance improves while those beaten down companies return to fairer valuations. As a result, it may require more of a significant decline in the broad market to put the wind at the backs of value stocks again.

Value strategies work best in distressed situations when solid cash generative assets are sold off because of contagion from a market dislocation. That affords patient investors the opportunity to pick up assets at very attractive levels with a view to holding them for the lengthy medium-term. Outside of those periods of market stress it can be slim pickings for value investors.

One additional idiosyncrasy of the sector is that just about all value investors use similar metrics so they do tend to end up with similar looking portfolios with the major differences being concentration. One of the primary challenges for value today is the potential for technological disruption to represent a trap for strategies which have worked reliably for decades.

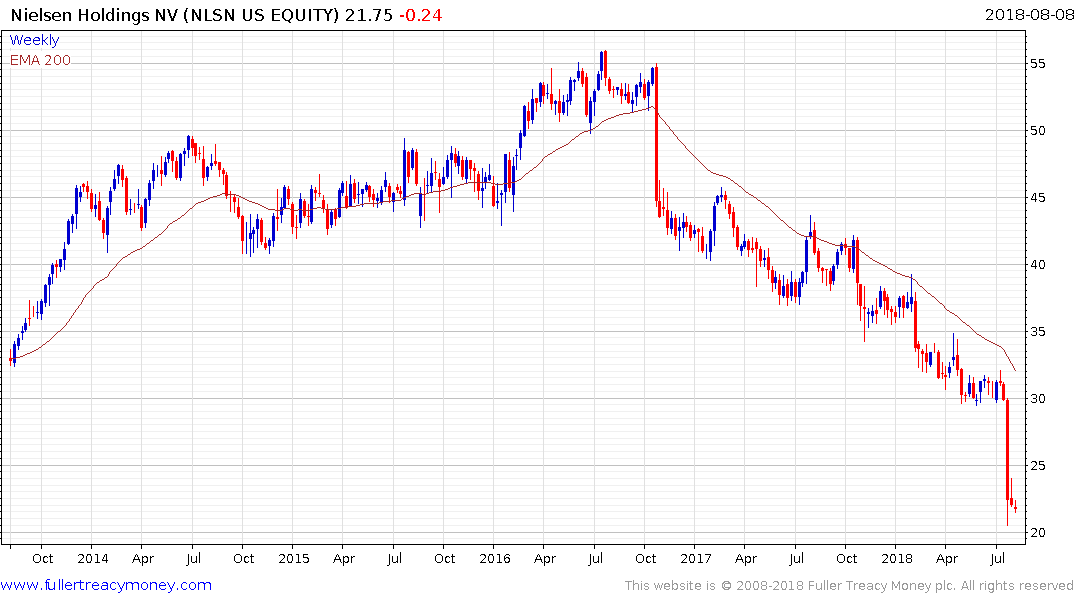

For example, if we look at Nielsen which has a dominant position in the television ratings sector. It has $1.191 billion in free cash flow versus a market cap of $7.711 billion which is a free cash flow yield of 15%. It has dividend yield of 6.3%. It debt to assets are at 50% and the next maturity is in 2020. By the metrics it’s an attractive value proposition and the price has accelerated lower so there is ample scope for a rebound. The big medium-term question is whether the company will still exist in the early 2020s considering the effect Netflix and streaming is having on the cable TV sector.

Hanesbrands is another example. The company is as synonymous with covering the nether regions of the US population as Marks & Spencer is for the UK population. It does approximately $568 million in free cash flow on a market cap of $6.714 billion for a free cash flow yield of 8.4%. The dividend yield is 3.22% and it is trading on a forward P/E of 10.62 with price to sales of 1. By conventional metrics that’s an attractive value proposition. The big question is whether the push by companies like Amazon and Target to sell own brand essentials will prove a death knell for Hanes. The share has halved from its 2015 peak and stabilised this week above the May low.

Buy and hold strategies work best in the mid to latter stages of a bull market because occasional reactions are continually resolved with successful upward breaks. That contributes to the perspective that the only way to prosper is to stay long. The concentration of market cap weighted indices in the largest companies means passive strategies are closet momentum strategies. When the leaders in the bull market eventually turn the exit from passive strategies is likely to have a severe knock-on effect for the wider market

Back to top