India Strategy Outlook 2012

Corporate India was seen tired and helpless towards the end of year, with most giving up hope for a revival in the short term. The long term India growth stories were seen to fade, even though there were silver linings in most of the developments that may be structurally positive in the long term. The cleanup act of the system continued with visible enforcement of law towards those who flouted the same and the Supreme Court was seen active in pinning those where linkages of scams or wrongdoings were noticed, which gives hopes for a better judiciary in the country.

As we enter the NEW CY12 with lot of negative developments in CY11 and sharp correction in markets, we strongly believe that the 'negatives' are at their peak or near peak on the domestic economic front and corporate performance are at their bottom or near bottom The word 'near' should be read with a bottom. near margin of safety for a quarter, from where we may see reversals in domestic macroeconomic and corporate performance. Fall in Inflation may prompt cut in interest rate, as indicated by RBI, IIP numbers may improve and corporate earnings may brighten from 2nd quarter of CY12. The major risk remains on the political front with elections in 5 key states, the result of which may determine the fate of the government and their reforms agenda.

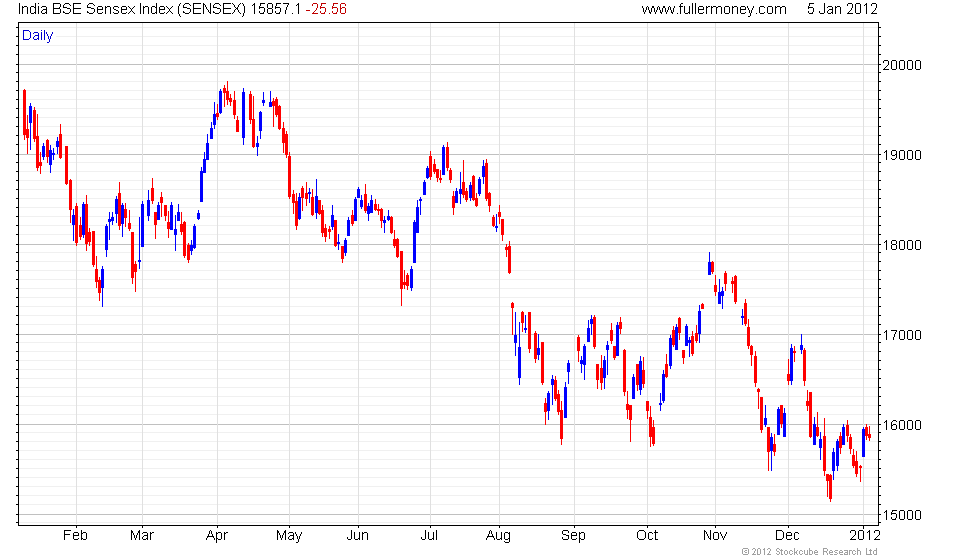

David Fuller's view Foreign Direct Investment (FDI) is probably

the world's most fungible commodity. India (historic,

weekly & daily)

has frightened FDI away through its bureaucratic bumbling and corruption. These

are self-inflicted wounds and most Indians deserve better.

Any

historically undervalued stock market is interesting by definition. Nevertheless,

international investing is a global beauty contest. Other stock markets currently

look more alluring, in terms of governance, valuations and relative strength.

I

will retain my personal long-term investment in India because I think Microsec's

optimism is probably justified. However, having often increased my investment

in this market following previous downturns since 2003, I am less tempted to

do so now. Nevertheless, on looking at India's historic chart above for perspective,

or better yet recreating it in the Library and using the 'Tracker On' facility,

we can see that the Sensex Index rose from approximately 113 in 1979 to 21,207

in 2008. That high was retested in 2010. If India's best economic days lie ahead,

as many of us believe because it is still very much an emerging market, the

next sustained break to new all-time highs should open the door to another huge

advance. The only problem - India's poor governance has most likely pushed that

opportunity further into the future.

{kind=link}