Internet Trends 2019

This report from Mary Meeker at Bond includes a large number of graphics which may be of interest to subscribers. Here is a section from the introduction:

The rapid rise of gathered / analyzed digital data is often core to the holistic success of the fastest growing & most successful companies of our time around the world. Context-rich data can help businesses provide consumers with increasingly personalized products & services that can often be obtained at lower prices & delivered more efficiently. This, in turn, can drive higher customer satisfaction. Better data-driven tools can improve the ability for consumers to communicate directly & indirectly with businesses & regulators.

Core constituents (consumers / businesses / regulators) are increasingly drinking from a data firehose & management challenges continue to rise for all parties. Broad awareness of challenges (& related vigorous / heated debates) can be the first step in driving change.

Consumers are aware of concerns about Internet usage overload & are taking steps to reduce usage – leading USA-based Internet platforms have rolled out tools to help monitor usage & social media usage growth appears to be decelerating following a period of strong growth. Privacy & problematic content concerns are also top-of-mind & are following similar patterns.

Owing to social media amplification, reveals / actions / reactions about events can occur quickly – resulting in both good & bad outcomes. In markets where online real-time rating systems exist, accountability can be improved vs. offline options as consumers & businesses interact directly while regulators can also benefit.

Rapidly expanding connectivity has helped amplify voices of good & bad actors. This has brought new focus to an age-old challenge for regulators around the world – finding the most effective ways to amplify good & minimize bad, often resulting in different regional interpretations & strategies.

Here is a link to the full report.

The march of technology and pace of innovation as massive data sets are parsed, managed and exploited has helped to drive the bull market in data centres and the resulting cloud-based product offerings. That remains a powerful trend because new business models are springing up to lever the potential for costumer engagement from automating the product offering to cater to user demand. That represents a reversal of the traditional product to customer model and is a primary trend behind the creation of new companies.

The big question for investors is how much of this is already in the price? The performance of new companies tends to be susceptible to overhyping and collapses when sale growth does not keep up with inflated expectations.

2U has been instrumental in helping universities deliver course material online. That did not stop the share from dropping 60% over the last 12 months following a reassessment of its growth potential.

Stitch Fix initially did well following its IPO but a growth scare resulted in the share giving up all of its advance. It has since stabilised and may be on the cusp of completing a base formation.

Shopify remains in a steep uptrend but the first clear downward dynamic is likely to signal a peak of at least near and potentially medium-term significance.

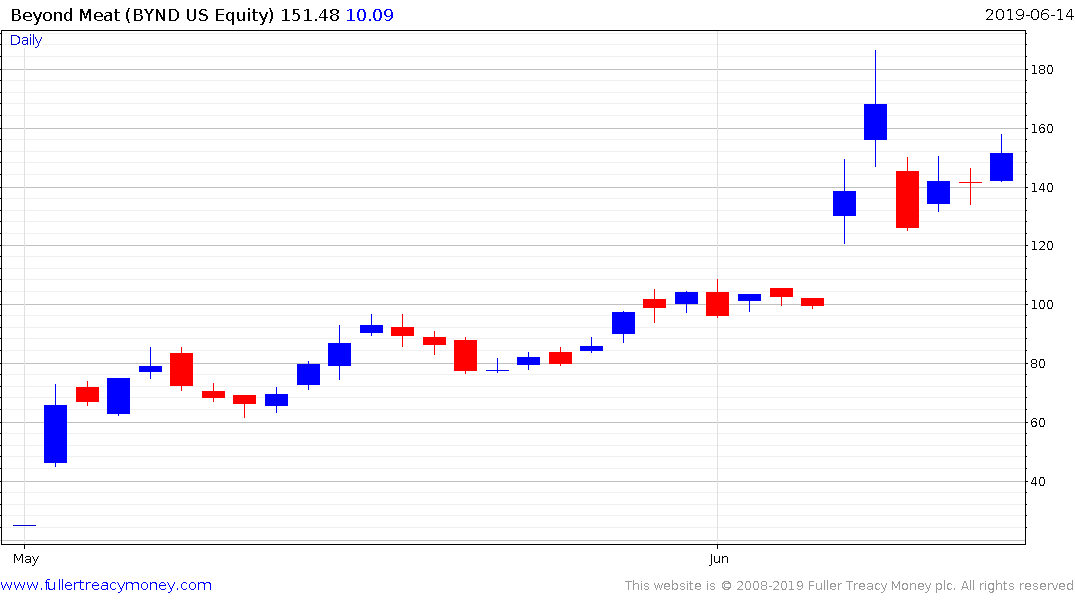

Beyond Meat’s rise remains underway as well.

Twilio is trading on an Estimated P/E of 1192 but continues to hold a sequence of higher reaction lows.

Perhaps the most telling trend of all is the pace of IPOs hitting the market. Uber and Lyft have stabilised following some tumultuous trading but there is a queue of companies ready for listing with Splunk being the highest profile this week.

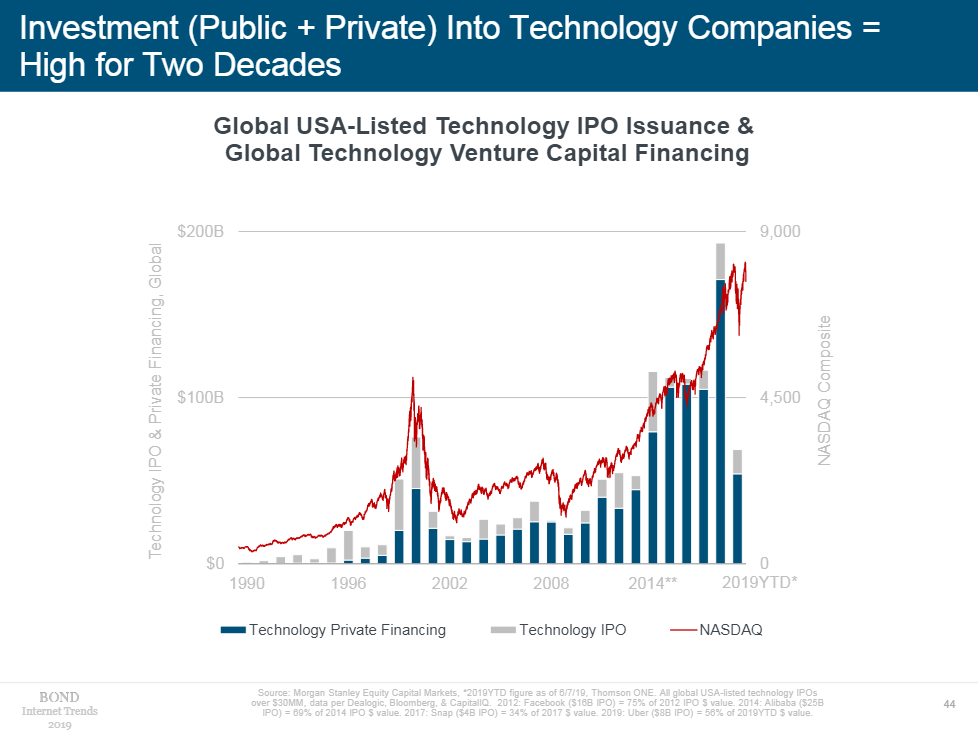

This chart from Meeker’s report highlights the fact P/E investment is below trend so far this year compared with last-year’s record. That suggests funds are more interested in exiting than entering the market. That gels with the sentiment among CFOs, with two thirds expecting a recession by the end of next year.

More than anything else, these considerations suggest major investors have stopped buying and are waiting for confirmation of a resumption of the trend to re-engage. That’s typical of investor activity following a massive reaction against the prevailing trend like we saw in the fourth quarter. One of the reasons why the Fed’s statement this week is being watched so carefully is the bond market has priced in a cutting cycle. It will need to be delivered upon, without stoking fears of a recession, if stock market sentiment is to remain bullish.

Back to top