In strategy shift, CalPERS looks to cut financial risk

This article by for the Los Angeles Times may be of interest to subscribers. Here is a section:

But even its staff acknowledges in a recent report that despite fast-rising contributions from taxpayers, the pension fund faces "a significant amount of risk."

To reduce that financial risk, CalPERS has been working for months on a plan that could cause government pension funds across the country to rethink their investment strategies.

The plan would increase payments from taxpayers even more in coming years with the goal of mitigating the severe financial pain that would happen with another recession and stock market crash.

Under the proposal, CalPERS would begin slowly moving more money into safer investments such as bonds, which aren't usually subject to the severe losses that stocks face.

Because the more conservative investments are expected to reduce CalPERS' future financial returns, taxpayers would have to pick up even more of the cost of workers' pensions.

Most public workers would be exempt from paying any more. Only those workers hired in 2013 or later would have to contribute more to their retirements under the plan.

The changes would begin moving CalPERS — which provides benefits to 1.7 million employees and retirees of the state, cities and other local governments — toward a strategy used by many corporate pension plans. For years, corporate plans have been reducing their risk by trimming the amount of stocks they hold.

With an unfavourable demographic profile many pension funds are being forced into increasing their weighting in bonds so that they can reduce risk in the distribution phase of retirement programs. This is regardless of the fact that government bond yields are low. This policy ensures additional funds will be required to make up for any shortfalls and/or benefits will be cut.

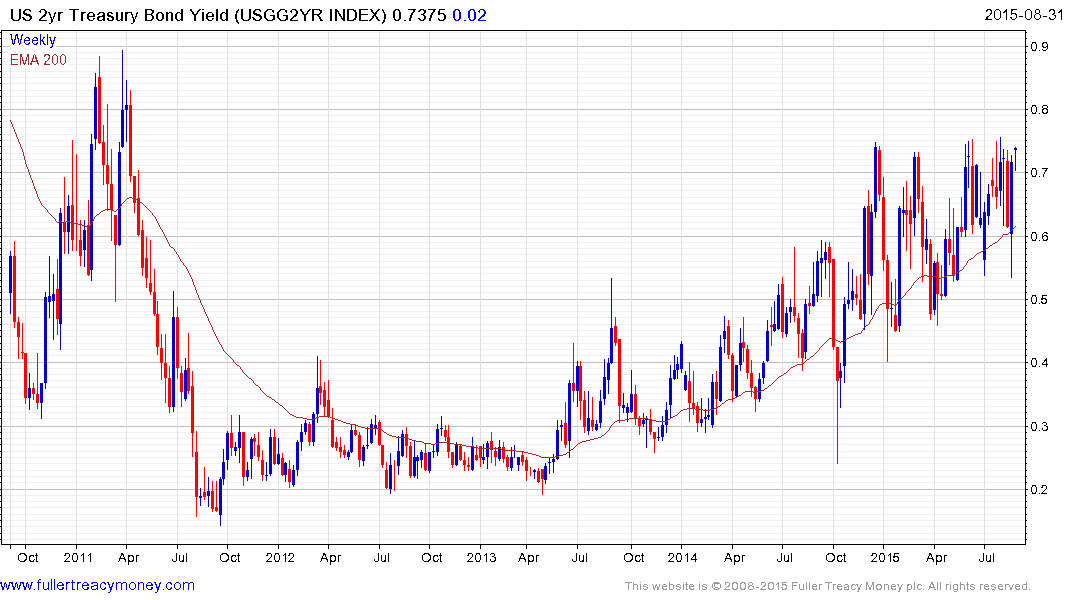

Government bond yields are pricing in an interest rate hike rather than to the migration of pension assets. The 2-year is testing the upper side of an almost year long range and a sustained move below the 200-day MA would be required to question medium-term scope for additional upside.

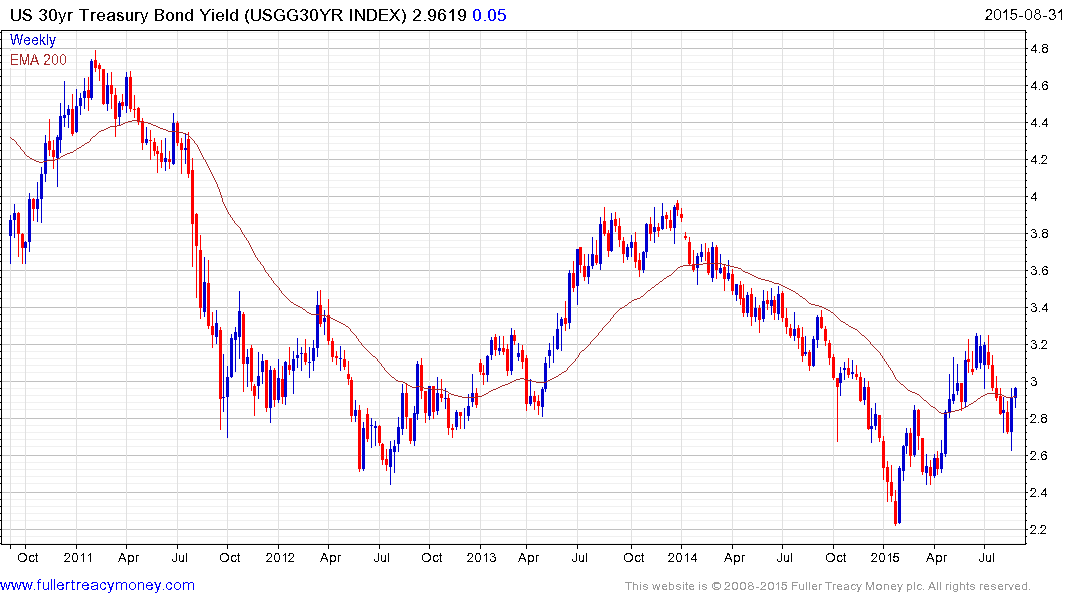

The 30-year moved to a new all-time low in January but has held a progression of higher major reaction lows since, to form a failed downside break. A sustained move below 2.6% would now be required to signal a return to demand dominance.